close

“First, do no harm.” Interestingly, that line is not part of the Hippocratic oath, although it is attributed to the ancient Greek physician. It’s also not always practical; if we followed it, we would never have surgery, for example. The expression has resonated through the ages because it suggests a balance.

President Trump is trying to rebalance world trade and the interrelated financial system. Since the United States quit the gold standard in 1971, Americans have enjoyed what a former French finance minister described as our privilège exorbitant, in controlling the world’s reserve currency. The U.S. dollar is the most widely held asset by foreign central banks, the most widely used currency for foreign trade, and the currency of choice for many countries to borrow in. When Japan buys oil from Saudi Arabia, it pays in dollars; when Vietnam buys German machinery, it pays in dollars; when Argentina issues bonds on the world market, they are denominated in dollars. Global growth runs on the greenback.

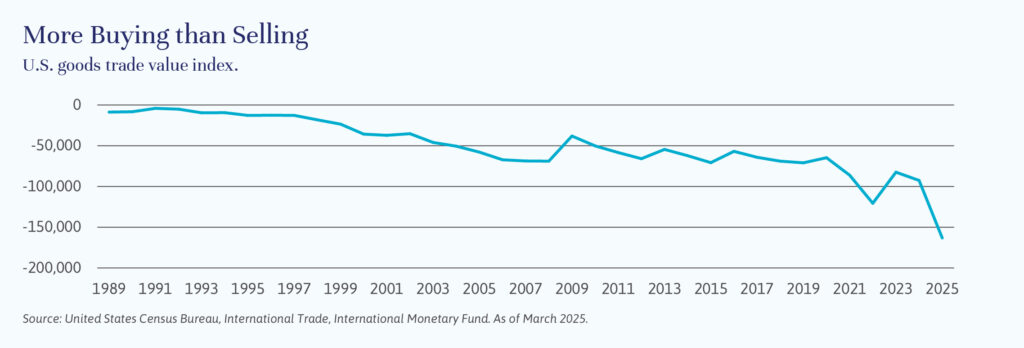

Access to all these dollars is facilitated by a persistent imbalance in the trade of goods between the United States and most of its trading partners. (The United States has a trade surplus in services and has benefited, along with the rest of the world, through the global growth generated by free trade.) But dollars sent overseas do not disappear. Instead, they are invested in U.S. dollar assets, including U.S. government bonds. This support has enabled the U.S. federal government to run ever larger deficits with higher debt levels without stressing the market.

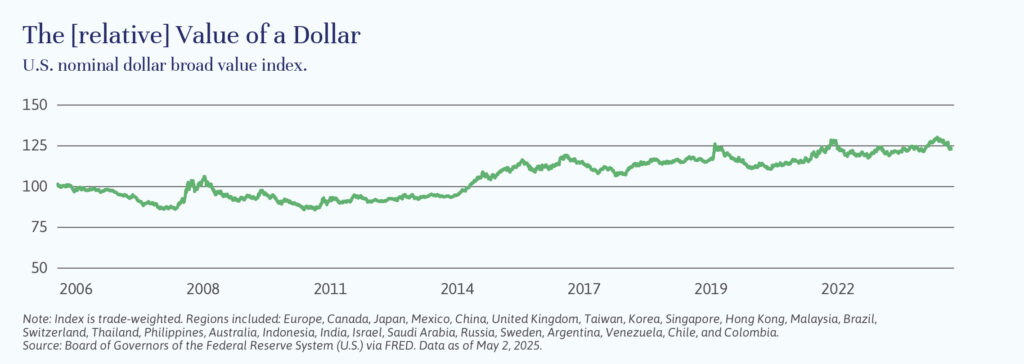

In short, the global demand for dollars, our great privilege, has until recently kept the value of the dollar high. This currency strength has enabled U.S. consumers to buy foreign goods cheaply and enabled emerging markets to build up manufacturing bases to meet that demand, lifting millions of people out of poverty.

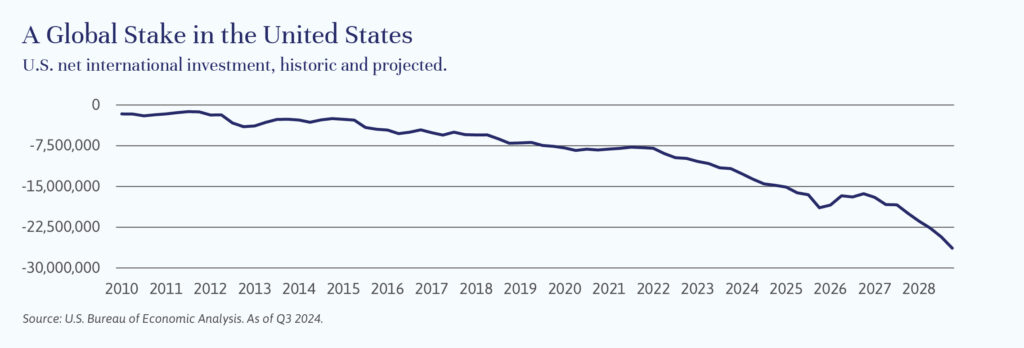

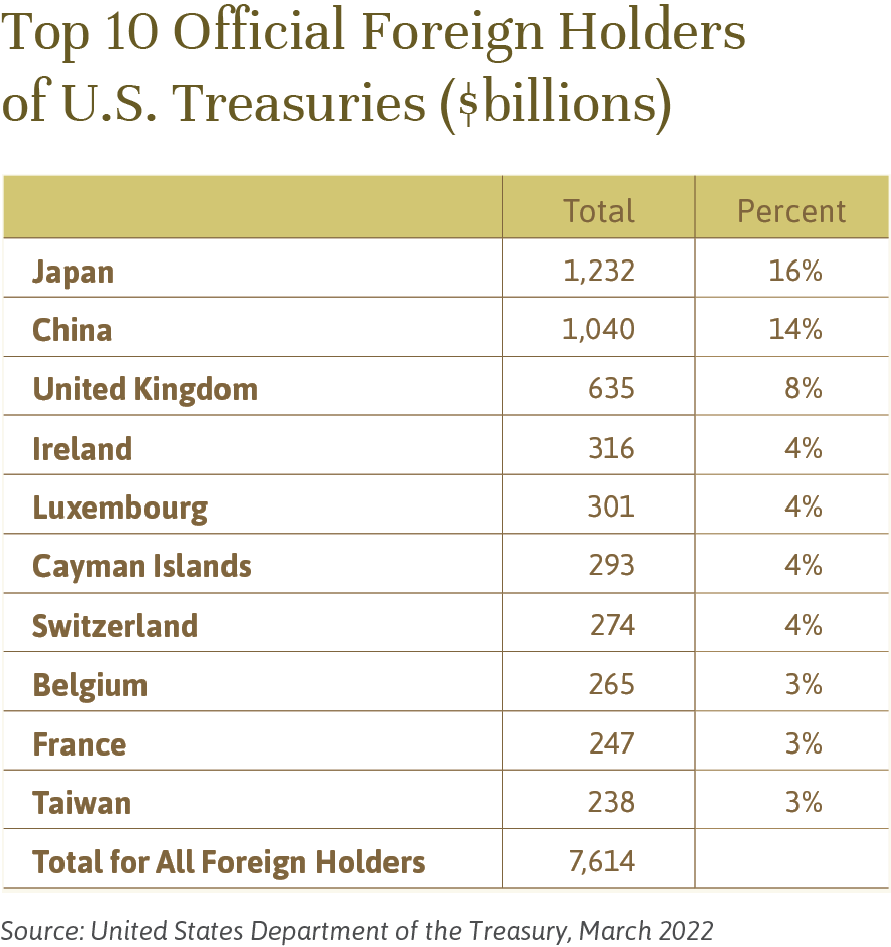

Has it all been too much of a good thing? Clearly, this administration thinks so. As a result of all the additional dollars invested back in U.S. dollar assets – including public equities, government and corporate bonds, real estate and direct investments in plants and equipment – the United States has an increasingly unbalanced investment position. Foreign entities own far more U.S. assets (a net $26 trillion) than U.S. investors own foreign assets. (See the chart “A Global Stake in the United States”.)

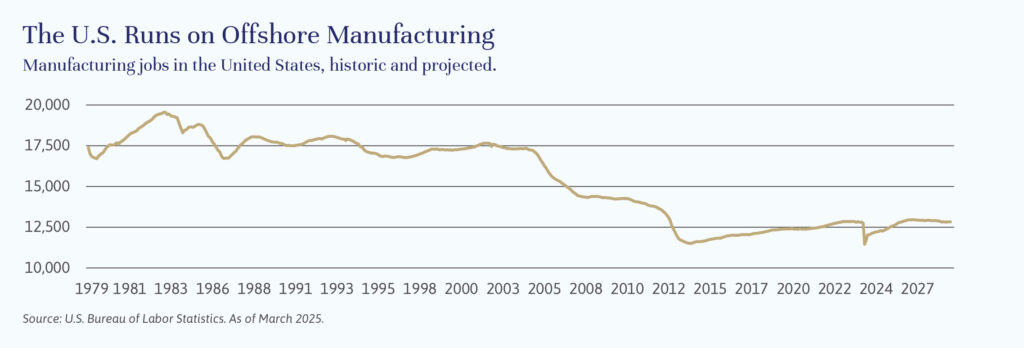

An additional consequence of the current system is that American workers and communities dependent on U.S.-based manufacturing are suffering. And we have become dependent on foreign-made supplies of many strategic items, including manufactured goods and materials necessary to build up and replace armaments and other military equipment. Addressing these issues through onshoring will take considerable effort and time and investment – and will not be economically advantageous in many cases.

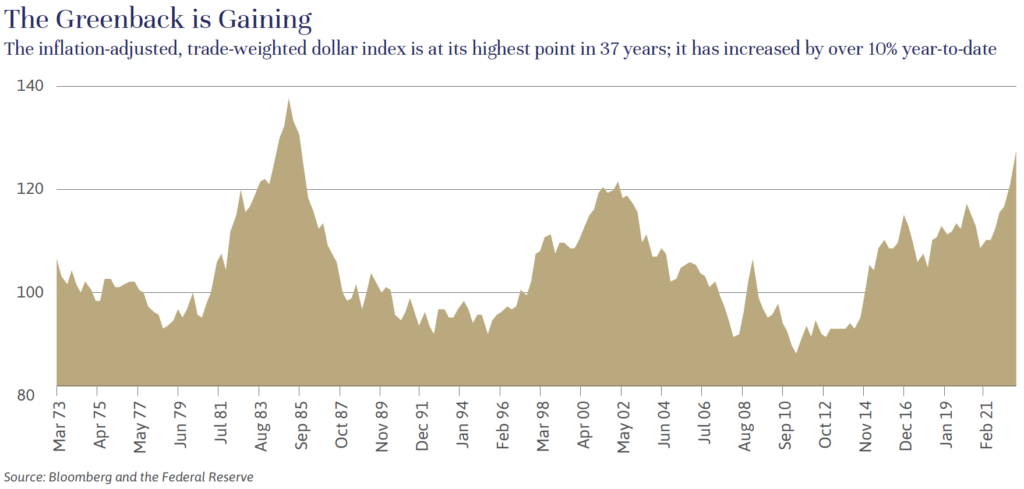

A managed devaluation of the dollar has been tried in the past. (See the article by Brian Pollak “A Brief History of Reserve Currencies”.) The efforts this time so far are more like a shock treatment. Very high and erratic tariffs and related threats are making the patient worse. The U.S. dollar is falling now, but possibly for the wrong reasons. After a dizzying spate of contradictory announcements from President Trump, the world is questioning the basic assumptions that have underpinned its reserve currency status – the economic vitality and political stability of the United States, along with our commitment to the rule of law, defense guarantees, and our responsible, independent central bank.

While we continue to expect that the extreme tariff rates will be reduced, partly in response to market reaction, and that the dollar will decline more gradually, there is now an increased probability that the United States and much of the world will enter a recession.

We are managing portfolios with these heightened risks in mind. In uncertain times, it is imperative that portfolios are well diversified. Our clients have benefited from being overweight U.S. public equity – and those gains are now being rebalanced in favor of international equities, as well as private equity where appropriate (see the article by Stephanie Hackett on “Buying, Building and Selling: Investing in Private Equity”) and public and private credit. These asset classes provide further diversification and, in the case of credit, enhanced income. Additionally, there should be sufficient cash and short-term bonds in portfolios to fund spending needs for two years or more.

John Apruzzese is the Chief Investment Officer of Evercore Wealth Management. He can be contacted at apruzzese@evercore.com.

Companies backed by private equity in the United States now outnumber publicly traded companies by two-and-a-half times, a 400% increase since 2000.1 They represent the fastest-growing sectors of the market, generating many technologies, products and services that investors cannot access in the public markets. What’s more, private companies have outperformed publicly traded companies in 97 of the last 100 quarters, on a 10-year rolling return basis.2

For many qualified investors, private equity is now the most exciting asset class.

The concept hasn’t changed much in 25 years. Private equity firms raise capital from outside investors and use it to buy companies with the goal of increasing their value and, eventually, realizing a profit. This process often involves expansion or restructuring, improving operations, strengthening management, and supporting companies through periods of stress.

What has changed is the scale of the investment set. Options range from very early-stage companies developing new products or technologies, to investing now in established businesses that need capital for expansion or operational improvements. Of the U.S. companies with annual revenues over $100 million, 86% are still private.3 Not surprisingly, they are in no rush to list. As private capital ecosystems continue to grow and strengthen, these companies can stay private for longer.

Two areas of private equity appear particularly attractive at present. The first – buyouts – are investments in established businesses with stable cash flows to implement operational improvements, expand to new products or geographies, eliminate unnecessary processes or costs, or to make add-on acquisitions. Buyouts acquire controlling and/or majority stakes and typically use larger amounts of debts. The second – growth equity – is made up of companies with proven business models that experience high growth rates or pivotal change, along with some recurring revenues. Growth equity investments are typically minority ownership stakes using little or no debt.

Private equity buyout managers have adjusted to higher interest rates and the higher cost of capital by reducing the amount of leverage. The market corrections over the last few years have forced companies to balance between growth and profitability, making this a compelling time to invest new capital.

Growth equity valuations have fallen by more than half from their 2021 peak, as initially overly eager investors came to realize that valuations should always reflect the illiquidity and complexity inherent in this asset class. Transaction volume has decreased, and private equity funds have struggled to attract new capital funding over the past two years.4

But the survivors have continued to build their customer base and grow revenues. The technology sector has been buoyed by strong fundamentals, and deal activity in tech started to uptick in 2024 and is expected to continue to increase in 2025-2026.5 The private equity healthcare sector has lagged over the past several years due to regulatory complexity and policy uncertainty but is also gathering steam.6

At Evercore Wealth Management, we are focused on manager selection in this asset class and advising clients on their optimal allocations. For those investors that have a long-term investment horizon and a risk tolerance for illiquidity, allocating to private equity can add diversification and potential for outsized growth. Private equity and other illiquid investments generally represent between 5% to 20% of individual portfolios, depending on investor qualification, investment horizon and goals.

Stephanie Hackett is a Partner and Portfolio Manager at Evercore Wealth Management. She can be contacted at stephanie.hackett@evercore.com.

Choosing the right managers is key to success in private equity, as we expect our private equity investments to earn a premium that will compensate for illiquidity.

Private equity remains an inefficient asset class, meaning that information access and manager skill can be significant drivers of return. It is critical to identify managers able to buy well, build well and sell well:

Buy well: Private equity funds have historically bought companies at valuation multiples that average 2.5 times lower than public market multiples.7

Build well: Private equity funds have been able to build companies with higher and more resilient growth through economic cycles, despite higher leverage.8

Sell well: Private equity funds add value during their ownership, selling better businesses than they bought. The average valuation multiple for private equity-backed companies is 1.2 times higher at exit versus what the managers paid at entry.9

Over the past 10 years, the dispersion in performance between the top quartile and bottom quartile for public equity portfolio managers has been between 2% to 3%. In private equity, this performance differential is 20%-plus.10 And there is greater evidence of performance persistence in private equity. About 70% of private equity funds that performed in the top quartile of their vintage year have a successor fund that also generated above median returns.11 Top-performing private equity funds can attract and retain talent, as well as access unique and proprietary deal flow. They are also able to raise larger successor funds that are often oversubscribed, so the teams spend less time fundraising and more time focusing on their portfolio companies.

— SH

Lawyers now spend seconds on contract reviews that used to take hundreds of (billable) hours. Data center cooling costs are being slashed. And digital agents are helping customers unlock productivity at an exponential scale. These are just three examples of Artificial Intelligence, or AI, driving meaningful change in corporate America. Potential further advances – in medicine, robotics, vehicles, marketing, you name it – suggest that the surface has barely been scratched.

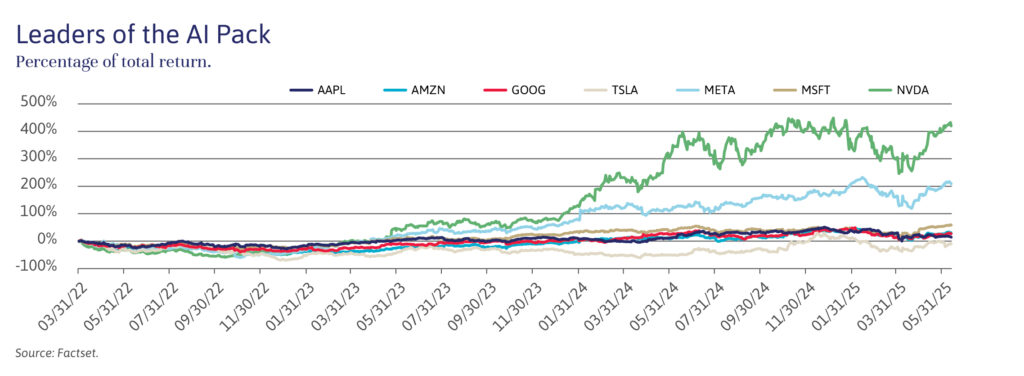

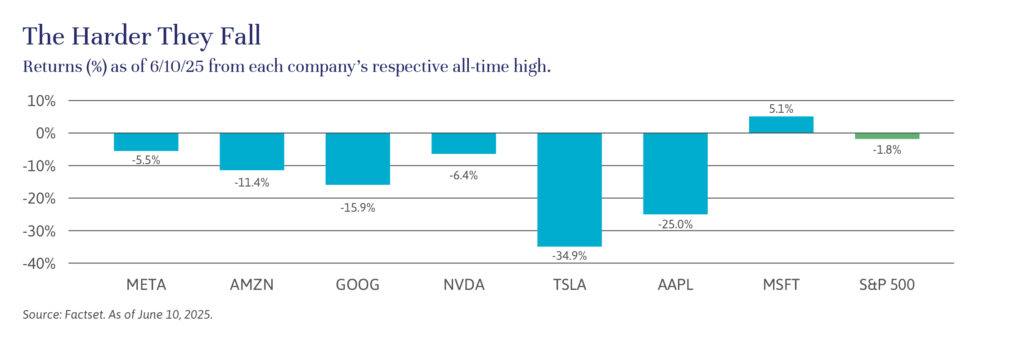

Still, AI has tested investors’ patience lately. After years of dramatic market outperformance, the share price of most members of the so-called Magnificent Seven – Amazon, Alphabet, Apple, Microsoft, Nvidia, Meta and Tesla – tumbled in recent months, as illustrated by the chart below. Though several have recovered appreciably, investors are clearly looking for a payoff.

It’s still early, though. Microsoft CEO Satya Nadella recently noted the evolving deployment of AI and the cloud, pointing out that most companies are early in the process of moving from the AI training phase of adding data and teaching models to understand specific data and processes, to the “inference” phase, in which AI models are deployed to actively drive results. Think of it as moving from learning how to ride a bike to actually riding it.

The gains we’re seeing today may be relatively simple compared to what’s coming. Nvidia CEO Jensen Huang and others have been focused on the next wave of AI: agentic AI, robotics, and autonomous vehicles. Agentic AI refers to systems that can make decisions and act autonomously to complete tasks. A customer service agent that automatically replies to emails, processes returns and updates records without human intervention would be an example. In robotics, companies like Boston Dynamics use AI to help machines navigate terrain, recognize objects, and perform complex functions like warehouse automation. In the world of autonomous vehicles, Tesla and Waymo use AI for real-time decision-making, enabling cars to detect obstacles, follow traffic rules, and operate without human drivers.

At a recent investor conference, Uber CEO Dara Khosrowshahi said that he was seeing a shift from “little optimizations that increase some efficiency by five percent [to] 20%, 30%, 40% increases in efficiency.”1 As these use cases scale, powered by Nvidia chips housed in hyperscaler data centers owned by Amazon, Microsoft and Google, the broader payoff grows more tangible.

Crucially, the pace of innovation is accelerating. Each breakthrough builds on the last, compounding gains and shortening the time between invention and implementation. AI adoption has quickly risen to the top of the corporate priority list, with many seeing it as essential to staying competitive, agile, and efficient in an increasingly digital world. Success will be measured by improvements in margins and operational output. For hyperscalers, it will come down to revenue growth and free cash flow. Microsoft, for one, is seeing stronger-than-expected AI revenue growth in its Azure cloud division, but time will tell if the revenues come to justify the scale of its investment.

There will be bumps along the way. A slowing economy is causing CIOs to tighten budgets. Trade tensions are complicating supply chains and investment strategies. Regulatory issues will take years to settle. Even as open-source breakthroughs like DeepSeek challenge AI incumbents, they also reinforce the sector’s immense potential and, by extension, the long-term value of cloud infrastructure and leading-edge hardware.

In the end, the promise of revolutionizing business operations is simply too great for most companies to ignore. At Evercore Wealth Management, our portfolios include both companies providing AI technology and beneficiaries. For patient investors in companies positioned to take advantage of the AI revolution, we believe that the potential for gains should be well worth the wait.

Michael Kirkbride is a Partner and Portfolio Manager at Evercore Wealth Management. He can be contacted at michael.kirkbride@evercore.com.

Gold could be considered the first reserve currency. The first gold coins that we know of were struck around 550 BC, initiating a measure of value and facilitating trade and transactions between different groups of people – even those from different regions and cultures – that has lasted to this day. Gold remains a monetary asset to this day, never entirely losing its luster.

Spanish silver dollars, also known as Spanish Pieces of Eight, and Dutch guilders are now collector items. But each also had their time in the sun. Pieces of Eight emerged in the 16th century as the first reserve currency associated with a sovereign nation. The coins were uniform in weight and silver content, making them a reliable medium of exchange as Spanish ships traveled around the world. The Bank of Amsterdam, established in 1609 and often considered the precursor to modern central banks, was the first public bank to offer accounts that were not directly convertible to coin, creating a new and easier form of transferability and liquidity. This innovation supported the use of the Dutch guilder as a global currency, as did the simultaneous rise of the Dutch East India and Dutch West India trading companies, which expanded global trade throughout Asia and the Americas.

By the 19th century, trade and capital investments were often denominated in sterling. Britain’s dominance in technology, innovation and production allowed its goods to be sold around the world and created the need for large quantities of raw materials and natural resources. Sterling weakened substantially through the world wars, when Britain took on significant debt and exhausted its foreign reserves. Nevertheless, it maintained an important position in global trade and as a reserve currency for much of the world until the end of World War II, when the sun finally set on the British empire.

Enter the U.S. dollar. The U.S. manufacturing base, unscathed by the Great War, became a producer of goods for all of Europe, including the United Kingdom, helping to elevate the dollar to a global currency. In addition, the U.S. dollar generally remained a hard-backed currency during this period, while many European currencies of the day, including sterling, did not. (The United Kingdom went off the gold standard from 1914 to 1925 and then permanently in 1931.) U.S. dollars poured into Europe and Japan after World War II to rebuild and redevelop shattered economies and infrastructures.

The Bretton Woods conference of 1944 codified the role of the U.S. dollar as the foundation of the global financial system. Here, most global currencies were officially pegged to the dollar, which was pegged to gold at a fixed exchange of $35 an ounce. The World Bank and the International Monetary Fund were established as well, all with a goal of stabilizing the post-war global economy.

It was, without a doubt, the American century. But there were two significant currency events since Bretton Woods, both provoked by large global trade imbalances.

The first was the so-called Nixon Shock of August 1971, in which the United States broke the Bretton Woods agreement by ending the convertibility of dollars to gold. The country was then running significant (although small by today’s standards) twin trade and fiscal deficits. Americans were buying a lot of West German and Japanese goods (the trade deficit) while funding the Vietnam War and the Great Society programs (the fiscal deficit). At the same time, many central banks were converting their dollars into gold, draining U.S. gold reserves, while the United States kept printing dollars without enough gold reserves to back those dollars.

Leaving the gold standard solved the problems of the day, weakening the dollar and rebalancing trade, at least for a time. It also gave global central banks, including the U.S. Federal Reserve, more autonomy over monetary policy, allowing most global currencies to float freely. But it made the dollar a fiat currency, wherein the value of a currency is derived from trust, not by the backing of a physical metal. This has caused the devaluations of less powerful currencies, such as the Argentinian peso, and many more currency crises. Some economists believe that those monetary policy actions were at least part of the reason for the stagflation (slow growth and high inflation) that persisted in the United States through much of the 1970s.

The second major intervention was the Plaza Accord of September 1985. In the years prior, the dollar had appreciated significantly against other major currencies, largely due to the relatively high interest rates implemented by Federal Reserve Chair Paul Volker to fight inflation. The recovered strength of the dollar had made U.S. goods more expensive to export and foreign goods cheaper to import, leading to another large trade deficit, again with West Germany and Japan. The Plaza Accord participants (the G5 – the United States, the United Kingdom, Japan, West Germany and France) agreed to work toward weakening the U.S. dollar, specifically in relation to the Japanese yen and German deutsche mark. The Accord essentially worked, leading to a lower dollar and a narrowing of trade imbalances. By 1987, the Louvre Accord was struck, essentially reversing the Plaza Accord, ending the period of dollar weakness and stabilizing the global currency markets.

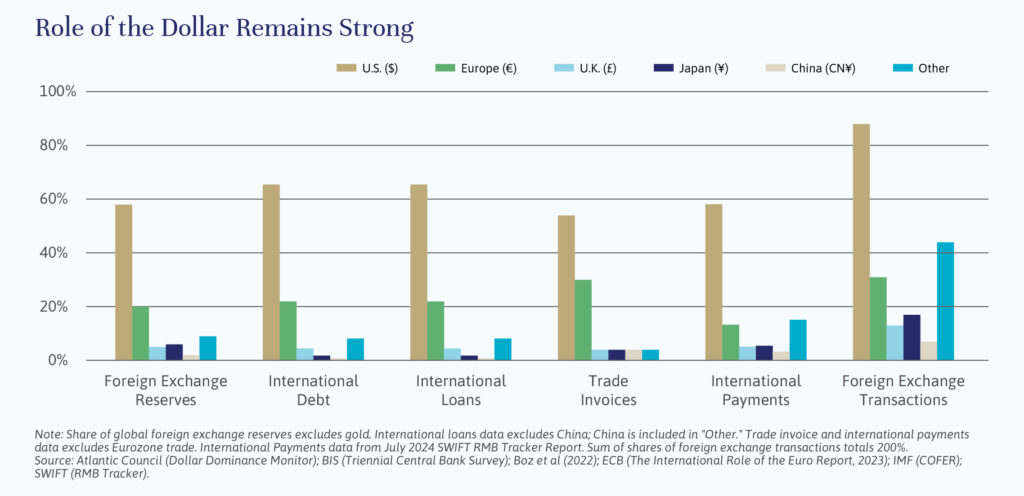

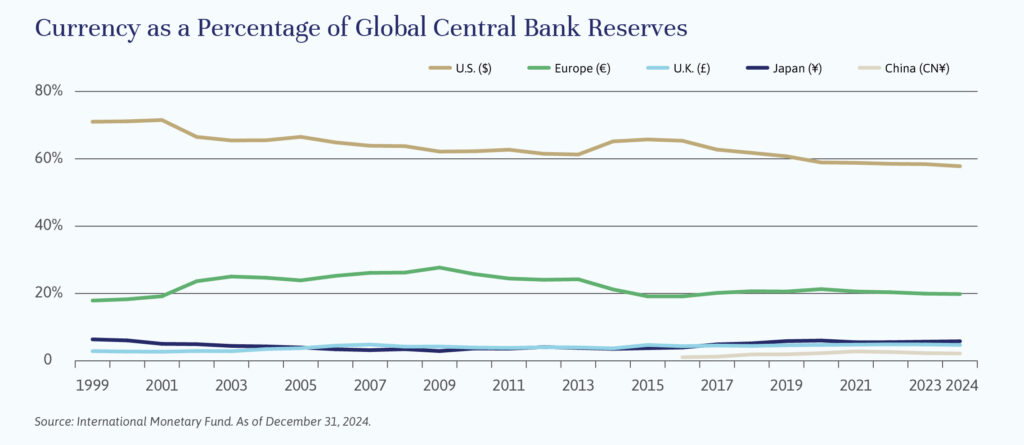

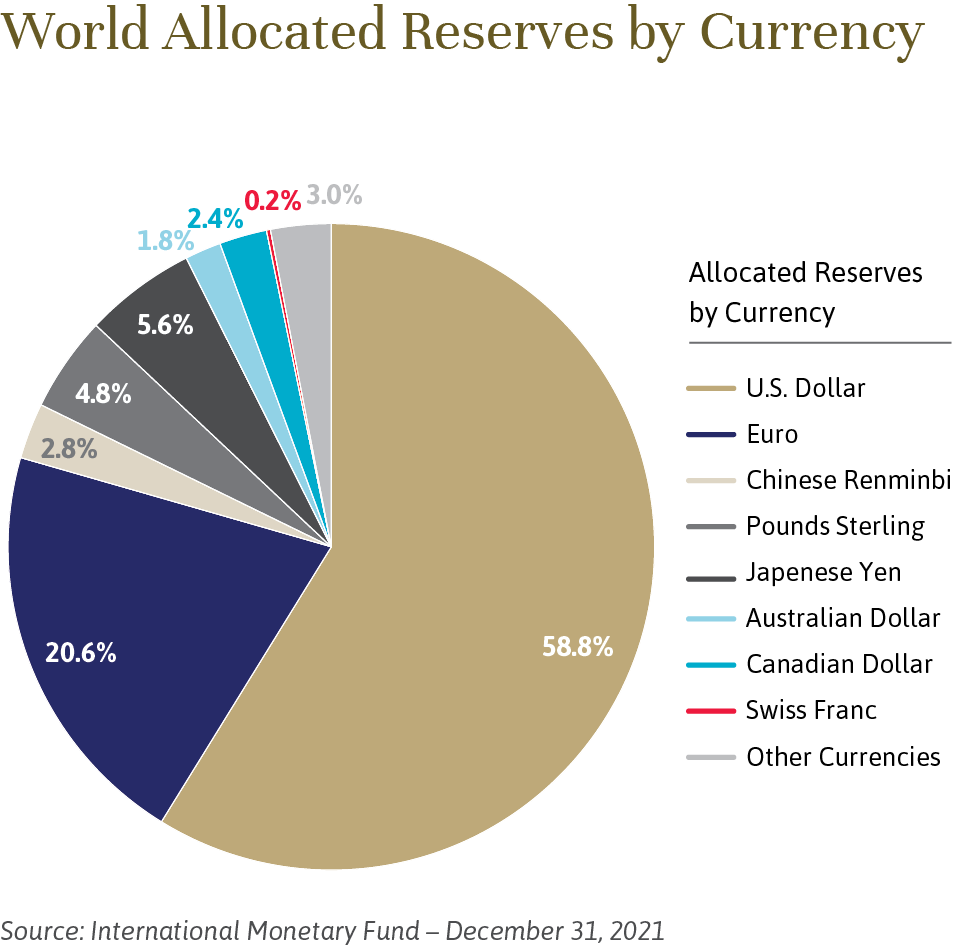

Will the Trump administration’s attempts to weaken the dollar constitute another major dollar intervention? It’s too early to say. The fiscal and trade imbalances of today are more significant than those of either 1971 or 1985, but the economy itself is in better shape, and the dollar continues to benefit from global trust in the United States, as illustrated in the chart “Role of the Dollar Remains Strong”. Still, there are already signs that the dollar is fraying. Its share of global central bank reserves fell 13% over the past 25 years as others grew, primarily the Euro but also the yen, sterling, and the Chinese yuan. (See the chart “Currency as a Percentage of Global Central Bank Reserves”.) And gold, the original reserve currency, still plays an important role 2,500 years on. International debt, currency denominations, international trade and foreign exchange transactions tell a similar story.

It is reasonable to predict that the dollar continues to erode, ceding more of its dominance as the global currency. The difference this time is that there is no single alternative currency waiting in the wings, at least not yet. The Euro suffers from still uncoordinated fiscal policies; the yuan is still a highly managed currency, currently kept deliberately low by the Chinese government; and the yen suffers from demographic challenges and very low interest rates. Digital assets like Bitcoin are nascent and highly volatile. Stablecoins are a more likely potential solution, but digital assets pegged to one or more fiat currencies remain in a very early stage of development. And gold, while shining bright at present, is not a scalable alternative. For most U.S.-domiciled investors, who will want to match dollar liabilities with dollar assets, diversification away from the dollar makes sense only incrementally.

Brian Pollak is the Head of the Investment Policy Committee at Evercore Wealth Management. He can be contacted at brian.pollak@evercore.com.

Editor’s note: Asset-backed credit is an important and growing asset class. Here we interview Michael Paniwozik, president of Apollo Asset Backed Credit Company, or ABC, one of the carefully selected outside fund managers that supplement the core capabilities of Evercore Wealth Management. Please note that the views of the external managers interviewed in Independent Thinking are their own and not necessarily those of Evercore Wealth Management.

Q: Let’s start at the beginning. What is asset-backed finance, exactly?

A: Asset-backed finance is a critical tool for financing the day-to-day activities of millions of businesses and consumers globally. It encompasses a broad set of credit types that touch everyday life, from residential mortgages, credit cards and student loans, to planes, trains, automobiles, sports and entertainment royalties, and more.

This asset class can provide investors with downside protection through credit enhancement and structural safeguards, as well as diversification and yield at the investment and portfolio levels.

Q: How does Apollo approach asset-backed finance?

A: ABC affords investors access to high-quality asset-backed instruments across a diverse range of sectors, providing yield in excess of publicly traded credit of comparable quality.

Our proprietary sourcing engine – along with disciplined “purchase price matters” investment philosophy and the scale and diversity of our capital base – allows for access to a differentiated risk/return profile within private credit. The breadth of our offering across all different types of asset-backed risk enables us to invest in all market conditions.

Q: Why is that important?

A: Our asset-backed investments offer access to diversified collateral pools across unique and idiosyncratic asset classes. This differentiation makes asset-backed finance particularly impactful, as its performance is generally less correlated to corporate credit, delivering attractive diversification and enhancing portfolio resilience.

Unlike allocations to direct lending, which from a risk standpoint compares to single-B/high-yield risk, private asset-backed credit is predominantly investment grade or investment grade-like. About 80% of the portfolio is investment-grade or IG-equivalent, with de minimis subprime exposure. Our investors use ABC as a replacement for or complement to public fixed income exposures. Zero portfolio-level leverage further enhances downside protection and reduces forced selling risk.

Q: What is your impression of the scale of this opportunity?

A: The asset-backed finance, or ABF, market is massive, with around $20 trillion in market size globally. This makes it much larger than the circa $3 trillion public/private leveraged corporate credit markets. It is experiencing the same type of de-banking that we have seen with corporate finance, creating opportunities for non-bank financial institutions like Apollo to access the underlying assets and structure private ABF loans. Private ABF loans can offer 1% to 2% premium in spread/yield versus both public ABF and public corporate credit on a ratings- and duration-matched basis.

Q: Why do you believe the ABC is particularly well placed to take advantage of this opportunity?

A: ABC is a semi-liquid, turnkey solution that provides investors access to high-quality, asset-backed instruments across a diverse range of sectors, aiming to provide yield in excess of publicly traded credit of comparable quality. We seek to invest in what we believe will be the most attractive risk/return opportunities across the five major categories of the asset class, focusing primarily on directly originated investment grade or equivalent assets.

And of course, ABC benefits from the Apollo ABF Platform’s broad origination channels. The firm has been investing in asset-backed credit for over 16 years and now has more than $312 billion deployed. We have 30-plus direct sourcing platforms and partnerships with 4,000 employees working on various asset-backed risks every day. We originate approximately $75 billion annually in asset-backed finance across some 50 asset classes and have material skin in the game with strong alignment with our investors.

Q: What is your outlook now?

A: We believe private markets remain an attractive alternative due to their resiliency, lower volatility and lower correlation to public markets. Public markets tend to experience extreme price movements when liquidity evaporates. Private markets are priced upon the fundamentals and financials, mitigating the lack of liquidity and discounts.

It’s also worth noting that ABC’s holdings are backed by thousands of underlying borrowers across sectors and geographies, reducing idiosyncratic risk. With broad exposure across five asset-backed pillars, ABC avoids overconcentration and has minimal direct sensitivity to tariff-impacted sectors.

For further information, please contact Evercore Wealth Management Partner and Portfolio Manager Stephanie Hackett at stephanie.hackett@evercore.com.

Oscar Sloterbeck

Editor’s note: Oscar Sloterbeck is Head of Company Surveys at Evercore ISI, one of the sources of research considered by Evercore Wealth Management. The surveys are used by ISI macro and fundamental research teams to measure the evolving strengths and weaknesses of the U.S. economy. Executives, typically CFOs and Treasurers, at 325 companies across 29 industries provide an index rating based on their evaluation of the strength or weakness of recent sales adjusted for the time of year.

Company capital expenditure, or CapEx, on technology is rising again, albeit at a moderate pace, according to our 2025 CapEx & Hiring Plans Survey, conducted after the U.S. presidential election.1 This outlook is consistent with solid U.S. economic growth.

Following the pandemic-driven decline in 2020, nominal CapEx growth was strong in 2022 and 2023, before moderating in 2024. Structural investment in data centers, industrial, tech, infrastructure, and pharmaceutical facilities has been strong, as has the upgrade of existing plant and equipment, as companies focus on boosting domestic production and increasing productivity. Spending remains high in these areas, but growth is moderating. We continue to see most U.S. multinationals increasing the U.S. share of their global CapEx budget as companies work to derisk their supply chains.

One variable that could change 2025 CapEx plans is a cut to the U.S. corporate tax rate. Companies are telling us that reinvestment will be the top use of funds if a U.S. corporate tax rate reduction occurs in 2025.

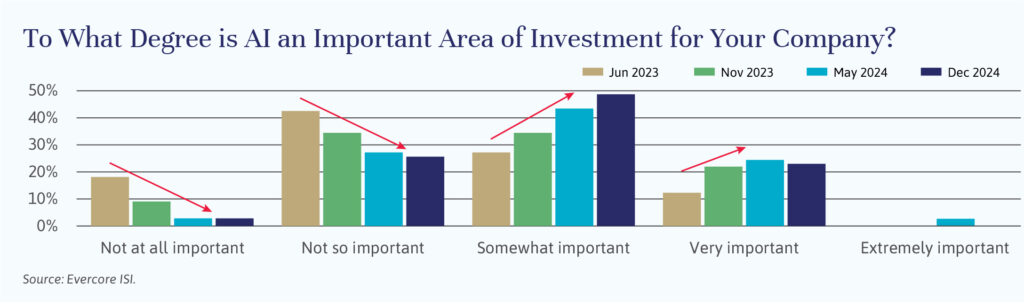

While overall CapEx is expected to slow, companies plan to increase tech spending in 2025. The focus of spending includes cybersecurity and AI, as well as CRM and ERP systems. (Editor’s note: Artificial Intelligence, Customer Relationship Management and Enterprise Resource Planning systems, respectively.)

In our 2025 survey, 71% of respondents categorized their AI investment as important, up from 56% in November 2023. Large companies view their AI investment as particularly important relative to companies with less than $1 billion in annual revenues. Firms expect to see the greatest value in their AI investment from internal efficiencies, with additional value deriving from customer service and sales and marketing. Many are focused on the potential impact on labor markets from the increased use of AI. Currently, roughly one-third of companies report that AI is already augmenting their human labor; the majority see any replacement of labor from AI as more than a year away. Recent productivity data has been good, enabling the U.S. economy to sustain solid growth while inflation has moderated. Our survey shows the funds for investing in AI are coming from other areas of spend, and for this year, it appears the funds allocated to AI are coming from traditional areas of CapEx, as opposed to the tech budget.

Companies do have concerns that are limiting the use of AI and are restraining investment. The most common gating factors include accuracy and reliability, followed by cleaning and preparing internal data, as well as cybersecurity and legal concerns.

Turning to labor markets, companies told us that hiring plans for 2025 are ticking up modestly, after decelerating from their all-time high in 2022 when job growth surged out of the pandemic. This improvement is broad across industries from consumer to industrials. Real estate companies are the one area showing softness, as the housing market remains mixed. Labor availability in the United States is improving, but labor is still viewed as somewhat “hard to get,” while availability remains pretty good in Asia and Europe where economic growth has generally lagged. The latest data shows signs of stabilizing nominal growth, and our 2025 CapEx & Hiring Plans Survey suggests the new year will see an increase in tech CapEx and stabilization in employment.

Editor’s note: Emerging markets can afford U.S.-domiciled investors a range of diversification opportunities at relatively low valuations. Here we interview Caroline Cai, CEO and Portfolio Manager at Pzena Investment Management, one of the carefully selected outside fund managers that supplement the core capabilities of Evercore Wealth Management. Please note that the views of the external managers interviewed in Independent Thinking are their own and not necessarily those of Evercore Wealth Management.

Q: Global equity market performance this year has been driven by a relatively few mega-cap U.S. growth companies. This has led to a significant difference in performance between growth and value stocks, particularly in the United States. Has the disparity between growth and value stocks also occurred in emerging markets?

A: The growth cohort is outpacing value in emerging markets as well, albeit by about six percentage points versus over 19 percentage points in the United States. The bulk of growth’s alpha stems from a single company, TSMC, which is NVIDIA’s AI chip supplier. This Taiwanese foundry giant had an approximately 17% average weighting in the MSCI Emerging Markets Growth index in 2024, returning roughly 70%. TSMC is not included in the MSCI Emerging Markets Value Index, but it is included in our portfolios, as we believe the stock remains cheap relative to its intrinsic value.

Q: For U.S.-domiciled investors, what is compelling about investing in emerging markets now?

A: Emerging markets are particularly cheap, in our view, trading at a 48% price-to-forward earnings discount to the top-heavy U.S. equity market. This offers investors diversification at the largest discount in more than two decades.

That said, we believe it’s important for investors to be selective when it comes to emerging markets. They are inherently disparate, with each country possessing its own unique risks and opportunities. Today, we are observing the type of valuation dispersion that is typical of such a diverse asset class, with India and Taiwan, two countries that we’ve reduced exposure to amid surging equity markets, trading at the upper end of the valuation spectrum, while China, Korea, Brazil, and others (all of which we’ve added to) now boast single-digit forward earnings multiples.

Q: If investors want to invest in emerging market countries due to the higher growth rates of these economies, how can a value approach lead to superior returns?

A: Perhaps because developing nations often post higher GDP growth rates than their developed peers, many market practitioners view emerging markets investing as a growth story. However, the value approach has proven far superior over time, with cheap emerging markets stocks (those with low price-to-book ratios) outpacing expensive names by 430 basis points per annum since 1989.1

Higher-beta emerging markets understandably endure more frequent bouts of volatility but can offer amplified return potential for value investors. We believe this is due to four key factors:

Psychology. Investors tend to exaggerate the significance of near-term problems, effectively discounting the potential for business, industry, management, currency or macroeconomic improvements over time. Active value managers can exploit these overly emotional responses, which are more prominent in emerging markets.

Earnings power. Despite the lack of empirical evidence, investors often inextricably link stock markets to economies, associating GDP growth with higher equity returns. When investors pay up for expectations of future growth, their reactions to disappointment can present a fertile hunting ground for disciplined value investors.

Range of outcomes. Different political and legal structures, currencies, and governance practices all add to the complexity of emerging markets investing, offering robust opportunities across a large pool of stocks.

Under-exploitation. Most investment managers tend to favor macroeconomic or quantitative approaches to emerging markets investing, prompting crowded trades and wider market swings that result in exploitable price dislocations.

These factors present opportunities to buy good businesses with low expectations, at attractive valuations. We believe valuation is the single best determinant of long-term returns in any geography.

Q: The fund is now slightly overweight in China. What do you find compelling about China now that you did not before?

A: China has become the largest hunting ground for emerging markets value in recent years. A macroeconomic slowdown and heightened geopolitical tensions have prompted selloffs in many outstanding Chinese franchises, despite these companies displaying solid financial performance. This has resulted in a large subset of Chinese companies offering financial metrics comparable to emerging markets peers at far less demanding valuations.

Despite a host of stimulus measures announced by the Chinese government in recent months, equities remain broadly cheap. Importantly, our investment thesis for the individual Chinese stocks that we own are not predicated on significant monetary or fiscal support from the government. These businesses are, in our view, trading at exceptionally low valuations that already discount persistent and severe economic pain. As Chinese valuations collapsed, we have selectively raised our exposure to stocks that we believe unjustifiably sold off due to temporary geopolitical and macroeconomic headwinds.

Q: How could the election of Donald Trump, who threatens to impose tariffs on Chinese imports, affect the Chinese companies that you own?

A: Tariffs and trade wars are always a threat, and we assess these risks on a company-by-company basis to determine whether – and to what extent – they might impact our estimate of a business’ normal earnings power. Generally speaking, the businesses we invest in have resilient operating models that we think are able to adjust to changing circumstances, including U.S. import tariffs.

Q: Can you please describe the Pzena process in analyzing emerging market companies?

A: Outside of our initial quantitative screen, our investment process exclusively entails deep, fundamental, company-specific research, whereby we seek to invest in good businesses trading at cheap valuations because of temporary pain that the market is interpreting as permanent/structural.

Our preferred valuation metric is price-to-normalized earnings, or P/N, which is a stock’s market value relative to our estimate of what a business should earn, on average, over the course of a full business cycle under normal circumstances. We only invest in companies in the cheapest P/N quintile of their investment universe. The discount rates we use to generate our normal earnings estimates and compare valuations across emerging market countries vary, depending on the country risk premiums. We use the market’s collective judgment, as proxied by a country’s long-term sovereign rate over the U.S. treasury yield, to measure a country’s risk premium. For example, a Chinese-domiciled company would utilize a materially higher discount rate in our valuation model than a South Korean company, and a South Korean company would have a modestly higher discount rate compared to a U.S. company.

Beyond the impact a higher discount rate has on the valuation of an emerging markets stock, which effectively raises the investment threshold, our research process is standardized across our strategies. Our analysts must understand and consider any factor that affects a company’s business, including the industry/country in which it operates and governance or regulatory issues that can widen the range of outcomes for a company.

For further information, please contact Evercore Wealth Management Partner and Portfolio Manager Judy Moses at moses@evercore.com.

If the history of antitrust law teaches us anything, it’s that innovation is the natural state, at least in the United States. By the time regulators focus on an issue, the market is often already working toward solving the problem.

When the U.S. government first filed its lawsuit in 1906, Standard Oil controlled over 90% of the domestic oil refining market. It also had a major position in pipeline distribution and was building scale in exploration and production. The company’s founder, John D. Rockefeller, was known for using aggressive corporate tactics, including securing exclusive agreements with railroads, driving competitors out of business through underpricing, and acquiring rival firms.

Yet, new competitors and new major oil finds were already on the horizon. The 1901 discovery of the Spindletop reserve in Texas – the first in the state – resulted in the formation of Gulf Oil and Texaco. The merger of Royal Dutch and Shell Transport and Trading Company was completed in 1907, creating the first scaled competitor to Standard. At the same time, the Anglo-Persian Oil Company was growing rapidly in the Middle East, changing the global playing field. It took until 1911 for the final judgment in the lawsuit to break up Standard Oil into 34 smaller companies.

Economically, the breakup created a windfall for Standard Oil shareholders but provided little relief for consumers. Rockefeller, who had stakes in all the new companies, saw his net worth treble between 1911 and 1913 to $900 million, or the equivalent of 3% of U.S. GDP, making him by this measure the richest man in the world1 – a record that has yet to be bested (Elon Musk is currently worth about 1.5% of U.S. 2023 GDP).2 Market dynamics and technology continued to change in ways that would have been unrecognizable to the Standard founder or the government regulators of his time, with new drilling technology, new modes of energy transportation and distribution, and expanding uses for energy all upending the status quo. Today, most of the legacy Standard companies are part of either Chevron or ExxonMobil; pieces of it are now owned by far-flung companies including ConocoPhillips, BP, and Shell.

AT&T, the successor company to Alexander Graham Bell’s Bell Telephone Co., was founded in 1885, and for over a century it maintained a dominant monopoly in both local and long-distance telephone service, and in telecom equipment manufacturing. The AT&T subsidiary Bell Labs was among the most innovative and influential research facilities in the world. The government’s antitrust case took eight years to conclude and another two to result in the breakup and sale of the local telephone business into seven new regionally focused entities, known at the time as the Baby Bells. The long-distance business remained with the legacy company.

A reasonable argument can be made that the breakup allowed for more competition in the short term, which begat more robust innovation, benefiting both consumers as well as investors. But we now know that the technology the government saw fit to break up was soon to be made irrelevant, as fiber optics, cellular telephones and the internet all displaced AT&T’s legacy technology. Consumer prices fell dramatically in the 1990s, particularly for long distance. By 2006, the phone companies stopped charging for long distance altogether, mostly due to robust competition from new entrants, like MCI and Sprint. But the price cuts came at the expense of significant added complexity, as consumers had to enter into separate bill pay and service agreements.

The Baby Bells have since reconstituted in the form of a more modern AT&T and Verizon. However, these companies derive most of their revenue from mobile and fiber optics businesses, both nonexistent businesses in 1982.

The Microsoft 1998 antitrust case did not result in a breakup. Although the initial judgment in 2000 ordered the company to devolve into two segments, it was overturned on appeal. Instead, the company agreed in 2001 to a settlement stipulating that Microsoft had to share its application programming interfaces, or APIs, with third-party companies.

Like Standard Oil and AT&T, Microsoft’s dominance in consumer technology was waning. One could argue that this was in part because of the settlement, which provided an easier competitive environment for companies like Alphabet (Google’s parent company), Meta and Amazon to build significant consumer-facing software businesses. And it is worth noting that allowing third-party API development is the model for today’s major consumer and enterprise platforms, including Google and Apple, which have been extremely powerful in spurring innovation in app development (Uber being perhaps the most obvious example). But competition in consumer technology is persistent, and the businesses Microsoft once dominated are a relatively small part of technology profits today.

Microsoft remains among the most valuable companies in the world. For investors in the company, the first decade post settlement, Microsoft’s shares underperformed the S&P 500 Index, as it took both time and effort to recalibrate the company’s focus to new areas. But investors who held on saw their total cumulative return rise 2,184% over the 23 years since the close of the case, close to triple the S&P 500 Index over that time.3 Today, Microsoft is a dominant cloud computing and enterprise solutions company, with consumer-facing businesses representing only a fraction of total revenue.

During the antitrust case against Microsoft, Bill Gates said, “People who feared IBM were wrong. Technology is ever-changing.” He was referring to the failed IBM antitrust case, which was the fourth largest (after the three discussed here) U.S. government antitrust case since 1900, and arguably the most redundant. But Gates’ point is important as we consider the potential antitrust cases against the Magnificent Seven.

While the incumbents might seem unassailable in 2024, it’s worth recalling that as recently as the end of 2012 (which was the first year all of the Magnificent Seven were public companies), Meta, then called Facebook, had a $63 billion market cap, was down 30% from its IPO earlier in the year, and was struggling to convert its revenue model to a mobile environment. Amazon had a $113 billion market cap, but almost no net income or free cash flow, and had yet to break out their cloud services unit, AWS, now its most important and profitable business, into its own reporting segment. And few had heard of NVIDIA, a $9 billion market cap company that was best known for making semiconductors for high-end gamers. No one has thought of IBM as a technology titan in a very long time.

To quote Bob Dylan, there’s nothing so stable as change. We remain vigilant both in questioning the depth and sustainability of the moats and management quality maintained by the largest technology companies. We are also attentive to opportunities to invest in smaller companies with innovative cultures that could be the subject of the next generation’s antitrust suit.

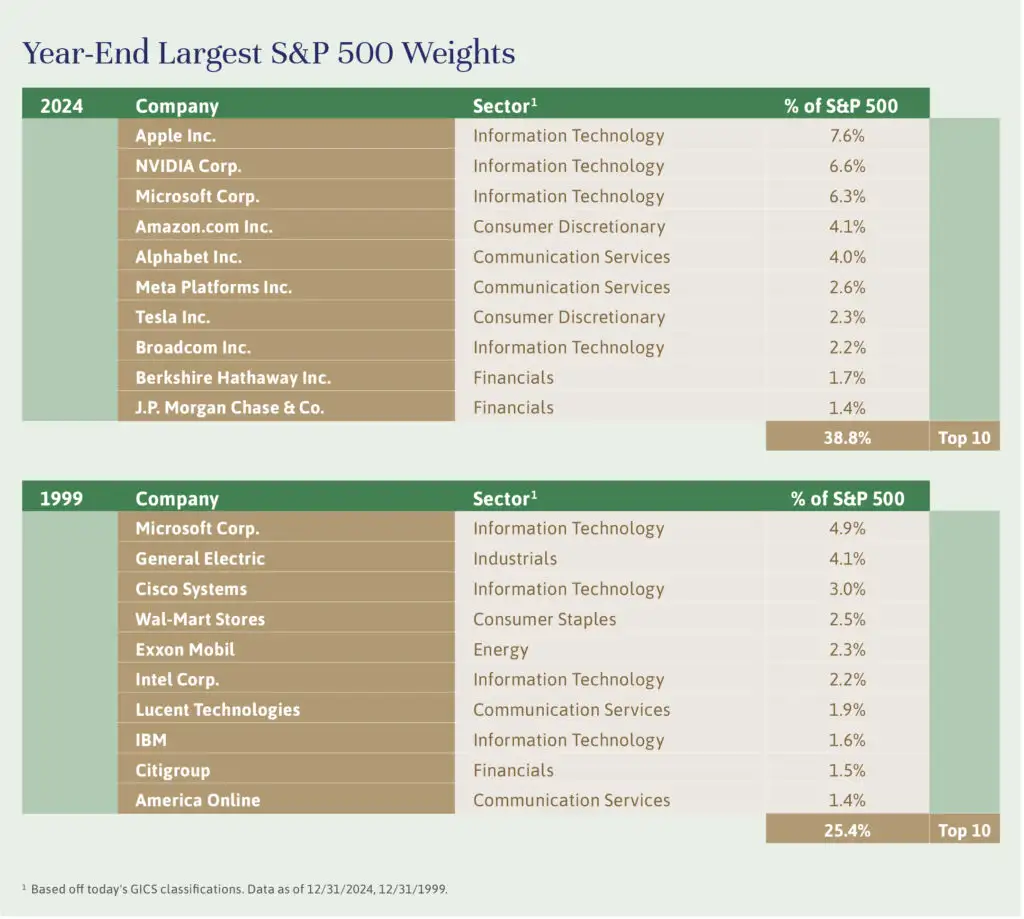

The S&P 500 has become so highly concentrated that it is taking on the higher risk and higher expected return characteristics of an insufficiently diversified portfolio. The largest market cap stocks in the S&P 500, appropriately dubbed the Magnificent Seven, now comprise almost 32% of the index and are growing faster than the remainder.

Prior periods of concentration involved large companies from very different industries, mostly blue-chip companies with strong balance sheets that had grown rapidly in the past but had evolved into risk-averse, conservatively managed companies. Take a look at the chart below, comparing this market with that of 25 years ago. The dominance of the leading companies is greater and less diverse.

The Magnificent Seven companies – Alphabet (Google), Apple, Amazon, Meta (Facebook), Microsoft, NVIDIA and Tesla – are among the most profitable, value-creating business entities ever devised. But they are all digital technology companies that are in large part betting their futures on the emerging AI technology.1 These companies not only have to capitalize on AI to meet current investor expectations, but they must do so soon.

It may take longer than investors currently expect, however. The promise of the internet back in 2000 was eventually realized, but it took years longer than companies and investors expected. Some companies never recovered. Others, like Microsoft, took over a decade to return to their old highs. Digital technology often creates a winner-takes-all dynamic; a global network effect and economies of scale whereby more users drive exponentially more usefulness and value. The main risk to an incumbent is a completely new technological innovation that changes the basic rules of the game. The recent launch of DeepSeek out of China is potentially just such an example.

It is unclear what proportion of these companies’ investment in AI is being spent on beating the other guy, rather than as the result of sober assessments of the potential returns. The Magnificent Seven are also running into the real-world constraint of electrical power capacity. The hyper-scaled data centers that Microsoft, Amazon, Alphabet and Meta are building with NVIDIA computer systems require more power than the current power grid can support, as we will discuss in the next issue of Independent Thinking.

Regulation is another pressing concern. These companies now dominate their respective spaces to the point that they could be considered near monopolies. Meta’s 77% share of social media, Google’s 80+% share of online advertising, and NVIDIA’s control of the latest AI chips are particularly striking.2 They can fend off competitors and earn unusually high margins – for now, that is. In his article, Adapting to Change: The Evolution of the Technology Market, Brian Pollak reviews government efforts to regulate or break up past monopolies and the risks now facing companies that could be considered the same.

It should also be noted that near monopolies are evident in other industries as well. Visa and Mastercard have a near duopoly in payment processing; Walmart, Costco and Home Depot continue to take market share from smaller competitors; and JP Morgan continues to pull away from its smaller rivals.

At the same time, there are at least two important emerging trends that could help smaller companies to grow faster. High interest rates, and day-to-day regulation fall far more heavily on smaller businesses. The Federal Reserve is in the process of lowering interest rates, and the new presidential administration should reduce regulation, even as it takes a closer look at Big Tech. It seems to us that a broadening out of stock market performance would be a healthy development, encouraging emerging innovation and competition.

In the interim, we believe we have positioned our portfolios to continue to benefit from the extraordinary performance of mega-cap stocks and better performance from the rest of the market. We are looking at new technologies earlier and considering the potential implementors. By retaining exposure to most of the Magnificent Seven but underweighting the group, we hope to mitigate concentration risks and to preserve and grow wealth.

Editor’s note: Neo Wang is the lead China economist/strategist at Evercore ISI, the leading U.S. research firm according to Institutional Investor’s annual survey.1 Evercore Wealth Management has limited investments in China, all of which are made through broader emerging market mutual funds.

Beijing is focused on building China into a leading modern socialist country, measured by both composite national strength and international influence, by the 100th anniversary of the People’s Republic of China, or PRC. The founding of the PRC in 1949 ended the century of humiliation, as Beijing puts it. So, what will it take to get there – and what will that mean for investors in the interim?

Economics 101 taught us that output equals labor force times productivity. On one side, China, the major country that is aging the fastest, is experiencing a decades-long secular decline in its labor force. The phaseout of the one-child policy completed in 2015 has hardly helped to revive the birth rate and, in any case, it still takes at least 16 years to raise labor. The idea of raising retirement ages, a seemingly instant solution, has met with strong resistance. Many retired people in China remain productive, helping to care for grandchildren. Any drastic change could send ripples across the economy, risking undesirable consequences.

On the other hand, productivity growth is subject to the law of diminishing marginal return and, in China, the technology “containment and suppression” led by Washington.

The best option left for China to sustain economic growth is to rely more on domestic efforts while striving to maintain business ties with the United States and its allies to realize net technology gains. The Party’s latest catchphrase, “new quality productive forces,” goes far beyond new energy vehicles, lithium batteries and solar panels to include semiconductors, Artificial Intelligence, advanced manufacturing, biomedicine and quantum technology. In essence, it is a supply-side upgrade, to climb the value chain and better serve both domestic and external markets.

Economic restructuring will get a push in this process, which we expect to be reflected in the evolving roles of four growth engines:

First, the supply glut of residential properties means that this sector is unlikely to generate capital gains over the foreseeable future. Any growth in the housing market will likely be solely through urbanization, and at a much slower pace.

Second, infrastructure investment will likely be favored by Beijing over real estate, as it generates a longer-tail economic and/or social benefit. It also helps to ensure a smooth downsizing of capital formation as a share of GDP.

Third, consumption should benefit from both the supply-side upgrade and rising spending power, thanks to the end of enthusiasm for homebuying.

Finally, exports should prove resilient due to China’s increasing supply of goods with higher value-added and at competitive prices to the vast emerging market as its manufacturing sector climbs the value chain.

Separately, so-called Japanification has been a recent rising concern of China watchers. They worry that deteriorating demographics, high debt, and the real estate troubles, all also issues in Japan in the 1990s, may similarly affect investors’ confidence. We think too much attention has been paid to the similar symptoms, while the vast differences have been largely ignored. Editor’s note: We interview WisdomTree Global Chief Investment Officer Jeremy Schwartz on Japanese equities here.

Beijing has been striving to become a reliable supplier and financer serving other developing countries, just as China was served by developed countries over the past four-plus decades. Getting the most out of the growth potential of the entire emerging market should be an indispensable part of Beijing’s efforts to sustain economic growth in the long run. The Belt and Road Initiative was just the start and helped to set the stage.

Soft power is more difficult to achieve. The PRC is an ideology minority and widely regarded by western democracies as an authoritarian regime. The Global South is more likely to embrace Beijing’s leadership and vision, but only to a limited extent given the competing forces, notably from India.

Against this background, we believe that Beijing has no interest in a war across the Taiwan Strait or in the South China Sea. The impressive military buildup is for deterrence so that it doesn’t easily get provoked and cornered into military response. Certainly, observers should question views driven by business or industrial interests, such as arms sales to Taiwan and diversification of chip capacity.

The United States is probably the last country interested in seeing China’s rising international influence. The two countries are engaged in a Cold War and de-risking, aka technology decoupling, will remain the dominant theme of the relationship. But deep economic integration and nuclear weapons greatly reduce the chance of falling into the Thucydides Trap, when a rising power threatens to displace a ruling power and a deadly pattern of structural stress sets in. We expect the two countries to remain adversaries, more contentious than competitors but not quite enemies. Compartmentalization should be the approach to manage the relationship.

As for the European Union, we expect Beijing to stay flexible and pragmatic, with the need to manage U.S.-China relations as a main consideration in its approach to Brussels.

One way China can increase international influence is by taking the lead in global efforts to cut carbon emission. China could potentially benefit greatly from this process, in areas such as industrial upgrades and reducing import dependence. Another way may be by playing a bigger peacemaking role. However, we expect Beijing to remain primarily inward focused and don’t see any reason it would want to help bring to an end any distraction in Washington.

Paramount leader Xi Jinping has been maintaining a tight grip over power and is expected to serve at least a fourth five-year term until 2032 when he will be 79 years old. After that, he will likely maintain his influence by retaining control over the People’s Liberation Army. With the fate of China largely hinging on Xi, two risks exist. One risk is in his health, rumored at times to be poor. We hope there is a succession plan, but there is no heir-apparent. The other risk is in the chance of a major policy error. Xi is a true Communist, like Mao, but there are important differences in their education, experiences and access to external views, which seem to us to mitigate this second risk.

At the moment, we don’t see much finger-pointing at Xi, even with the current economic headwinds. Most Chinese attribute these difficulties to lingering effects of the pandemic, rising geopolitical tensions, and the prolonged housing downturn. There is no imminent risk of social unrest, either from young people struggling to find jobs or high earners facing moderate pay cuts. China will remain a surveillance state, but the public is largely accustomed to it and perceives more benefits than drawbacks, a mindset encouraged by the government-controlled media.

From an equity portfolio investment perspective, we expect China to become increasingly less of a country story and more of a sector or stock play. Xi is playing the long game, attaching significant importance to sectors of strategical benefit to the country. Most of them feature hard technologies, in contrast to consumer-facing internet technologies. Foreign investors’ return seems not even close to the top of his priority list. To keep making money from China, investors may have to align their investments with Xi’s priorities.

However, some of Xi’s favored sectors are not at all suitable for western investors, because of Beijing’s recent focus on national security. We think the two most suitable sectors are healthcare and clean energy, which are supported by the surging elderly population and Beijing’s ambition for a green transition. Chinese companies are mostly safe if foreign investors avoid controlling stakes. And foreign companies had better avoid collecting genetic information on the Chinese people or supplying critical energy infrastructure.

As China climbs the value chain, the local market should become more competitive, due to stronger competition from Chinese peers and the changing mindset of Chinese customers. Foreign companies’ performance in China will be increasingly unrepresentative of how China‘s economy is doing overall.

Concerns over the repatriation of investment or profits seem to us unwarranted. We do not believe Beijing will punish any U.S. company for no other reason than the general tension with Washington.

For further information on Evercore Wealth Management and Evercore ISI research, please contact Brian Pollak at brian.pollak@evercore.com.

Bill Gates has a good line on change: “People,” he says, “often overestimate what will happen in the next two years and underestimate what will happen in 10.” We see evidence of that now, in the rush to exploit Artificial Intelligence (as described in CapEx: Too Much of a Good Thing?) and the related stock market volatility. If the past is any guide, the capital being spent today will eventually pay off – but the going may not be smooth.

CapEx mega-cycles are generally characterized by the invention of a new, disruptive technology that requires the buildout of massive infrastructure. They tend to revolve around major productivity-enhancing innovations, such as new forms of communication, new energy sources or generation methods, or transportation. Cheap and easy credit can pump investment – so can government backing through direct funding or regulatory support. While government support and debt funding can help a new industry get started, too much of both can often create a glut of capital, which leads to malinvestment.

The early automakers, the advent of electrical generation, and more recently, the smartphone, had prolonged growth trajectories. The industries that grew up around those new technologies all experienced consolidation (meaning many of the early companies failed), as well as continued innovation and capital spending. In the end, however, these advances in technology massively enhanced productivity without any significant economic hangover when their growth eventually slowed.

Other technological innovations were punctuated by overzealous capital spending booms followed by devastating financial crashes. Post-crash, industry growth and investment continued, albeit at a more reasonable pace. Steam locomotion was an early, transformative example. Invented in 1797 in England, the first rail lines in the United States were built in 1827 by the Baltimore and Ohio Railroad. The ability to transport goods and people quickly and safely over long distances changed the nature and trajectory of westward expansion in the country and supercharged national economic growth. In 1862, the Pacific Railway Act authorized the construction of the first transcontinental railroad, which ultimately linked California with the rest of the nation. This and the end of the Civil War in 1865 sparked even more growth, fueled by the combination of government support and debts. That ended in 1873 when Jay Cooke & Co., the bank that financed many railroad firms using high levels of debt, went bankrupt in September of that year. A market panic ensued, ending with bankruptcy of around one-quarter of the 364 railroad companies, and by 1876, 14% of the labor force out of work.

Still, railroads continued to expand after the crisis passed to peak in 1916 at over 254,000 miles. The growth of the railroads and continued improvements in track and locomotive technology spurred ever better connectivity and transportation, speeding the overall development and expansion of the country. The best investments were in the companies that benefited from this development, such as Sears, Roebuck & Company and Standard Oil, both of which leveraged railroads to build their companies to national scale.

Fast-forward to the telecom and internet boom of the 1990s and a similar story plays out at a much faster pace. The telecom CapEx cycle really took off in the middle of the decade as a massive new source of demand (the internet) combined with new advances in fiber-optic technology and the passage of the Telecommunications Act of 1996 (which allowed for more competition and new entrants).

This set off a wave of investment. Technology-focused capital spending between 1996 and 2000 increased by 75.6% cumulatively.1 Many of these big spenders were new entrants into telecommunications infrastructure, spurred by deregulation and further encouraged by a massive growth opportunity. While the internet usage and use cases continued to grow for decades, by 2001 it was clear too much capital had been deployed too quickly. Problems were exacerbated by fraud and too much debt: Global Crossing, WorldCom and Enron all went bankrupt due either to fraud or too much debt, or in some cases, both. The subsequent stock market crash resulted in massive declines, over 70% for both the tech-heavy Nasdaq and the S&P 500 Communications Services Sector Index.2 As with the railways, many of the companies that invested in the fiber build-out of the 1990s were not around to see it come to fruition. While AT&T, Verizon and Cisco are all still around, Amazon and Google, which used the internet and telecommunications network to build massive global businesses, turned out to be better investments.

AI is at least as likely to generate new industries and avenues for growth. But how long before today’s investments pay off? Is AI the next smartphone or will the cycle look more like the telecommunications industry? At current spending rates, Herculean growth assumptions must be achieved over relatively short periods. The biggest players know that, however, and they – Amazon, Google, Microsoft and others – have massive balance sheets and are taking on very little debt.

As investors, we are reasonably confident that these companies, among a few others, will be able at present to focus on AI’s potential over the next 10-plus years, and not just the next two, which mitigates the worst-case volatility for this cycle. But we are also cognizant that in past cycles, the best investments were often the beneficiaries of the innovation, not the innovators themselves. Sears was a better investment than Union Pacific in the first decades of the 1900s, just as Amazon was a better investment than Cisco in the first decades of the 2000s. We are focused on finding companies in healthcare, financial services and manufacturing that will be the primary beneficiaries of this CapEx cycle.

Brian Pollak is a Partner and Portfolio Manager at Evercore Wealth Management and the Chair of the Investment Policy Committee. He can be contacted at brian.pollak@evercore.com.

Public and private capital expenditure, or CapEx, is at record highs in the United States. From semiconductor manufacturing to cloud infrastructure expansion, to boosting the energy grid, incorporating Artificial Intelligence, or AI, into our lives isn’t cheap. At the same time, companies are also re/onshoring manufacturing, to control more aspects of critical supply chains and convert to greener energy. As the costs total up, thoughtful investors need to reconcile the benefits and the risks.

The scale of the investment is enormous. The largest cloud service providers – Amazon, Microsoft and Google parent Alphabet – are committed to over $150 billion combined in estimated CapEx spending this year.1 The lion’s share is earmarked for AI adoption, including infrastructure, services and research – to drive ever greater computation at ever greater speeds and scale. As illustrated by the chart below, that’s up almost 50% from collective CapEx spending by these three companies last year, and up over 85% from their five-year average.

In addition to these hyperscalers, next-tier cloud providers such as Oracle and IBM are ramping up their own CapEx to support internal AI programs. Indeed, Oracle is projected to double its CapEx in the year ahead. And Meta and Tesla have similarly massive spending requirements for their own networks, projecting $50 billion and $10 billion in CapEx over the next 12 months, respectively. Next up should be spending by corporations in the broader economy, including in the energy, healthcare, consumer products and financial services sectors, which will require the software, data centers and services that the hyperscalers are building out. In addition, plenty of money will be spent on the delivery of AI to people – the so-called Edge AI, which brings the tools to people’s phones and computers – and the energy necessary to enable all of this.

At the base of this investment is a reliance on access to the semiconductors that power all the data processing and analysis underlying AI. U.S. vulnerabilities here were cast into stark relief by the pandemic and cooling ties with China: The CHIPS and Science Act of 2022 has so far sparked announcements from Micron ($25 billion in Idaho), Taiwan Semiconductor ($65 billion in Arizona), Intel ($96 billion between Arizona, Ohio and Oregon), and Samsung ($45 billion in Texas), among others. All told, 80 or so projects are in the works. It is worth noting that these investments should create significant construction jobs and eventually tens of thousands of high-paying technology jobs, as well as make the United States more self-reliant.

More broadly, onshore manufacturing has fiscal support from the Infrastructure Investment and Jobs Act of 2021 and the Inflation Reduction Act of 2022. But bringing manufacturing back to our shores, which had been moved to China or Mexico over the proceeding decades, will not be a simple or immediate task. Still, 70% of U.S.-based companies with a global footprint have expressed an intent to reshore at least a portion of their manufacturing (per Cornerstone Macro) – and many have indeed begun to do so. This trend is being led by companies involved in manufacturing electrical equipment, appliances and components; computer and electronic products; chemicals; transportation equipment; and medical equipment and supplies.2 CapEx spending here outside technology remains low, but that could change soon.

As for the energy grid, the United States has a deservedly terrible reputation. The demand for capital investment is only more pressing now, as the data centers that power AI are using tremendous amounts of energy. The incremental electricity consumption projected from 2024 to 2030 will be the equivalent of three times that of New York City.3 And re/onshoring manufacturing, as well as increasing electric vehicle usage, will only add to domestic energy consumption. Much of this cost will be borne by government-led initiatives, of course. But the private sector is contributing as well, in the power grid, in transmission and distribution, in pipelines, and on alternative energy sources, including natural gas, nuclear and renewables. Utilities across the country are looking to seize the opportunity to address an uptick in energy demand by targeting high-return investments in expanded capacity. At the same time, supporting the grid is an area of some bipartisan support, with proposed legislation released this past July.4

So, what is the risk of overspending and overbuilding? Will the payback on spending be high enough for the hyperscalers and the other big investors to earn an appropriate return on their considerable capital? In the interim, will the profits generated from AI among the end-users – the smaller companies actually deploying AI in their business practices – meet stock market analysts’ currently high expectations? At this rate, we’ll need to see a major shift in productivity and growth over the next decade or so to justify this spend. And to top it off, high PE multiples and the significant concentration in the S&P 500 index to the hyperscalers leading this investment gives us cause for concern.5

Profits are already showing up at the cloud service providers: Microsoft and IBM have both detailed a direct line to revenues from their massive capital spending, as they have been able to convince many of their customers to spend more on AI-enhanced products. Longer term, this cycle has one big advantage over past debt-fueled CapEx booms. The biggest spenders are the biggest and best capitalized companies in the world, with massive research and customer bases. They are primarily using operating cash flow, not debt, to fund AI-driven spending. They should have time to make sure that their investments pay off.

It is unclear yet whether AI-related productivity enhancements will be worth the cost for the average small- or medium-size company. Call centers, pricing algorithms, supply chain and inventory management, and improved customer interactions are among the many use cases posited, but all need time to be implemented before rates of return on investment become clear. Bigger picture, the prospect of autonomous vehicles, AI-enhanced robotics, new and faster research and development in healthcare, energy, space travel and more could have a massive impact on productivity.

As for dependencies, it’s difficult to argue that a more efficient power grid, a shift to greener energy and, eventually, shorter supply lines aren’t in our broader long-term economic interest anyway. This infrastructure needs to be built, regardless of the AI cycle, and a strong CapEx cycle generally bodes well for the economy. To date within energy infrastructure, we do not see signs of overbuilding or bubble economics. Indeed, the question here is whether the developments in these areas will proceed fast enough to support advances in technology. This is an important consideration as the AI investment cycle unfolds unpredictably in parallel.

We continue to believe that overall portfolio diversification, with exposure to cash, defensive and credit-sensitive fixed income, stocks and illiquid alternative investments, if appropriate, is the best risk mitigator. We are always mindful of having too much exposure to any single trend or investment thesis, regardless of the surrounding hype.

Brian Pollak and Michael Kirkbride are Partners and Portfolio Managers at Evercore Wealth Management. They can be contacted at, respectively, brian.pollak@evercore.com and michael.kirkbride@evercore.com.

Editor’s note: Investors interested in exposure to General Partner-led (“GP-led”) secondaries, as described by Nigel Dawn here, the global head of the Private Capital Advisory Group at Evercore, may be interested in single asset continuation vehicles.

Ricardo Lombardi, Global Head of Strategic Equity at ICG, provided these comments to Independent Thinking. Please note that the views of the external managers interviewed in Independent Thinking are their own and not necessarily those of Evercore Wealth Management.

Q: Let’s start with the basics: What is a single asset continuation investment vehicle?

A: These structures focus on situations in which the GP [the private equity General Partner] wants to keep a specific asset beyond the original investment timeline. As investors, we want to be confident that there is additional upside in the value of the business that can be generated with our capital.

Q: What makes for an attractive candidate?

A: Ideally, the underlying company asset is a market leader in an attractive, noncyclical and consolidating – but still fragmented – industry and is generating organic growth. We look for quality businesses with healthy profit margins and recurring revenues.

Q: Why should investors consider single asset continuation vehicles, as opposed to multi-asset vehicles?

A: In a multi-asset transaction, investors are likely buying assets that range in quality. While that does provide an element of diversification – and most established secondary buyers prefer them for that reason – the quality of single asset deals can be superior, given the right circumstances. After all, the transaction is driven by the sponsor’s interest in retaining a truly outstanding asset. If the buyer has a very disciplined approach to pricing and selection, single assets should have the potential to generate superior risk-adjusted returns.

Q: Any other considerations?

A: The single asset market has significant long-term growth potential because it’s still very small. However, the potential market is underpenetrated and growing – single asset continuation vehicles still represented only 3.8% of total private equity exits in 2023.1 We expect this market to continue growing, as private equity sponsors increasingly appreciate the attraction of the GP-led transactions from the perspective of both liquidity management and portfolio construction.

Q: Please describe your diligence and underwriting process.

A: Our team of direct buyout professionals has the skills to meet with management, visit sites, develop operational models, hire third-party consultants, and evaluate pricing and partnership structures. And we partner with well-regarded and established GPs who are known to us and have already achieved positive results with their asset.

Q: How do you think these GPs see ICG Strategic Equity? What are they looking for in a lead buyer?

A: The GP’s primary interest should be around fairness to its LPs, notably in process and price. Key considerations for the GP should include certainty and speed of execution, as well as stability for themselves and the asset’s management team. We provide a one-stop solution in that we typically commit all of the required capital for the deal, which enables the GP to engage with just one buyer, instead of a syndicate of buyers. That makes the process much simpler and resource-effective.

Q: How are market conditions now? What are you focused on at present?

A: So far in 2024, we are seeing one of the strongest pipelines of deal activity we have ever had, both across North America and western Europe. We continue to see increased adoption by GPs that have never pursued GP-led transactions before, so the addressable market is growing. At the same time, at ICG Strategic Equity we continue to be focused on growing the quantum of capital that can be transacted with a sole buyer, and pursuing continuation vehicle sizes up to $1.5 billion.

With the macro backdrop continuing to drive more GPs to want to create liquidity for flagship funds, plus LPs continuing to want liquidity and increased capital flowing into the market to execute on these deals, we are bullish about the outlook for both the volume and scale of transactions going forward.

For further information, please contact Evercore Wealth Management Partner and Portfolio Manager Stephanie Hackett at stephanie.hackett@evercore.com.

Editor’s note: Nigel Dawn is the global head of the Private Capital Advisory Group at Evercore, leading a global team in originating and executing secondary market transactions for owners and managers of private financial assets (private equity, private infrastructure, and others). Clients include both General Partners, or GPs, and Limited Partners, or LPs, such as financial institutions, university endowments, publicly quoted investment vehicles, and public pensions. Here are some highlights from a recent conversation with Independent Thinking.

Q: Let’s first address your market from the perspective of high net worth investors and related nonprofits, notably foundations and endowments. Why should private investors be interested in the secondary markets?

A: I think the attractiveness of this market is in the potential returns. Effectively, you get to buy private equity at “spot” prices. [Editor’s note: Spot prices are the current liquid market prices of securities.] That’s much better than the primary private equity market where, no matter how good the manager, it’s still 100 cents on the dollar when you are raising a new fund. Also, this is a market where you can deploy your capital relatively quickly and get it back quickly, given you are buying mature assets.

Q: It’s also a market that many investors don’t fully understand, perhaps because it’s changed so much. How do you see the evolution of continuation funds, the strategy that you are known for developing?

A: The secondaries market has pivoted from propping up low-quality GPs with challenged assets to enabling the very best GPs retain their best assets. [Editor’s note: A General Partner is the manager responsible for running a fund.] The appetite to repurpose the continuation fund structure was around for some time, but the pandemic was a catalyst that accelerated widespread adoption.

GPs needed to find a way to ‘buy time’, while providing money back to their investors and while raising new money to support their best companies. We saw that continuation funds could enable them to retain their best companies in all market conditions and offer their investors the choice of selling and receiving cash or continuing to invest in those companies alongside the GP.