close

Jeff is the Chairman of Evercore Wealth Management and Evercore Trust Company, N.A. Jeff, Chris Zander and their partners established Evercore Wealth Management in 2008. The firm is now one of the leading independent Registered Investment Advisory firms in the United States (Barron’s, Financial Advisor 1 ).

Jeff was earlier Chairman and CEO of U.S. Trust, where he started his career in 1970 and served as President and Chief Operating Officer before he was appointed CEO in 2001 and Chairman of the Board in March 2002. In 2003, he joined Lehman Brothers as Chairman and Chief Executive Officer of Lehman Brothers Trust Company and remained with the firm through 2007.

Jeff is the author of the book, Rich in America: Secrets to Creating and Preserving Wealth. Prominent in industry activities, he is a former Chairman of the American Bankers Association’s Trust and Investment Management Division. He is also actively involved in a number of community organizations in Florida and New York. He serves on the boards of several charitable organizations and acts as Chairman of the Board of the Hebrew Home at Riverdale in New York.

Jeff holds a B.A. from Alfred University, an M.B.A. from New York University, and a J.D. from St. John’s University School of Law.

As a late-in-life Pilates enthusiast, I’ve learned the importance of alignment; all it takes is one body part to fall out of whack, and all the other bones, joints and muscles soon feel the strain. Adjust that part while there’s still time, and the whole can come together again.

The same is true for managing wealth – especially in, or ahead of, retirement. We need to make the right corrections, aligning our short-term spending (on ourselves and others) with our long-term lifestyle needs and our legacy goals. The choices are very personal and entirely up to us, but we do need to understand the interconnectivity.

Want to buy a boat? Join a new club? Spend a year traveling the globe in style? Terrific – that sounds like a lot of fun. Family temptations may loom large too, as helping to fund homes or start-up businesses for children, and educations and other enriching experiences for grandchildren, can feel very satisfying. And more time to engage with nonprofits is likely to inspire more generous gifts.

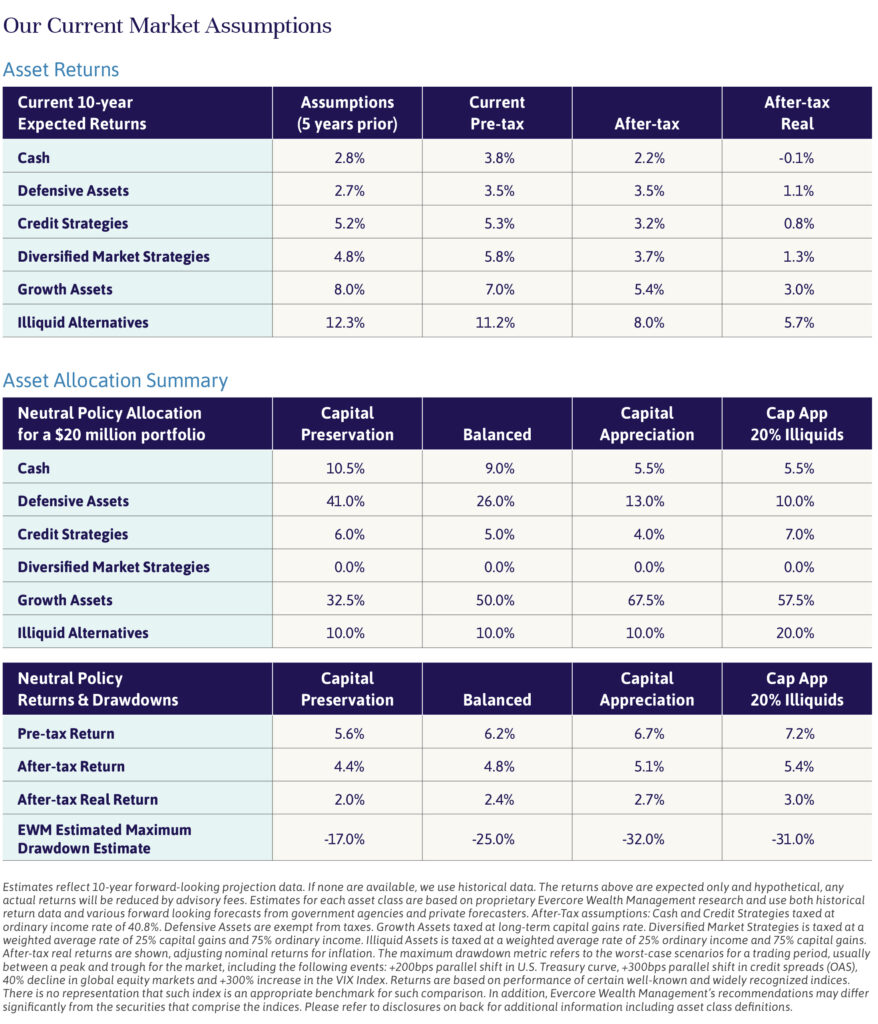

These are all wonderful ways to spend, of course. But they will be more enjoyable for those comfortable with the tradeoffs. And there are usually tradeoffs, no matter how large the portfolio. Take a look at the chart below. Here’s what seemingly small differences in spending rates can do to the same $20 million portfolio.

Most advisors plan based on a proportion of pre-retirement income, typically 70%, or current reported spending, assuming that it will drop off in retirement. And just about all base their estimates on average life expectancy and inflation rates.

But I am certain that for many of our clients, spending does not drop off in retirement. Sure, we save a few bucks on commuting, and we don’t need any more suits (who does, nowadays?). But that’s a drop in the proverbial bucket for the high net worth and ultra-high net worth families. In my experience, most of us tend to underestimate our spending, both before and into retirement. The exceptions become the rule; the once-in-a-lifetime experience is quickly followed by another (or shared with family). In short, there is always going to be another one-off expenditure.

Not only are we having more fun than our own parents or grandparents did, but we are also living significantly longer. Indeed, the top 1% of Americans by wealth at age 65 can now reasonably expect to live well for another 20 or so years, thanks to the miracles of modern medicine. And there will still come a time when our lifestyle spending shifts to medical and care-related expenses.

As for inflation, it’s easy to underestimate that as well, particularly as prices for goods and services valued by the high net worth consumers appear to be rising relatively fast. (Please see my related article here).

So, how do we find financial balance in our so-called golden years? The starting point is a thorough lifestyle analysis, to evaluate current and future spending needs, mindful of the need to fund potentially very long lives. These calculations should take into consideration capital market return assumptions, as well as estimated inflation and tax rates, and individual tolerance for market and liquidity risk. (For our current capital market return assumptions, see chart below.)

We can then evaluate the likelihood of reaching other goals, including wealth transfers (a pressing topic for clients who have yet to take advantage of at least part of the $27.2 gift tax exemption before it sunsets next year). And if the numbers aren’t aligned to those goals – or if the goals themselves have changed – we can recalibrate the wealth plan. Trim (or occasionally, increase) spending, take on more investment risk, revisit legacy goals – one or a combination of these and other tactics can support a long and happy retirement.

As I’ve discovered in Pilates, it is best to address weaknesses earlier. But it’s never too late to make improvements.

Jeff Maurer is the Chairman of Evercore Wealth Management and Evercore Trust Company. He can be contacted at maurer@evercore.com.

This milestone 50th issue of Independent Thinking® explores key themes shaping global finance, including the economic impact of AI, the resilience of markets amid geopolitical crises, and the growing role of private equity continuation funds.

The publication emphasizes that despite global turmoil, the U.S. economy and markets continue to benefit from robust technological innovation and disciplined long-term investing. It presents timely planning guidance for life events like divorce and retirement, especially as wealth planning becomes more complex in the face of rising longevity, international family dynamics, and the Corporate Transparency Act. Interviews with industry leaders offer insight into evolving investment opportunities, including GP-led secondaries and single-asset continuation vehicles.

Life insurance is also explored as a strategic tool for liquidity, estate equalization, and tax efficiency for high-net-worth families.

Investment and Wealth Management services are provided by Evercore Wealth Management, LLC an investment advisor registered with the U.S. Securities and Exchange Commission (the "SEC") under the Investment Advisers Act of 1940. Registration with the SEC does not imply a certain level of skill or training. Trust and custody services are provided by Evercore Trust Company, N.A. a national trust bank regulated by the Office of the Comptroller of the Currency.

Client retention rate is based on data from 06/30/24 – 06/30/25. Assets under management are as of 06/30/25