close

In times of uncertainty – economic, political, or personal – it’s natural to worry. Even those who are financially well-off aren’t immune to the “what-ifs” that keep us up at night. So, what’s the antidote? It starts with building the right team of trusted advisors and continues with engaging in open, honest conversations.

Easier said than done, of course. In my 50 years as a wealth manager, I’ve seen some shocking violations of trust. And we’ve all heard the old social rule: Don’t talk about sex, money, or politics. While the world has changed, that taboo still lingers. I don’t always feel that I can talk openly about my finances with my friends or even my family. And I know I’m not alone in that.

But trust is essential, particularly when the going gets tough – in our society, in the markets, or in our personal lives. We sell ourselves short if we don’t trust our family and our advisors, our doctors, teachers, coaches – the people invested in our lives and those of our families. That’s why it’s important to determine if someone is worth trusting and, that done, to create a safe space where transparency is welcome.

Consider health, another traditionally private topic. Our long-term medical well-being depends on trust as well as luck. A good physician, one who really listens, needs patients to speak up, to share their concerns, take the necessary tests, discuss results, follow advice, and seek a second opinion if the diagnosis is serious. (That’s not disloyal – it’s wise.)

I would never rely on self-diagnosis to deal with a serious medical condition, even with the help of Doctor Google. That’s good practice for other areas of life too. While I might consider that my long experience as wealth manager has made me an expert on financial matters, I recognize the value of collaboration in evaluating my own options and forming my own decisions. Outside perspective and expertise are essential.

That’s why when I’m asked, “What’s your best advice for the current market?”, my answer is always the same: It depends on the full financial picture. A good advisor needs to have a full understanding of individual and family long-term goals and current concerns, assets and liabilities, income and spending patterns, health considerations, family dynamics and legacy intentions.

The real antidote to uncertainty isn’t just financial stability. It’s knowing we’re not navigating life alone. Build a circle of trusted advisors: a physician, a financial advisor, an accountant, and a lawyer. Give them the full picture, share questions and concerns, ask for second options. If we let our advisors help, we can focus on what matters most.

Uncertainty will always be with us. But with the right team and the right conversations, we can face it with confidence and calm. It’s never too late to build the right team – and never too early to stop worrying alone.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

Over $100 trillion in assets will be transferred within 25 years in the United States.1 At 77 years old, I have to consider that my legacy will be included in the total (although more on that later). In any case, it should be the largest intergenerational transfer of assets on record. Will it be successful? Will it support happy, successful families that contribute to our society?

I sure hope so. And I know that our clients do too. In my 50-plus years in the wealth management business, I’ve seen a lot, enough to develop some ideas on best practices for successful wealth transfer. Here are a few, in chronological order: (A note to my peers: If you’ve missed a few steps with your own children, there’s still time to try to apply what you’ve learned, as appropriate, to grandchildren.)

Start early

Many families wait until it’s too late to discuss finances; very few start too early. Spouses need to develop shared goals for raising successful children, financially and otherwise, before the tooth fairy’s first dollar is spent, and to keep communicating as the family evolves. This becomes more challenging in the event of divorce or within blended families, but it’s still doable. Advisors can help.

Educating young children about money and helping them develop a healthy perspective on their privilege is a gift, one that can be more valuable than the assets themselves. Paid work in addition to chores, modest allowances, small contributions to charities that interest them; these can all serve as teaching aids. So too can a robust “no,” even when finances allow otherwise. The ability to distinguish between needs and wants is invaluable.

As children grow, they will ask uncomfortable questions. And for affluent families, one of the questions is likely to be: “Are we rich?” They are already getting a sense of their circumstances, measuring their experiences and resources against those of their peers. They need context for that, something that could be provided by describing wealth as a tool for security and opportunity, not just luxury.

Consider differences

Every parent with more than one child, every grandparent with multiple grandchildren (and every sibling, for that matter), knows how different individuals within the same family can be. Sometimes it seems that the closer in age they are, the more unlike each other the children become. It makes sense to tailor decisions about education, work and other activities to each child’s unique circumstances. For example, part-time work can help build character, but for an athlete, theater kid, or someone with special needs, there may be other priorities.

There will be differences within communities too. But there’s arguably no better way to immunize a child to what has been described as “affluenza” than reminding them they don’t have to follow the crowd. That was hard enough when my own children were young; it’s going to be more difficult – and more important – as this wave of wealth flows in within an environment of social media.

Invest in the next generation

As children grow, particularly during adolescence, it’s a good idea to gradually increase transparency around family wealth. Most of our clients aim to provide children with a debt-free college education. This is a wonderful opportunity for grandparents to help, especially as direct payment of tuition is free of any gift tax.

Other tax effective ways to share wealth include taking advantage of the annual gift tax exclusion (currently $19,000 per person in 2025) by making direct gifts to older children and gifts in trust for younger children and grandchildren. Families with significant wealth can use the lifetime estate and gift tax exemption (currently $13.99 million per person). Larger gifts are typically placed in trusts to provide structured management and tax benefits. (Read “Choosing a Charitable Vehicle” to see which charitable giving vehicle might be right for your family).

Adult children can benefit from carefully considered support as well. Graduate educations, investments in startups and deposits on first homes are the most obvious examples that many, but by no means all, high net worth families consider funding. It is a very personal choice and one that should be made in close consultation with advisors who know the family dynamics.

Finally, for people my age, it makes sense to share transfer plans with middle-aged children, to aid in their own long-term planning.

Keep both eyes open

Change is inevitable. While we are already seeing evidence of this great wealth transfer, we are mindful that life expectancy is rising and that the additional years can be among the most expensive – which brings me back to my own expectations. With parents who lived into their late 90s and each generation living longer than the last, my wife and I need to consider our own future as well as that of our children and grandchildren.

No one should transfer more than they are comfortable giving or give more than (or before) their heirs will benefit from receiving. Again, trusts can play a critical role in successful wealth transfer, as can choosing the right personal and corporate trustee. Families have other options as well. It is interesting to note that in addition to the massive intergenerational wealth transfer, another $18 trillion is expected to go to charities over the next quarter-century.2 Proper planning, education and communication are essential in making (and revisiting) related decisions.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

Trusts are commonly used by high net worth and ultra high net worth families to preserve assets for a spouse or future generations in a tax-efficient manner, shelter trust assets from future creditors or divorce, and provide for a family member with special needs. Here are some of my thoughts on best practices when using trusts:

Consider granting your beneficiaries a limited power of appointment over trust assets, if that is appropriate in the context of your wishes. This allows them to modify trusts terms if their circumstances change.

By following these best practices, you can create a trust structure that aligns with your objectives, protects your assets, and supports future generations effectively.

— JM

David Attenborough continues to explore at 98; Warren Buffett continues to invest at 94; and Mick Jagger still “can’t get no satisfaction” at 81. We’ve been hearing so much about what scientists describe as “super agers,” those with the mental and/or physical capacity of people decades younger, that we are almost losing perspective on the normal aging process. The election has served as a reminder, with one of the two oldest major-party presidential candidates in U.S. history dropping out.

Aging is a fact of life. In my 77th year, I hiked the wilds of Alaska and took the photo above, received apparently effective treatment for prostate cancer, underwent a shoulder replacement, and photographed Yellowstone with my siblings. My 70s are almost as eventful and volatile as my 20s! I am enjoying the good times, while searching for grace amid the challenges. In short, I accept that stuff will happen. I know some physical frailty is on the way, and I am watchful for other signs of weakness.

Most of us would like to retain control over our lives, but there is no doubt that we become more vulnerable. Stuff is happening now to the so-called Silent Generation and the vanguard of my giant Baby Boomer generation. In my communities in Florida and New York, and in discussions with our older clients (and their adult children) across the country, I am hearing the same questions, the same concerns:

How can I protect myself as I age? How can I protect my spouse? What can I do for my children and grandchildren? What can I do for my community, for the causes I care about? What is going to happen in this election? In the world?

I, along with my colleagues at Evercore Wealth Management and Evercore Trust Company, can help address most of these questions (see the article by Ross Saia and a few additional suggestions on aging well by me, below). Thoughtful planning, appropriate risk-adjusted investing, and truly personal fiduciary care will go a long way for our clients and their families in preparing for the future, whatever it holds.

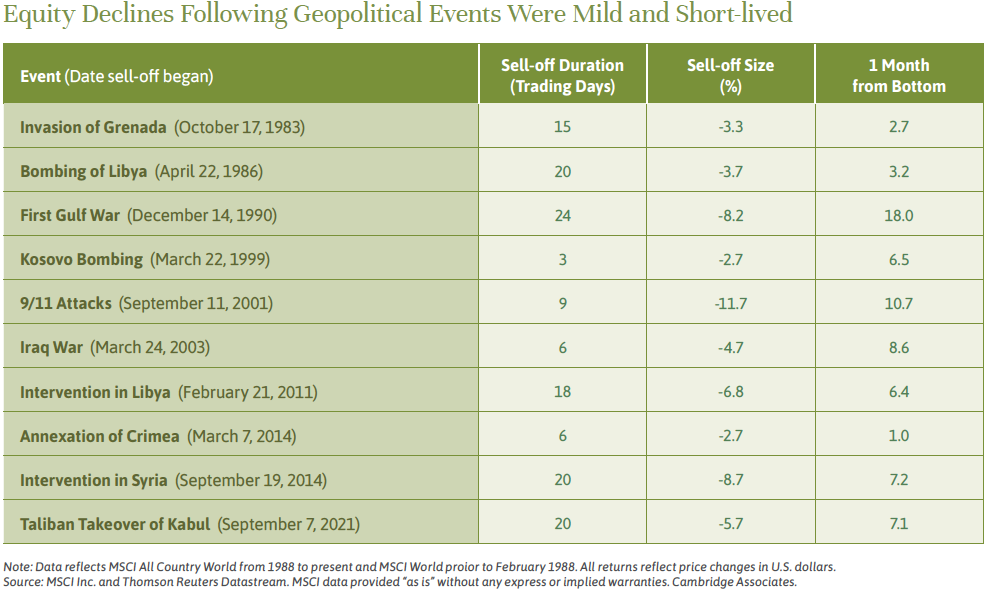

As for those last two questions about the state of our world, I can’t be sure about those, although I wish I could. We will be discussing the election in webinars and client events in the coming months. In the interim, please take a look at Brian Pollak’s article in the previous edition of Independent Thinking, on the surprisingly low impact elections and geopolitical events generally have on the markets. There are other issues at stake, of course, but this may be one consolation.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

I like to think I chose my parents wisely, but of course I’ve been lucky: My parents, grandparents and some great-grandparents lived into their 90s in relatively good shape for all but the last few years. In a similar vein, the affluent are generally lucky too, with the top 1% of American women and men now living to an average 88.9 years and 87.3 years, respectively.

Habits count too, though. So here are a few suggestions:

Ace the basics.

Recruit your team and give them the tools to succeed.

Keep an eye on the long term.

Successful aging is hard work. But it is famously better than the alternative.

— JM

“How do I educate my spouse about our wealth?” “How much do our children need to know?” Estate planning discussions tend to focus on the distribution of assets. But it’s the answer to these two questions that will often determine how effective the plan proves to be.

While every family, every situation is different, a collaborative approach is usually best, both between spouses and between parents and adult children.

Even when spouses have shared goals regarding the disposition of their assets, engaging the less financially knowledgeable spouse at their level of understanding and interests and educating them about the potential financial trade-offs can improve the outcome. A trained advisor should be able to make sense of the SLATs, GRATs, CLATs and DINGs of estate planning while helping to foster a sense of unity and preparedness, which is vital in managing assets and addressing future uncertainties.1

The more informed children are about their likely inheritance, the better choices they can make about their own finances, including saving, borrowing and spending on their own children. Involving adult children in the planning process can also provide them with a sense of inclusion and responsibility and help them become familiar with the financial and legal aspects of estate planning. Effective family governance and legacy goals can be much more attainable if family members feel informed and engaged.

Even in blended families, where sources of wealth vary and where profound differences can exist between levels of wealth, informed planning can promote a sense of unity and preparedness.

Perhaps equally important is the need for transparency. Honest conversations about estate planning can help manage expectations and reduce potential tensions, misunderstandings, conflicts and even legal disputes. Explaining the rationale behind decisions, whether it’s the distribution of assets, the establishment of trusts or assignment of fiduciary responsibilities (i.e., trustee, executor or personal representative appointments), can be very helpful. Heirs need to know the “why,” not just the “what” and “how much” while there’s still time to have those conversations.

Admittedly, there are situations where sharing sensitive information is not advisable or appropriate. In such cases, a letter of wishes can be placed among estate planning documents explaining the rationale behind decisions and outlining expectations. In any event, families with significant wealth should consider appointing a corporate trustee or co-trustee to educate and support an individual trustee.

Ultimately, estate planning is about more than just the distribution of assets; it’s about ensuring that the family is prepared for the future and that your wishes are respected. Taking the time to educate a spouse and involve adult children in the process can make a world of difference.

Ross Saia is a Partner and Wealth & Fiduciary Advisor at Evercore Wealth Management and Evercore Trust Company. He can be contacted at ross.saia@evercore.com.

As a late-in-life Pilates enthusiast, I’ve learned the importance of alignment; all it takes is one body part to fall out of whack, and all the other bones, joints and muscles soon feel the strain. Adjust that part while there’s still time, and the whole can come together again.

The same is true for managing wealth – especially in, or ahead of, retirement. We need to make the right corrections, aligning our short-term spending (on ourselves and others) with our long-term lifestyle needs and our legacy goals. The choices are very personal and entirely up to us, but we do need to understand the interconnectivity.

Want to buy a boat? Join a new club? Spend a year traveling the globe in style? Terrific – that sounds like a lot of fun. Family temptations may loom large too, as helping to fund homes or start-up businesses for children, and educations and other enriching experiences for grandchildren, can feel very satisfying. And more time to engage with nonprofits is likely to inspire more generous gifts.

These are all wonderful ways to spend, of course. But they will be more enjoyable for those comfortable with the tradeoffs. And there are usually tradeoffs, no matter how large the portfolio. Take a look at the chart below. Here’s what seemingly small differences in spending rates can do to the same $20 million portfolio.

Most advisors plan based on a proportion of pre-retirement income, typically 70%, or current reported spending, assuming that it will drop off in retirement. And just about all base their estimates on average life expectancy and inflation rates.

But I am certain that for many of our clients, spending does not drop off in retirement. Sure, we save a few bucks on commuting, and we don’t need any more suits (who does, nowadays?). But that’s a drop in the proverbial bucket for the high net worth and ultra-high net worth families. In my experience, most of us tend to underestimate our spending, both before and into retirement. The exceptions become the rule; the once-in-a-lifetime experience is quickly followed by another (or shared with family). In short, there is always going to be another one-off expenditure.

Not only are we having more fun than our own parents or grandparents did, but we are also living significantly longer. Indeed, the top 1% of Americans by wealth at age 65 can now reasonably expect to live well for another 20 or so years, thanks to the miracles of modern medicine. And there will still come a time when our lifestyle spending shifts to medical and care-related expenses.

As for inflation, it’s easy to underestimate that as well, particularly as prices for goods and services valued by the high net worth consumers appear to be rising relatively fast. (Please see my related article here).

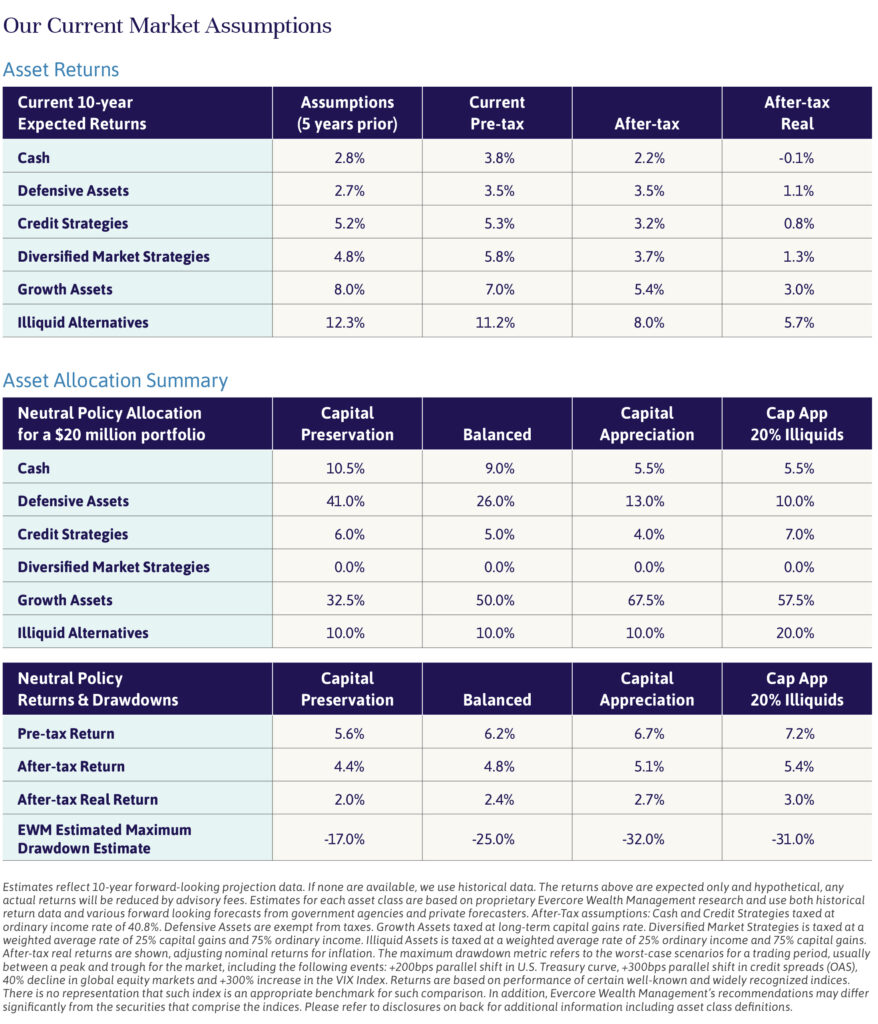

So, how do we find financial balance in our so-called golden years? The starting point is a thorough lifestyle analysis, to evaluate current and future spending needs, mindful of the need to fund potentially very long lives. These calculations should take into consideration capital market return assumptions, as well as estimated inflation and tax rates, and individual tolerance for market and liquidity risk. (For our current capital market return assumptions, see chart below.)

We can then evaluate the likelihood of reaching other goals, including wealth transfers (a pressing topic for clients who have yet to take advantage of at least part of the $27.2 gift tax exemption before it sunsets next year). And if the numbers aren’t aligned to those goals – or if the goals themselves have changed – we can recalibrate the wealth plan. Trim (or occasionally, increase) spending, take on more investment risk, revisit legacy goals – one or a combination of these and other tactics can support a long and happy retirement.

As I’ve discovered in Pilates, it is best to address weaknesses earlier. But it’s never too late to make improvements.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

A friend tells me that she now spends the evenings watching I Love Lucy reruns to take her mind off the news. I can think of worse coping mechanisms.

The headlines are mostly grim, and I know that many of my generation worry most about what they may mean for our children and grandchildren. But as we are told on every flight, we must first secure our own oxygen mask before helping others. So here are a few personal reflections, in the hope that they may prove useful. In my experience, testing – and retesting – our predilections and tolerance for risk is the best way we can prepare for the future.

Politics: We can control our media exposure, staying informed without doom scrolling or rewarding those that peddle hype or falsehoods. And we can engage, as we wish our politicians did, across the aisle – getting to know people with different views. At the least, we’ll gain insight. At best, we’ll find common ground and do some good in this world. And, of course, we can vote.

Health: It wasn’t long ago that the news was dominated by a single headline – an experience that has made us all more aware of our health. Diet, exercise, regular checkups, vaccines and, increasingly, technology can help position us to take full advantage of the trend to increased longevity. (Contact your advisor to view my discussion about “silver tech” with Andy Miller of the AARP’s innovation unit). But 100-year life spans need to be protected and funded. Long-term healthcare policies, a healthcare proxy, durable power of attorney, and a revocable trust, which allows a designated successor trustee to take care of finances in the event of cognitive impairment, can all play important roles in protecting us as we age.

Home: In theory, a single storm could take out both of my houses, on the east coast of Florida and in Long Island. But for me, five days of pure terror are so far a reasonable price to pay for 360 days of joy. Having made that choice, there’s a limit to how much I can control, beyond hoping that personal lifestyle, philanthropic, investing, and voting choices are the right ones. But I can keep up to date with relevant technological, landscaping and maintenance techniques. And I can make sound decisions on insurance, to the extent that market conditions allow. (Contact your advisor if you would like to view our recent webinar on property casualty coverage.)

Personal finances: I have spent the last 50 years worrying about financial risks for clients, institutions, and my family. In that time, there have been six bear markets, with an average drawdown of 41%, and an average recovery time of 2.8 years. Understanding our risk tolerance – where we fall in the “eat well versus sleep well” scale – is a very personal determination, and one that is likely to evolve. Some clients wish to take only limited risk and are content with 100% of their assets allocated to a laddered bond portfolio; others simply don’t invest in bonds because of the relatively low return potential. Most of us are somewhere in the middle.

Personally, at this stage in my life, I do not want to have a pit in my stomach during a significant drawdown. I therefore maintain sufficient cash and bonds to cover five years of spending. On that basis, I am more aggressive with my other assets, investing in illiquid private equity and real estate where I personally expect higher returns. When the drawdown does occur – because it will – I can tap my reserves for spending and meeting capital calls.

Perspective: Attitude really is everything, so we should all strive to keep calm and carry on, come what may. I’ve learned, on occasion the hard way, that keeping busy and optimistic is the best way to live. So, when headlines feel overwhelming, try looking for the good. It’s there too.

“I’m not funny,” Lucille Ball once said. “What I am is brave.”

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

Baby Boomers have it pretty good. By and large, we’ve enjoyed high and full employment, exciting technological advances and extraordinary asset growth. And the best may still be to come, as affluent Americans live longer and heathier lives. Many of my generation are still working; others have embarked on retirements rich with possibilities. And a growing number of us are shaping lives that blend work and myriad other interests. Really, what do we have to complain about?

Well, maybe we can complain about inflation. While it’s ebbed considerably in recent weeks – and is nowhere near the double-digit rates we in the vanguard of our generation experienced in the 1970s when we started working – prices still seem high, notably for the goods and services that appeal to high net worth consumers. Our generation has partly brought this on ourselves, as we seem to be busy spending at least some of the $78.3 trillion gross that U.S. Baby Boomers have accumulated (see Where Are the Kids? Demographics in the United States by John Apruzzese here). Our unprecedented numbers and wealth are driving prices higher for the things and experiences that we tend to value.

Take travel, for instance. Prices haven’t been this high in years, not because business travelers have returned (they haven’t), but because well-off leisure travelers have taken their place, willing to pay through the nose to avoid the worst of the airport crush and get some rest or experience adventure. Planes are packed, as are upmarket hotels, resorts, restaurants, and theaters and concert halls. I didn’t pay tens of thousands of dollars to see Taylor Swift, although I understand that a surprising number of Baby Boomers did, but I did pay about twice what I expected on a recent trip to Paris and Berlin.

Indeed, just about everything that high net worth Baby Boomers could want seems more expensive now. Golf club memberships, luxury clothing, accessories and cars, tutoring and summer camps; name it and it probably costs far more now. Property casualty insurance is another striking cost for high net worth homeowners, with premiums for upscale homes rising more than 10% a year in coastal communities and those vulnerable to wildfires. (We hosted a webinar on just this subject on June 22; contact your advisor for replay details.) It’s difficult to ascertain just how much the high net worth rate of inflation is, of course, since people make very different choices, but for argument’s sake, let’s say it’s twice the rate of inflation generally. Personally, I think that’s conservative.

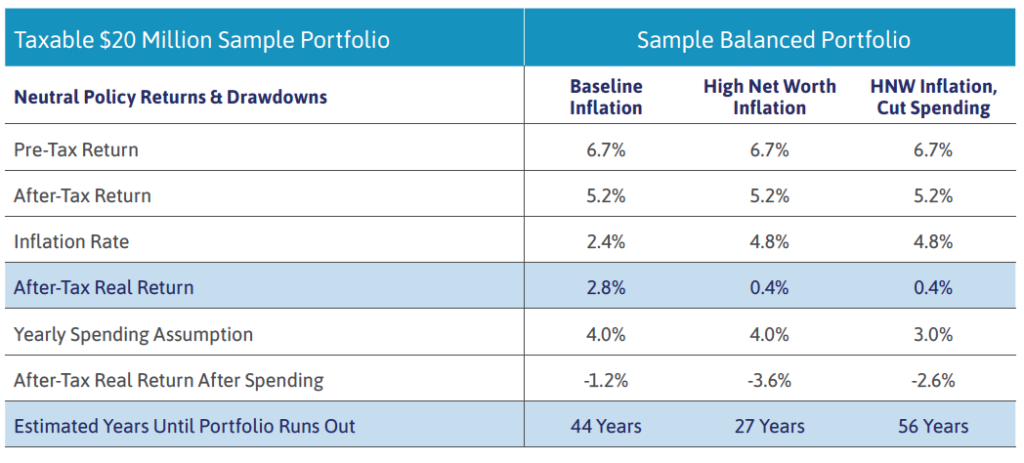

So, what does that mean for portfolios? Please see the piece below by Jake Stoiber with a couple of examples of a balanced $20 million portfolio – one based on a typical spending rate of 4% and another on a more frugal 3% of the portfolio. (These are all for New York state-based clients for tax purposes; figures will change depending on domicile and other factors.) Clearly, spending has an enormous impact on our assets, far more so than our attitudes toward risks. And spending on more inflated items has that much greater of an impact. Interestingly, when we ran these same numbers for a more aggressive accumulation portfolio, the differences were less significant.

This period of still relatively high inflation won’t last forever. Other periods of extended inflation have lasted on average for four years, and the overall inflation rate of the past 75 years is 2.5%. For those still earning, chances are you’ll be able to ride this period out, if you plan accordingly. But for the many Boomers in or approaching retirement, it’s important to consider the overall impact on portfolios of rising spending – notably on the luxury goods and services – in the context of long-term lifestyle and wealth transfer plans.

Inflation can undermine our plans for ourselves and for the people and causes we care for. It is important to budget realistically and to take into account that your spending may be rising faster than the rate of inflation. If you are spending more than our projected capital market returns, we encourage you to plan carefully. The real impact on portfolios can be managed, through close planning with a trusted wealth management team. It may be that you choose to curtail your spending, or take on more portfolio risk, or decide on a combination of both. Alternatively, you may want to revisit your goals, drawing down more of your assets if necessary to maintain your lifestyle and adjusting bequests to heirs and charity. The decision will be very personal, so it’s important to know what to expect – and exactly what your options are.

Most of our clients like to eat well and sleep well. And with proper planning, we believe they will be able to continue to do just that. Successful members of my generation – who have had it so good for so long and still have so much to look forward to – will want to keep it that way.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company, N.A. He can be contacted at maurer@evercore.com.

What does inflation do to a portfolio? Using our updated capital market return assumptions and our baseline sample balanced portfolio as a starting point, we put some numbers behind the impact on a hypothetical $20 million portfolio, given various inflation, spending and risk assumptions. It is important to remember that return expectations can change, and as Jeff Maurer writes above, risk appetites and spending habits can always be tailored. At current inflation rates, a portfolio can outlast moderate spending; it may be more significantly eroded – or even exhausted – by spending more typical of high net worth Baby Boomers, especially the younger members of the generation, still in their late 50s and 60s.

Further, shifting into a more aggressive portfolio doesn’t buy investors much more time – just two years – and exposes investors to greater drawdowns, which can also influence a portfolio’s drawdown path. At that point, $20 million may not feel like as much as it should. However, decreasing spending by just 1% can buy an extra decade or more. Periods of high inflation may be good opportunities to reduce spending, particularly on luxury goods and services, and/or to revisit long-term financial goals.

Two companies are created by men born 111 years apart. The first, Cargill, a producer and distributor of agricultural products, becomes one of the largest and most successful private companies in the world, still family owned. The other, Microsoft – well, you know. So, what do these two companies have in common, apart from being built by men named William? They both struggled and ultimately succeeded, in very different ways, with the issue that vexes every lasting concern – succession.

As an advisor for 50 years to business owners, executives, and multigenerational families, I have observed that succession planning should be viewed not as a one-time event, but as a continuous, evolving process. Most big companies develop a pool of talent and observe that talent over time. If the company or family is doing well, internal promotions can be the best path to continuing success. If the business is faltering, turning to the outside generally produces better outcomes. According to a recent analysis published in the Harvard Business Review, the amount of market value wiped out by badly managed CEO and C-suite transitions in the S&P 1500 is close to $1 trillion a year. The report estimated that better succession planning could add 20% to 25% to company valuations and investor returns.

1That’s true for small businesses and for families too, as succession planning enables functions to be passed from one leader to another, recruiting from the outside and appointing independent trustees as needed. When the 74-year-old Charles is crowned King of what his father described as “the firm” on May 6, it will mark the latest stage in a planning process that really started in 871 with the succession of Alfred the Great. (It may also highlight some of the pitfalls of designating a successor merely by birthright.) While most of us don’t aspire to this grandeur, many of us would like to identify the right future stewards of our wealth for our families and our businesses.

On a personal note, succession planning was a big issue at my earlier firm, where over my first decade there were four chief executives, which during that time diminished the value of the firm. But the last of the four was a great success, and when he reached mandatory retirement age at 65, he promoted me to president at age 42, as part of a well-planned succession process. All of this was very much on my mind when I helped found Evercore Wealth Management at the age of 61, with a view to running the firm for 10 years. Over time, I worked with Evercore senior management to identify and prepare my successor. When the time came, we had a smooth and successful transition to Chris Zander, one of our founding partners, and I was able to stay on as a nonexecutive chairman, which works well for us and, I believe, for our clients.

In a similar vein, we actively and continuously plan for the evolution of our firm, as partners and other professionals retire – to ensure that our values and culture, as well as our expertise, are carried forward, and our clients have time to work with and approve our suggested successors. And we encourage our clients to ensure that their other advisors – whether attorneys, accountants, doctors and the like – also have succession plans in place. You probably don’t want to get old with your dentist.

As for the two Williams and their somewhat larger companies, I imagine that William Wallace Cargill would be gratified to know that 158 years after its founding as an Iowa grain-storage business, his company remains in family hands, perhaps because subsequent generations realized that its affairs had become far too complex and turned to outside management starting in the 1960s. Indeed, 14 members appear to be billionaires, making the family the fourth wealthiest in the United States. If Cargill were a public company, it would be among the largest in the country and perhaps among the most controversial – but that’s another story.

William Henry Gates III, better known as Bill, is probably relieved to focus on his philanthropic interests after the six-month crisis back in 2013 when his successor, Steve Ballmer, announced that he was quitting and the scramble for his replacement resulted in the internal promotion of Satya Nadella, a 21-year veteran of the firm – and a subsequent 30% gain in the company’s stock price over the next 16 months.2 Two very different companies, two very different succession solutions after periods of arguably unnecessary turmoil, but in the end the right choice for each.

In our view, the earlier we plan for succession – and the more we continue to invest in it – the better the outcome.

Jeff Maurer is the Chairman (and former CEO) of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

There are two types of financial plans: the ones that sit in the back of a drawer (or the email box equivalent), and the ones that are regularly revisited and refreshed. We are proponents of the latter. Proper financial planning begins and continues with conversation, at least every year and often more frequently, as family, business, regulatory and market conditions evolve. Current financial circumstances, attitudes to risk, and long-term goals are likely to be the major topics. But as much of the advisor’s work is in getting the details right, there’s a lot more to discuss too.

What are the best steps to take now to secure your lifestyle and protect you as you age? How will a new venture, gift or donation impact your liquidity needs? What are the tax implications for your estate?

It’s a lot to consider. Done right, regular financial modeling will enable you to understand the long-term implications of spending patterns on your portfolio, taking into account capital market assumptions embedded within various asset allocation decisions. You could review Monte-Carlo simulations, which predict the probability of a variety of outcomes across a range of variables, but you may be better served by a thorough drawdown analysis that illustrates what may happen to your portfolio in a variety of market conditions, such as a repeat of the 2008-2009 financial recession, the brief 2020 COVID meltdown, or the 2022 inflation-related drawdown.

If the results are too much to stomach, you’ll want to consider a less risky portfolio, and the consequences to income and growth that will likely flow from that decision. Either way, you’ll probably want to maintain the equivalent of three to five years in cash and defensive assets. You may establish a specific reserve fund or strategy if there’s a known risk on the horizon. For example, if your plan is dependent on continued employment income from you and/or your spouse, have you assessed the need for disability and/or life insurance to protect that income stream?

Once the asset allocation is agreed upon, the next (but not last) step is implementation. Whether putting cash to work to build out agreed asset allocations, transitioning an existing portfolio, or managing around a concentrated holding, the investment process should be methodical and transparent.

A financial plan is only as good as the inputs used and the assumptions made – and life, as we all know, can be unpredictable. As such, it is essential to revisit the plan regularly, ensuring that you are on track to meet your goals, and accounting for evolving family and market conditions, always mindful of potential tax consequences. Recent losses in the markets and spikes in inflation make this a particularly important time to revisit your plans. And of course, every major life change – marriage, birth of a child, retirement – is a reason to check back in with your advisors and adjust the plan appropriately.

A comprehensive and thoughtfully managed financial plan shouldn’t collect literal or virtual dust. It should evolve, providing inspiration and peace of mind.

Tom Olchon is a Managing Director and Wealth & Fiduciary Advisor at Evercore Wealth Management and Evercore Trust Company. He can be contacted at thomas.olchon@evercore.com.

If age is an attitude, then I feel pretty good. When I think back to my parents at this age, it seems to me that they were somehow much older than I am now. I’m more active, more engaged, and more physically fit. While they had rewarding lives, mine just seems more fun. Perhaps my own children and grandchildren will feel that way too. If 75 is the new 60 now, imagine what the experience of future generations could be.

I’ll never know, of course. But as two-thirds of my life has been spent in the wealth management business, I do know one thing: Successful aging is greatly influenced by financial health and a good attitude, as well as by physical and mental health, and relationships. Federal longevity statistics bear that out at the most fundamental level, with the top one percent of Americans by wealth living longer than the average, and life expectancy across the board increasing with income.

Wealth is not a panacea for the worries that come with age, of course. But, if managed correctly, it can buy at least some peace of mind and, when needed, the best medical care. (Of course, a healthy diet, not smoking, exercising, and only light use of alcohol also help.) Here are three current examples, much in my thoughts at present.

First, how can anyone – especially people who like to live well – afford to live to 100 years old, while still meeting important family and philanthropic goals? As Wealth & Fiduciary Advisor Tom Olchon discusses in his article, Financial Planning: More Than Investing, planning for a very long life starts and continues with rigorous financial analysis, regular risk assessments, and steady fiduciary oversight. As I round what I hope is only third base, my wish is to keep running in good health and with good cognition. But I have backup plans in place too, including a revocable trust, appropriate powers of attorney and health care proxies, a living will, and a good team of wealth and health advisors.

Second, how can we remain resilient and keep having fun through inevitable and often brutal market drawdowns? There have been 20 bear markets since 1929, with an average drawdown peak-to-trough of 37% and an average 3.3 – year recovery time. My advice remains the same as it was at the beginning of this bear market: Don’t panic and stay the course. Maintain a balanced portfolio with sufficient cash and defensive assets to ride out the hard times and be in a position to capture the market upside over the long term.

Third, how can we share our good fortune with our children and grandchildren, without inadvertently depriving them of the satisfactions of challenge and accomplishment? Watching my eldest grandchild preparing to head off to college reinforces my view that education is the greatest gift we can give those we love. (Anyone who wants to learn more should view Comprehensive Lifestyle Planning: The Cost of Education by Ashley Ferriello, a Partner and Wealth & Fiduciary Advisor at our firm, who describes some of the tax-efficient and satisfying ways in which to fund or contribute to an education.)

That view – that education makes a fine gift – is widely shared, I know. I haven’t seen much consensus beyond it, however. If, when and how to transfer assets to children and grandchildren is one of the most dynamic and challenging discussions in our work, and no two families have the same opinion. That’s why we are hosting a webinar on December 15, 2022, titled Enough, but Not Too Much: Raising Independent Children in an Affluent Environment. Please join it, if you can.

Attitude, said Winston Churchill, is a little thing that makes a big difference. Multiple studies have drawn a connection between maintaining a positive attitude and aging with resiliency. I should add that anyone who reaches this age in good health, with strong relationships and solid finances, has reason to feel enormously grateful. I know I do.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

In the spirit of transparency, and because we believe it’s the best estimate of portfolio risk, Evercore Wealth Management attempts to show clients an estimated maximum drawdown for their portfolios, from market peak to trough.

We start with basic assumptions, based on historical data, for each of our asset classes: Cash, Defensive Assets, Credit Strategies, Diversified Market Strategies, and Growth Assets. And we test those assumptions, effectively shocking them by modeling across a range of market scenarios. For example, how much could yields rise? What if they rise across the entire curve? How much do credit spreads widen? What is the potential relationship between U.S. and international stock performance?

We then multiply these adjusted assumptions for each asset class by the weights we allocate to them in our sample portfolios or investment objective guidance. The result is our maximum drawdown estimate, currently 25% for a balanced portfolio. It’s worth noting that we calculate the drawdown in our sample balanced account as though we do not own illiquid alternative assets. We do this because there is a lag in illiquid manager performance reporting, and excluding these assets seems to us to be the more conservative approach. We believe investors with illiquid growth assets should, over time, expect a similar drawdown.

We review and, if necessary, revise, these assumptions at the same time we update our long-term capital market assumptions, and as circumstances warrant. This review also gives us a chance to compare our estimates to previous market selloffs at both the sample portfolio level and the individual asset class level to make sure our assumptions are reasonable in practice.

In the 13 years since our firm’s inception, we have never breached our maximum drawdown estimate. Even the Great Recession downturn of 2007-2009, which forged our approach, remained within our expectations. The 2020 post-COVID shutdown market plunge came close, but in the end it held. We believe our estimated drawdown analysis is a good tool that allows us to advise our clients to ride out down markets and allows us to plan and invest with confidence in all market conditions.

Bear markets are inevitable, painful and, with proper planning, manageable. This is my eighth bear market in my 52 years as a wealth manager. The prior ones averaged a peak-to-trough drawdown of 41% in stocks and 25% in balanced portfolios (60% in stocks, 40% in bonds), well in excess of the 20% drawdown that defines a bear market. Each experience was unique: The 2020 pandemic bear market lasted just 33 days, compared with the 32-month average; others dragged on for years.

By our current assumptions, as described by Jake Stoiber here, we believe the greatest potential risk to a traditional balanced portfolio is a 25% drawdown. Most bear markets come nowhere near that, but the short dramatic plunge in March 2020 took us right to the edge of our expectations, with a record 33% drop for stocks from peak to trough and an estimated 22% for our balanced composite.

So how do we manage assets through bear markets? We start by revisiting our clients’ risk tolerance levels. For those in or approaching retirement or who rely on their portfolios for spending, we believe a properly diversified account should aim to have at least 20%-25% in defensive assets or cash. That allocation, along with normal portfolio income, should allow families to cover four to six years of spending including capital calls. (It’s also worth noting that while no one can control bear markets, we can all control, at least to some degree, our spending.)

If that sounds like a lot, consider that it should enable investors to ride out market drawdowns, avoiding permanent loss of capital through forced sales at depressed prices. An investor who sold a million dollars’ worth of shares in the S&P 500 index in March 2020 not only had to pay taxes on the embedded gains, but also lost out on the subsequent appreciation. The same position would be worth $1.75 million today.1

Once we determine the appropriate asset allocation, we are generally slow to make strategic changes to the portfolio unless our view of long-term asset class returns or volatility changes. Of course, as John Apruzzese describes here, we are always looking at relative valuations and economic conditions and questioning our own capital market assumptions. And we do react tactically to market conditions by rebalancing portfolios.

For example, as the equity market cumulatively doubled over the three years ending 2021, we worked with clients to trim equity positions to maintain the agreed-upon asset allocation. In the current bear market, we are taking the same approach, this time considering in consultation with clients if – and when – it’s appropriate to rebalance into equities.

We know it is unlikely that we or just about anyone else will make the correct decision to sell an asset class right before it goes down and to purchase it right before it goes up, so we proceed very carefully. Additionally, we must consider the tax consequences of sales for most of our clients.

Please review Jake’s article and let us know if you have any questions. It can make for uncomfortable reading, which is why not many wealth managers show what drawdowns can really do to a portfolio. We do. Most of our partners have already experienced three statistically “once-in-a-lifetime” financial events (in 2000, 2008, and 2020), so we know the value of planning and preparation.

Our goal is for every one of our clients to be well-positioned to ride out this and future bear markets, and to be able to look forward to the better days that will inevitably follow.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be reached at maurer@evercore.com.

Here’s a paradox: In the two years in which we have wrestled with a global pandemic and its myriad related issues, the S&P 500 soared, rising 120% from the initial shutdown shock. Now, just as the virus may be downshifting to endemic, the market and world is becoming more volatile.

There are reasons for this contradiction, of course, notably the recent spike in inflation and the prospect of rising interest rates, which are addressed in this issue of Independent Thinking – and now a major geopolitical shock in eastern Europe. But over the years, we have learned a thing or two about change. That’s why we work to construct flexible wealth plans and resilient portfolios intended to limit drawdowns and to produce reasonable, risk-adjusted returns, in all market conditions.

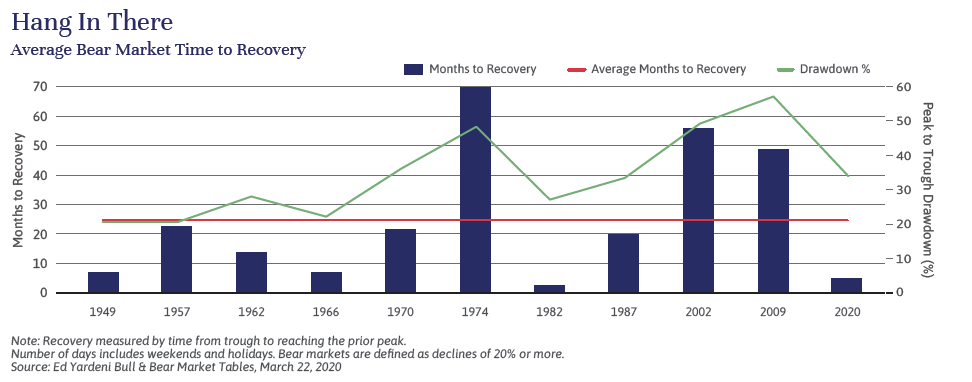

The first and most important step for investors is to acknowledge that these are challenging times and hang in there, come what may. Equity markets generally recover as the world returns to order, illustrated below.

Second, and specifically to investing, let’s deal with this change in the full context of our decade of remarkable gains. Thanks to a rare show of partisan resolve and an accommodating Federal Reserve, the U.S. economy barely missed a beat throughout the pandemic, and investors enjoyed spectacular stock market growth. Those of us who are retired or working remotely and sheltering in our own homes saw our balance sheets improve dramatically. We spent less and saved more, while our assets, including the homes in which we sheltered, soared in value.

As we look ahead and deal with this market correction, along with a period of inflation and rising interest rates, it is important to take the time to reexamine goals and appetites for risk and liquidity. As I talk with our clients, some common themes emerge. Here’s an example:

A couple, let’s call them the Smiths, had $20 million in liquid assets when they began working with us in our New York office in 2017, when the S&P 500 was less than 2,500. They were comfortable with some degree of risk but were willing to forfeit some prospect of return to protect their portfolio against substantial market drawdowns – an approach that kept them sanguine during the COVID-19 drawdown, illustrated below. In keeping with their risk tolerance, we continued to actively rebalance their portfolio, trimming equity gains as tax-effectively as possible, while adding to defensive and illiquid asset allocations. They have spent about 5% of their portfolio a year, but the market has more than made up for that, and they now have $25 million in investable assets even after the S&P 500 has fallen close to the 4,200 level in the current market drawdown.

As we recently sat down with the Smiths to review their accounts and our investment outlook, we came to the joint realization that they can now afford to explore more options, even taking into account the current volatility. The overall growth in their assets over the past five years has made them confident about their own future, able to withstand and exploit market fluctuations. They are now considering using a portion of their unified gift and estate tax credit and giving a portion of their still very appreciated securities to their children and grandchildren, letting the funds recover and grow for the next generation free of future estate tax. They can hedge their gifting through a Spousal Limited Access Trust, or SLAT, which would enable them to remove the assets from their taxable estate while allowing one spouse to have future access to the trust funds.

It’s important to note that the Smiths are able to consider taking on a little more illiquidity risk because they have over 25% of their portfolio in cash and defensive assets, enough to cover spending and capital calls for five years. Based on our capital market assumptions, we believe investing in illiquid growth opportunities can produce returns that exceed liquid growth equities by 3%-4% annually. The Smiths are also prepared to put some of their cash to work now, adding to quality shareholdings at more advantageous prices.

Of course, the right plan and the right investment portfolio will be as unique as the family it serves. The Smiths are considering taking on more risk. For others, sitting tight or taking less risk may be the appropriate solution at present. But I hope that all of us who are living through this extraordinary, paradoxical time will consider a thoughtful review now with trusted advisors.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

This is not “That ‘70s Show”. I know that not because I’m familiar with the popular television show of that name, but because I started my career in 1970. It was a decade of poor economic growth and poor equity performance, accompanied by runaway inflation of as much as 13 percent. Interest rates also rose over the decade as the Federal Reserve attempted to fight inflation; by September 30, 1981, 40 years ago, the Treasury 10-year note yielded 15.82%, a record high.

The focus of wealth managers then was to keep investors from losing too much ground while remaining positioned to benefit from future growth. So the recent, and we believe temporary, run-up in inflation to around 5% certainly bears watching, but it doesn’t keep me up at night.

This is not “That 2010s Show” either. That decade was marked by extraordinary returns in several asset classes, notably equities, which enabled balanced investors to stay on track to meet their financial goals, despite historically low dividend and fixed income yields. The S&P 500 index rose 14.5% on an annualized basis from the beginning of that decade to this year to date. (From fashion to social mores to investing, most decades seem to end a year or two into the next.) Our balanced account strategy compounded annually at 9.0% net of fees, outperforming its benchmark, which itself returned 7.7% over the same period.1

These returns have been just too easy to get used to. But at some point, the S&P 500 is likely to revert to its 10% annualized growth mean, illustrated by the chart below, and balanced accounts will move accordingly. In addition to rising inflation risk, income and capital gains taxes look set to rise. Domestic policies seem to swing in long arcs based on election cycles; the pandemic and related global supply chain issues only add to the uncertainty now. While we certainly hope to continue generating strong investment returns, we are under no illusions that it’s going to be easy.

From my vantage point, as Chairman, and as the Partner at our firm with the longest memory, this seems like a crucial time to review lifestyle, family, business and other goals in anticipation of a changing environment. That means revisiting lifestyle needs, circumstances and risk appetites. It’s our job to help our clients manage through personal change, as well as change in the markets. A close review of each client’s circumstances and perspectives will, along with our capital market assumptions, inform financial plans and direct investment recommendations.

For some, a close review may result in putting off retirement for a few years or viewing philanthropy differently. Others may elect to increase their portfolio’s return potential by investing in more illiquid assets, trading liquidity for potentially higher returns. Some will consider a change in domicile to a more tax-friendly state. Many should review estate plans in light of proposed estate and gift taxes, as Justin Miller observes in his article, Estate Tax Planning: Act Now, Before It’s Too Late. Investors who rely on their portfolios to fund all or part of their lifestyles and have been trimming equity positions to cover spending requirements, as well as to rebalance portfolios and reduce risk, may need to reduce their spending.

We may be at the beginning of an inflection point, so now is the time to make or review wealth plans. There’s no substitute for a conversation. Please make time to sit down, virtually or in person, with your Evercore team, to plan for this decade – and the years to come.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

I really like scaffolding as a metaphor for supporting our families. I like it so much that I’m borrowing it from Dr. Harold Koplewicz, President of the Child Mind Institute, author of The Scaffold Effect: Raising Resilient, Self-Reliant, and Secure Kids in an Age of Anxiety and our guest on a recent client webinar (see the recap here) – and extending it to wealth management.

Isn’t some measure of financial scaffolding exactly what many of us are trying to provide our children and, perhaps, grandchildren and future generations?

Think of a scaffold outside a building – easy enough if you live in New York or another big city. It typically enables the building to rise higher. In wealth management terms, this means providing just the right degree of financial support and structure to allow children to fulfill their potential. The best scaffolding will vary by family and for each family member, as each individual is unique and will develop – and will come to define happiness and success – in his or her own way. But truly supportive family financial scaffolds generally have three common elements. Let’s review them here.

First, sustainable financial scaffolding is built on a firm ground. In this sense, parents understand and are comfortable with their own financial future before extending support to others. This means thoroughly reviewing lifestyle goals and analyzing cash flow to account for aging, balancing family needs with philanthropic commitments, and other, less foreseeable changes. Once the foundation is set, the scaffolding can rise.

Second, the focus of the scaffolding tends to be on educating the next generation. That doesn’t just mean funding tuitions and learning experiences, although that is a big component in most family financial superstructures. It also means providing the scope, restraint and flexibility to educate children to understand how fortunate they are to have this support, and working to instill strong, lasting values that they can share with future generations.

Third, the scaffold construction should be flexible, able to adjust to changing family structures and circumstances. Trusts can be very effective scaffolding tools, if structured and administered appropriately.

That’s the theory. Here’s an example of how a strong scaffolding that included a thoughtfully drafted, well-administered trust can work in practice.

A couple who negotiated the successful sale of their transport company several years ago were able to fund trusts for their two children using their full estate and gift tax exemptions. At the couple’s deaths in 2020, the trusts were worth $40 million and the remaining $30 million left in the couple’s estate was left to a family foundation. The co-trustees, a relative and a corporate trustee, like all good trustees, had and continue to have important decisions to make. (See the Independent Thinking article, Choosing the Right Trustees here.)

One of the two young adults has special cognitive needs that means he’ll require lifetime support; the other has just earned a PhD in special education. Their parents, with the help of the trustees, have made the appropriate provisions in their wills to ensure care for the older child (while ensuring that he remains eligible for public benefits over his lifetime). The daughter will become a co-trustee of her brother’s assets if she is willing and when she is prepared. Ultimately, the assets will be redirected to the daughter and her future family.

Their cousins, the children of the professor and his librarian wife, are still in high school. But the parents are already preparing them to be good custodians of the wealth they stand to inherit. With the potential risks as well as opportunities in mind, they have included many of the provisions in their own wills that the grandparents did in the original trust, to protect and encourage the children in whatever their futures hold.

Well-crafted and properly administered trusts can serve as financial scaffolds for families, even for generations. They can provide help when it’s needed and encourage the beneficiaries to reach new heights.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

It’s been more than a year since I – and I’m guessing you – enjoyed a live performance. I’ve been hooked on the theater since 1961 when my parents took me to see Camelot, the Lerner and Loewe musical starring Richard Burton, Julie Andrews and Robert Goulet, at the Majestic in New York City. And I was so looking forward to seeing The Lehman Trilogy last spring along with some of our clients. But … well, you know this particular plot twist: Stages, along with concert halls and comedy clubs, went dark, with millions of performers, stagehands, ushers and back office personnel left bereft of livelihood and passion.

Their virtual efforts, however admirable and entertaining, don’t seem to me a satisfying substitute for the real thing (although a recent production of Meet Me in St. Louis by the Irish Repertory Theater of New York came close). I miss the intimacy of the venue, of being part of the audience as we are transported to a new place, swept up in the drama, the mystery, the music and the laughter. I miss rising together, with one voice, to thank the cast for sharing their talents with us.

That talent is still out there: More than five million Americans make their livelihood in the broader arts, at the National Endowment for the Arts’ last count, with more in New York alone than in finance, tech or education. They are waiting in the wings, working at other jobs, hoping for better days. I like to think that they miss us too.Arts and culture represent 4.5% of U.S. gross domestic product, or GDP, a proportion larger than that contributed by industries as diverse as construction, agriculture, and transportation. The $75 million appropriated back in March by Congress through the CARES Act to preserve jobs and help support organizations forced to close wasn’t nearly enough.

In the interim, we can help. One of the great privileges of a career in wealth management has been to work with clients who integrate the arts into their lives, sharing their enthusiasm with their families and, often, with their communities. Many of our clients are continuing to support the arts by keeping subscriptions and memberships current and by donating to favorite institutions.

We can help, whether your interests are in the arts or in the many other areas affected by the duration of this pandemic. It’s worth noting that this may be an opportune time to diversify appreciated stock positions in anticipation of higher income and capital gains taxes, if that makes sense in the context of broader retirement, family gifting and philanthropy goals. (See Pam Lundell’s article here.) It’s also a good time to consider strategies such as charitable split interest trusts.

It’s been 60 years since I first sat in that theater, enthralled by the trials of Arthur, Guinevere and Lancelot. I will be at least as thrilled to see the lights switch back on and to wait with the rest of the (inoculated) audience for the curtains to rise again.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

The vanguard of the Baby Boomers came of age at a challenging time in America; I turned 21 in 1968, a year in which none of us knew what would happen next. Now we’re coming into our old age during a pandemic in which we are among the most vulnerable and, again, none of us know what will happen next. But we can do this, with a good attitude and the right team in place.

First, we need to get through this pandemic. This winter will bring a return to indoor life for many and a sense of isolation, as outdoor restaurants, gyms and yoga studios shutter. Even those of us in sunny climes may be dreading the prospect of renewed lockdowns and holidays without friends and family present. It won’t be easy, but with intelligent social distancing, a lot of Zoom time and a dose of good luck, it will be manageable. I really like this line by Vivian Greene, the widow of Graham Greene and a fine author in her own right: “Life isn’t about waiting for the storm to pass…. It’s about learning how to dance in the rain.”

So let’s look the storm in the eye and plan. If current statistics serve as a guide, 70% of the 10,000 Americans turning 65 each day will need some form of long-term care and 20% will fall prey to some kind of financial abuse. By the age of 80, 70% will experience some form of cognitive decline. Clearly, this is not a process we want to embark on without support. But again, with that support in place, aging can be a joy. It’s interesting to note that survey after survey suggests a U-shaped life experience of happiness, with older people for a good while as happy as those in their 20s.

I started assembling my personal aging support teams in my 50s, first for my parents (see Jen Tse’s article here on adult children planning for aging parents), but around the same time for me and my wife. I had seen too much over my career to leave any manageable aspect of aging to chance, whether for my family or, when we founded Evercore Wealth Management in 2008, for our clients. We need to be ready, whether for the proverbial bus or for a long, slow decline.

A good wealth management firm will be prepared to take the lead in coordinating a plan and, when the call comes, in its execution. The dedicated advisors will know the members of the team, and will know the location of the essential documents (including healthcare proxies), the location of all assets and insurance policies. We recommend the use of a revocable trust as the primary tool, which allows a successor trustee to step in for the grantor at the time of the grantor’s cognitive decline, and ensures that the wishes of the grantor are carried out and the family’s interests are protected.

In addition to the wealth advisor, the right team will include a physician, an estate attorney, an accountant, and one or more family members or a trusted friend. The team should also include a care manager, who can help families navigate healthcare and residential options, from aging in place at home, to memory loss and skilled nursing facilities. Each member of the team should have a clear role, and be fully briefed on the relevant individual and family goals.

It is important to keep the team informed as to changes in circumstances and goals. It’s a good idea to revisit the membership of the team on a periodic basis to check on each member’s level of engagement. For example, I know I will have to replace the physician on my team over the next few years as he retires from his practice. I also recommend that trusts include a provision to remove corporate or individual trustees to allow the family flexibility with unanticipated circumstances. The team and documents we leave behind will oftentimes be the proxy for our voice and will help shape how we are remembered by our children and grandchildren.

A long life is a great blessing, if it can be lived well. That may feel especially challenging this winter, but hang in there. With the right planning and the right team in place, chances are that we’ll keep dancing in the rain.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

Fifty years ago, I was attending business school and marching up and down Wall Street – but not the way you might think, at least not at first. Back then, I was marching as an organizer of a group called Business Students for Peace. It was just a few weeks after the Ohio National Guard fired on protesters at Kent State University, a time that felt much like this. A few weeks later I was marching the street again, seeking employment. I stumbled into a position at U.S. Trust, then located at 45 Wall Street, and entered the wealth management business.

I’ve learned at least two things since. The first is to hold on to our ideals, as they will be repeatedly tested in our personal and business lives. I like to think I’ve done my best, but I know that there is much more that I (and all of us, as a society) can do, a subject I hope to revisit in subsequent editions of Independent Thinking. The second is to be prepared for change, because none of us know what’s coming next.

Enter COVID-19. I haven’t been to a restaurant, bumped into a friend or colleague or, worse still, hugged a grandchild without a mask since mid-March. And like many among my generational cohort, I’m sad to say that I have no plans to rush back to the old normal. But if I didn’t expect a pandemic, I was at least prepared, thanks to good technology and good advice.

I love technology. I find it incredibly interesting, and it informs my work and other passions. So when I realized my home offices in Florida and New York would in fact be my only offices – and video my only way of catching up with those grandchildren – I was already set up with the appropriate equipment (as were my colleagues, thanks to years of robust business continuity planning). And I was equipped to play, as well as to work. My spouse of 47 years and I had subscriptions to multiple entertainment sources – daily online newspapers, magazines, music and films, as well as video technologies that enabled us to socialize, order online, and settle $5 wagers on golf games through Zelle.

On a related note, our financial accounts were online, our documents stored on the cloud (as are our photographs), and we were enrolled in contactless payment systems.

It is my hope that all Evercore Wealth Management clients, irrespective of age or technological sophistication, will similarly benefit from technology. Please see Ashley Ferriello’s article on virtual wealth planning here and, if you were unable to join our recent webinar Thriving in a Digital Age: A Primer (and More), you can access the replay on our client site or here.

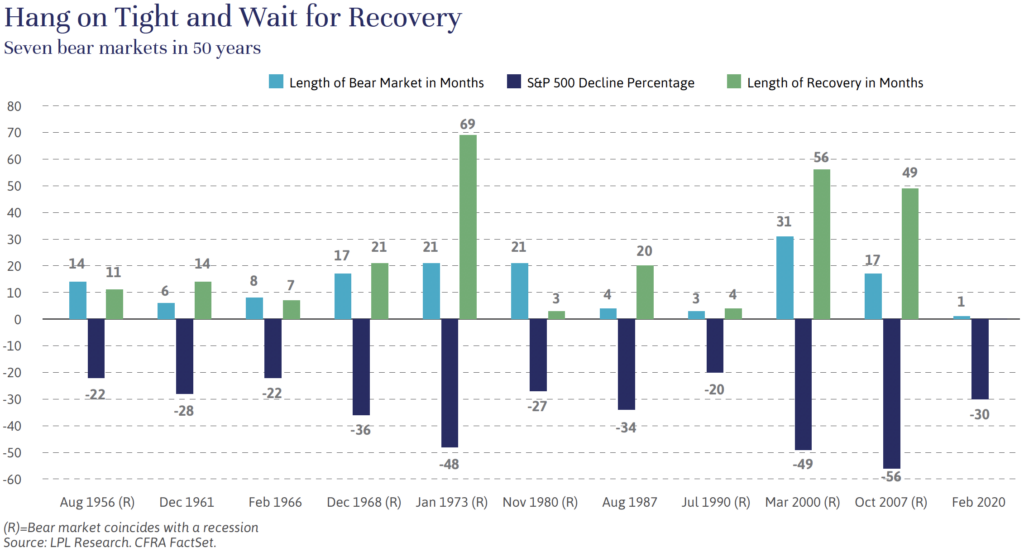

Additionally, I (along with other Evercore Wealth Management clients) was ready on the financial front. In the 50 years since those marches on Wall Street, I’ve experienced seven bear markets, all very different but none pleasant. The important thing is to ride them out, which means staying close to trusted advisors who have their clients’ best interest at heart and are objectively focused on those clients’ long-term goals.

As illustrated below, each of those bear markets had a maximum drawdown of between 20% and 56%, and lasted between three and 31 months, with recovery times longer still. The COVID-19 bear market, which started in February and resulted in a 30% drawdown, appears to have lasted less than one month, although we won’t be sure of that for some time. But we’ll be prepared, in any case.

None of us know what’s coming next. I’m sure that all of us hope for an increasingly equitable society, an effective COVID-19 vaccine, and to gather in peace in a new and better normal.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

This pandemic is testing the resilience of our society, our organizations, and our portfolios. There’s a long road ahead, but it seems to me that we are coping and will prevail. I see great resilience all around me, from our first responders, to our scientists, to the people who are stocking – and restocking – supermarket shelves. As for the rest of us, we are doing our part in doing what we are told, carrying on while remaining socially isolated, to help flatten the curve and to allow economic activity to restart.

Our firm is certainly resilient, up and running remotely at full steam as soon as we vacated our office buildings across the country. I could not be more proud of our teams and the ways in which we are staying close to each other and to our clients.

Of course, it’s easier to be resilient if you are prepared. Our partners and I, all of whom have experienced past significant market upheavals, built this firm to meet clients’ long-term goals. That means constructing and managing portfolios to anticipate and limit the impact of big drawdowns and to produce reasonable, risk-adjusted returns through all market conditions.

Our drawdown analysis is based on 50 years of data and has, in my opinion, always been one of our most important tools and a focus of discussions with potential and existing clients. Not many firms show the potential impact on portfolios of a big drawdown. We always have, which has helped our clients prepare for the real thing.

When we entered 2020, we projected that our model balanced portfolio had a drawdown potential of 24% – meaning that it could fall 24% from its peak value to its trough value and remain positioned to participate in the subsequent economic recovery.

Our balanced portfolios include growth investments and defensive investments. In times of market disruption, we generally anticipate that growth securities can lose as much as half their value (to date, the S&P 500 has been down 34% and is now down 18.5%) while defensive securities, mainly investment grade bonds, as the name of the asset class suggests, will generally hold their value. Our clients who felt they could not tolerate a drawdown of 24% have more defensive assets in their portfolio, and those who felt they could tolerate more risk have more growth assets in their portfolios.

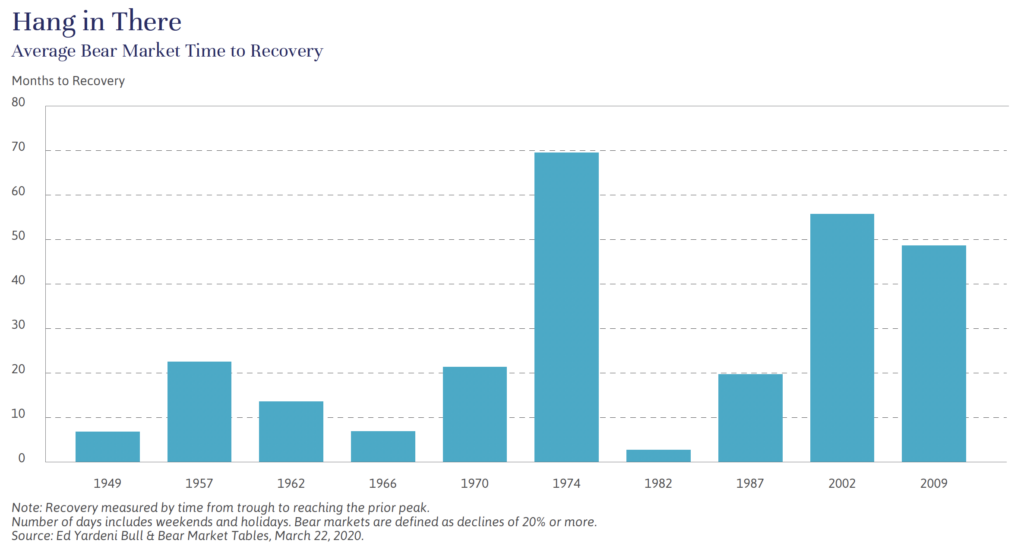

We were surprised by the recent lack of liquidity in high-grade bonds, but take comfort that liquidity is returning to those high-grade markets in anticipation of fiscal and monetary stimulus. In past market drawdowns, the time for the growth assets to return to previous peak values has varied from three months to 70 months with an average of 27 months, as illustrated below.

This has certainly been no ordinary market drawdown, as John Apruzzese and others discuss in these pages. Nevertheless, we believe our balanced portfolios will continue to prove resilient and that our clients, with the help of our advisors, will maintain sufficient liquidity and be in a position to benefit from the recovery.

One of the paradoxes of this period of social isolation is the renewed appreciation of the people in our lives. As I write this, my wife and I remain holed up at home in Florida, missing family, friends and colleagues but grateful to be in constant touch. I enjoyed seeing so many familiar names engaging in our recent investment outlook webinar; seeing the questions scroll through made me feel as close to our clients as if I were in the same room.

I know I speak for all my colleagues when I say that I am very grateful for our wonderful clients.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

Investment and Wealth Management services are provided by Evercore Wealth Management, LLC an investment advisor registered with the U.S. Securities and Exchange Commission (the "SEC") under the Investment Advisers Act of 1940. Registration with the SEC does not imply a certain level of skill or training. Trust and custody services are provided by Evercore Trust Company, N.A. a national trust bank regulated by the Office of the Comptroller of the Currency.

Client retention rate is based on data from 06/30/24 – 06/30/25. Assets under management are as of 06/30/25