close

Volatile markets trigger anxiety and strong psychological reactions, making it a challenge to stay focused on wealth-planning fundamentals. The good news is that a market downturn can provide unique opportunities to strengthen a long-term strategic wealth plan. Here are some suggestions to stay on track, reduce risk and even take advantage of down markets in a volatile economic climate.

Certain foundational steps can help protect a wealth management portfolio in uncertain times.

Maintain Adequate Liquidity. Ensuring access to sufficient defensive assets – such as cash and Treasuries – for lifestyle needs and short-term obligations is the starting point. At current levels, markets could slide further, and having access to adequate liquidity reduces pressure to sell investments at depressed prices and trigger capital gains. Depending on the sources of income, it could be prudent to maintain adequate short-term reserves to cover at least one year of expenses. Setting up a secured line of credit could provide additional protection if necessary.

Recalibrate Asset Allocation. In addition to ensuring adequate defensive assets, a down market is an opportune time to reassess the overall investment mix in the context of individual and family risk tolerances, time horizons and financial objectives. Minor asset allocation adjustments can often help realign the investment strategy with long-term wealth-planning goals.

Tax-Loss Harvesting. If the portfolio includes positions with losses, consider harvesting them. Those tax losses can offset any current or future capital gains. From an asset allocation perspective, investors can reinvest in a similar index fund or exchange traded fund (ETF), to maintain a similar market exposure while avoiding the tax code’s wash-sale rule. This disallows losses when selling an investment if a “substantially identical investment” is purchased 30 days before or after the sale. To the extent that investors are working with multiple investment management firms, the lead advisor should coordinate the overall investment strategy so that one manager isn’t buying the same stock that another manager sold, which would disallow the loss under the wash-sale rule.

Adjust Timing for Charitable Giving. It may be prudent to wait until market values recover before making charitable gifts to a public charity, donor-advised fund or private foundation. Donating appreciated assets down the road can increase the impact of generosity while also allowing for a larger itemized deduction for the fair market value of the donation, free of any capital gains tax on the long-term appreciation.

Review Loans. With interest rates fluctuating, it’s worth reviewing current mortgages and other loans. Extending a fixed-rate period or locking in lower payments may improve financial flexibility.

While market downturns can be unsettling, they also open the door for long-term planning strategies.

Thoughtful Cash Investments. A drop in market values could be a compelling time to invest surplus cash. Investment entry points during market lows can pave the way for more significant long-term growth, especially as part of a rebalancing strategy aligned with long-term goals.

Roth IRA Conversion. Market dips provide a tax-efficient window to reduce the tax cost of converting traditional IRAs to Roth IRAs. You can pay tax on a lower asset value now and enjoy more potential tax-free growth moving forward. Investors can withdraw assets from a Roth IRA after age 59½, completely free of income taxes. Heirs can later withdraw remaining Roth IRA assets without any income taxes. Time horizon is key in evaluating this strategy.

Maximize the Lifetime Gift and Estate Tax Exemption. The current $13.99 million per person ($27.98 million per married couple) exemption presents a powerful opportunity for gift, estate and generation-skipping transfer, or GST, tax planning. Transferring assets when values are depressed locks in potential recovery and appreciation outside the taxable estate. Using trust strategies – such as spousal lifetime access trusts, or SLATs, grantor retained annuity trusts, or GRATs, sales to intentionally defective grantor trusts, or IDGTs, and/or Delaware dynasty trusts – can not only provide additional asset protection for loved ones, but all the potential market recovery and future growth of the assets can be transferred completely free of gift, estate and GST taxes to future generations.

Fix Underperforming GRATs. If a prior GRAT has underperformed, consider swapping in cash, bonds or promissory notes for the assets that have gone down in value, then re-GRAT those depressed assets to reset growth potential as part of a new GRAT strategy with a higher likelihood for success. In a way, the re-GRAT strategy is like “heads, you win; tails, you don’t lose.”

Updating a lifestyle and retirement financial planning analysis can help mitigate feelings of panic and prevent imprudent overreactions to a market downturn. Testing the plan against various market scenarios – including through our calculations around potential maximum drawdowns and periods of higher inflation – can help investors better assess the probability of financial success and identify any necessary changes. Examples of potential wealth-planning adjustments could include modifying spending levels, adjusting asset allocation, factoring in alternate income sources like employment, dividends, interest or trust distributions, and reassessing required minimum distributions.

While it’s natural to feel uneasy during market downturns, it is important to stay engaged. The right strategies can help investors weather today’s volatility while laying the groundwork for long-term success.

In an economically challenging environment with increased market volatility, staying in close contact with your wealth management advisor is more important than ever. If you’d like to revisit your wealth plan, discuss any of the strategies mentioned above, or simply talk through what’s on your mind, our Evercore Wealth Management team is here for you. Please don’t hesitate to reach out.

Justin Miller is a Partner and the National Director of Wealth Planning at Evercore Wealth Management and Evercore Trust Company. He can be reached at justin.miller@evercore.com.

Private fund principals have access to unique planning strategies that leverage both carried and capital interests to shelter assets from transfer taxes, and reduce and defer income taxes. Now is the time to take advantage of these strategies.

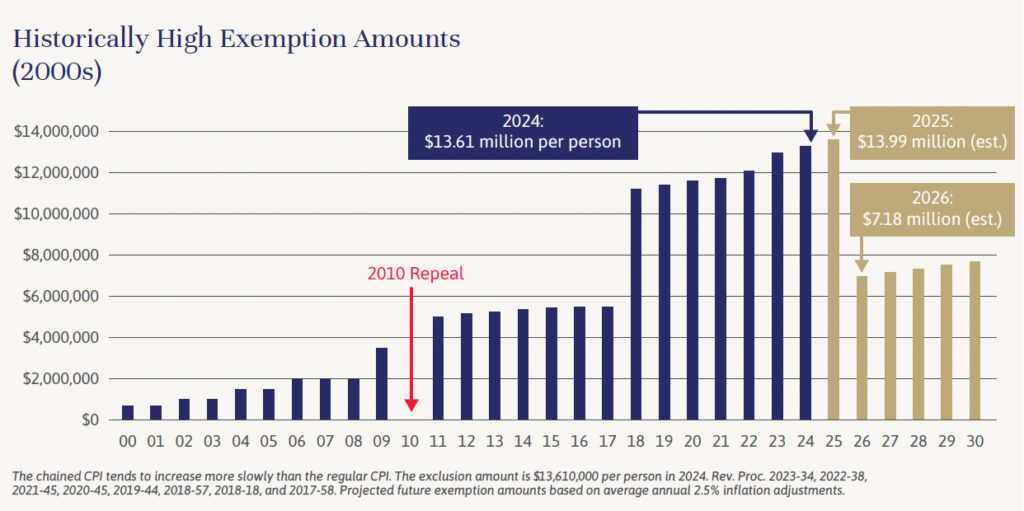

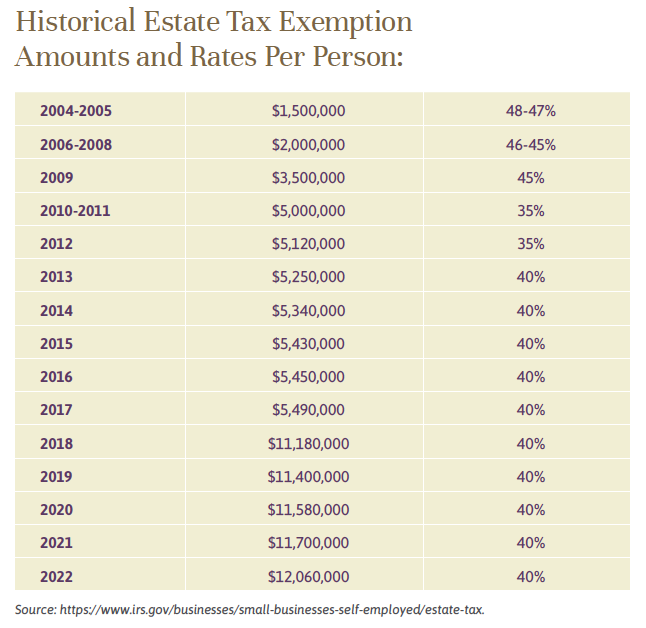

As described here, the lifetime individual federal gift, estate and GST tax exemptions are currently projected to drop to an estimated $7.16 million as of January 1, 2026, from the current $13.61 million per individual. Until then, a married couple that gifts $27.22 million to a trust for the benefit of children and grandchildren before the sunset could potentially avoid over $5 million of estate tax at the current 40% rate, and also possibly save heirs future gift, estate and GST tax on any growth of those assets with proper planning. Even if the exemptions are not reduced, gifting assets lowers estate taxes by 40 cents for every dollar of growth in the initial gift and could avoid additional state estate tax and GST tax.

So, what should private equity, private credit, and venture capital fund principals do? The following planning strategies could be considered:

The ideal asset to gift is one with a low value at the time of transfer with large upside potential. If you give $10 million into a trust that grows to $50 million at the time of your death, you have effectively moved $40 million of growth out of your taxable estate, saving heirs roughly $16 million in transfer taxes. Carried interest in a newly formed fund is the ideal asset to gift, as it arguably has a relatively smaller value at the initial closing but may have significant value in the coming years. Therefore, the carry can be gifted at a very low “cost” with potentially very high long-term value.

The problem with gifting carried interest is that the IRS, under Code Section 2701, does not allow a transfer of one interest in an asset while retaining another interest in the same asset. Fund managers often hold General Partner, Limited Partner and carried interests in their funds. If a manager tried to gift just the carry, the IRS would deem carried and all capital interests in the fund as a gift, which would be problematic and/or administratively impossible. Fortunately, there are two potential solutions to this problem.

The first is an exception to Section 2701 called a vertical slice. A fund manager can take a proportionate share of all their capital and carried interests in a fund and gift that “slice” to a grantor trust for the benefit of children and future generations. The vertical slice strategy is not as powerful as gifting only the carry, but it can transfer meaningful capital at its lowest valuation and potentially shelter future growth from estate taxation. However, there are certain considerations that must be kept in mind. The interests that are transferred will be subject to a proportionate share of capital contribution obligations. The trust that receives the interest should have enough liquidity to cover these capital calls. The manager’s advisors will need to be aware of any vesting requirements of the carried interest – unvested interests cannot be gifted. They will also need to know about any management fee offsets or other compensation arrangements.

The other strategy that fund principals can use is a sale of a derivative contract tied to the performance of a carried interest. A contract can be sold to an irrevocable trust that gives the trust some or all of the economic benefit of the carried interest above a hurdle over a period of time. This contract can be reasonably valued by a professional appraiser. Since the manager is not actually giving away the interest, only the economic benefit, a forced gift of the capital interest under Section 2701 is avoided. A derivative strategy could offer several advantages: It is administratively less burdensome; there are no capital call or vesting issues; and the most impactful asset from a tax savings perspective is gifted at a lower exemption cost than a vertical slice. However, given the complexity involved, this strategy may carry more audit risk. Principals also will need to beware of potential losses if the carry does not grow beyond the hurdle rate, death occurs before the contract expires (the contract will need to settle at that date), or a potential liquidity crunch if the contract term ends with a high carry value without any distributions.

Note that fund principals also may want to consider a Family Limited Partnership or Family LLC to pool other assets under one umbrella together with either one of the foregoing strategies. This can allow for easier administration and potentially further discounts to the valuation of the assets held in the partnership.

Successful mature funds generally have high valuations with relatively predictable cash flows. Fund managers who regularly donate to charity could consider transferring a portion of their mature funds to a Charitable Remainder Trust, or CRT, to reduce and defer income taxes. A CRT pays the fund manager a fixed annuity payment or percentage of the fund’s value every year. At the end of the trust’s term, any remaining value is transferred to a charitable beneficiary, which could include a donor-advised fund or private foundation. A CRT is a tax-exempt entity; therefore, when assets are transferred into the trust, the transferor receives an income tax deduction based on the estimated present value of the remainder, and the trust does not pay tax on any income generated by the fund. Instead, the fund manager will only pay a portion of the income taxes due upon receipt of the annual payments, making this an income tax deferral strategy.

Depending on the fund manager’s goals, a Charitable Lead Trust, or CLT, also could be an option. A CLT is similar to a CRT, except that the charity receives the annual payment, and the remainder can be transferred to heirs. A CLT can be set up as a grantor trust or a non-grantor trust. With a grantor trust, the fund manager receives an upfront charitable deduction but is subject to tax on the trust’s income each year. With a non-grantor trust, there is no upfront charitable deduction, but the trust receives a charitable deduction each year and the fund manager is not subject to tax on the trust’s income. Unlike a CRT, which is commonly used as an income tax planning strategy that also benefits charity after death, a CLT typically is utilized as more of an estate tax planning strategy that also benefits charity during life.

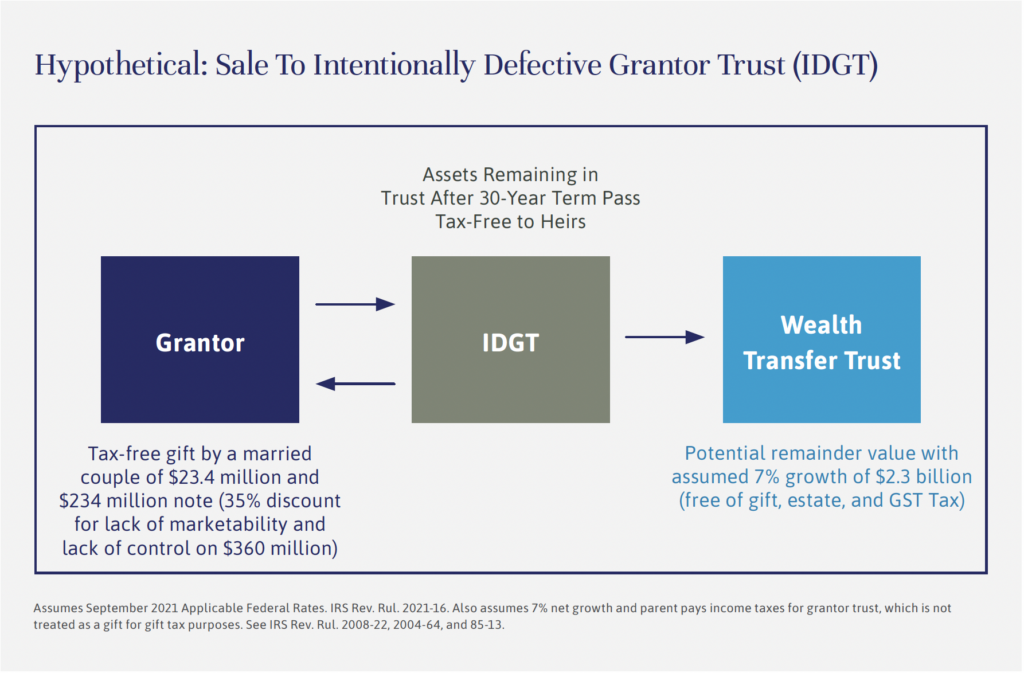

Fund managers who have already used their exemptions or who want to transfer only growth in their funds can use “freeze” strategies. The two most common are grantor retained annuity trusts, or GRATs, and sales to intentionally defective grantor trusts, or IDGTs. To summarize simply, GRATs transfer growth above the Section 7520 rate (4.4% as of October 2024) out of the estate while using almost no federal gift and estate tax exemption. One of the downsides of a GRAT, however, is that the GST exemption amount cannot be used effectively, making it less efficient for multigenerational asset transfers. Another option with potential for GST tax savings for transfers to trusts earmarked for grandchildren and beyond is a sale to an IDGT. (See a recent related article.) In this case, cash is gifted into a trust – typically 10% of the asset purchase amount – and the fund manager sells assets to the trust in exchange for a promissory note. Because the IDGT is a grantor trust, the sale to the trust is not treated as a taxable event for income tax purposes, but the asset can be removed from the grantor’s estate for gift, estate and GST tax purposes. The IDGT uses the cash and income received from the asset to pay annual interest on the note – often at the lowest applicable federal rate as published by the IRS. At the end of the promissory note’s term, the IDGT eventually repays the note while retaining all the growth in the asset minus the interest and principal paid back to the fund manager.

When deciding what strategies to use, private fund principals will need a team of advisors to help navigate the options in the context of long-term goals and giving viability. Proper execution and ongoing administration also are essential. Since this type of planning is highly technical, it should only be implemented with a team of advisors that includes attorneys, accountants, appraisers, and wealth managers who specialize in this area.

Sean Brady is a Managing Director and Wealth & Fiduciary Advisor at Evercore Wealth Management and Evercore Trust Company. He can be contacted at sean.brady@evercore.com.

Sunset is when the sun appears to sink below the horizon. However, when it comes to estate planning, sunset is when the current gift, estate and generation-skipping transfer, or GST, tax exemption under the Tax Cuts and Jobs Act of 2017 gets cut approximately in half. After 2025, individuals will be limited to giving an estimated $7.18 million tax-free to their heirs, down from the current $13.61 million “use-it-or-lose-it” exemption amount. A historic window of opportunity to maximize intergenerational wealth transfer is set to close soon.

Depending on elections in November 2024, it is possible that Congress – with the future president’s approval – could extend the historically high exemption amount by passing legislation similar to the Tax Cuts and Jobs Act of 2017. However, such an extension seems unlikely at this point, given the extent to which it would increase deficits. The Congressional Budget Office recently estimated that the cost of extending just the exemption levels through 2033 would be approximately $167 billion.

If 2026 still seems a way off, consider that some trust and estate attorneys are already turning away clients as the deadline looms. Anyone able to take advantage of the full exemption who fails to use more than $7.18 million will likely lose the remainder as of 2026, as illustrated in the chart below. Also lost after 2025 will be all the potential estate-tax-free appreciation of those assets, perhaps for generations to come. If that $13.61 million generated, say, a net 7% return over 30 years, that’s more than $40 million of savings at the current 40% gift and estate tax rate. For an ultra-high net worth couple able to gift twice that amount, the savings would be more than $80 million.

In short, this is the time to address three key questions: Can you afford to gift? If so, how much? And what should you give?

Preserving peace of mind is the starting point. Individuals and couples need to know that they will retain sufficient assets to sustain their lifestyle and meet other goals – a decision that should be made only after a thorough financial analysis. And even if parents or grandparents are ready to give, family members might not be ready to receive. Next-generation readiness and, often, complex family dynamics must be considered too. For those whose financial analysis shows that they should not gift more than the $7.18 million threshold ahead of the sunset, it is still prudent to begin estate planning sooner rather than later to maximize potential future growth outside of the estate and reduce the potential future estate tax exposure.

Trusts can play a key role here, helping to ease this transition and in planning for the unknown, including future generations. Spousal lifetime access trusts, or SLATs, Dynasty Trusts, and Intentionally Defective Grantor Trusts, or IDGTs, can preserve and protect wealth (see below for a brief guide to these three trust structures). Structuring any trust as a grantor trust amplifies the power of estate planning, as the grantor continues to pay the income taxes on the trust. This allows trust assets to compound over time unencumbered by taxes while the grantor reduces the amount of their estate that could be subject to future estate taxes without using up any additional exemption amount.

Keep in mind that the choice of an individual and/or corporate trustee is critical. Both an individual trustee and corporate trustee should know the family well and be confident that they can carry out their duties for a long time. Moreover, an individual and corporate trustee can be named together as co-trustees where the corporate trustee can educate and otherwise support the individual trustee by lessening the administrative burden, as well as assisting with future trust management and governance issues. (For more information, please visit https://evercorewealthandtrust.com/choosing-the-right-trustees/).

The next consideration is generally which assets to give and how to structure those gifts. Cash, real estate, public securities and private investments each have associated implications that need to be considered, as illustrated below. Each situation is different, so it’s important to run different test scenarios taking into account factors such as basis, capital appreciation and liquidity – to evaluate the pros and cons of gifting each type of asset.

Cash is straightforward, as there are no concerns around valuation or embedded gains. However, most people have a limited amount of cash on hand, and what they do have is reserved for lifestyle needs. The next option would be publicly traded securities, which, while also relatively easy to gift, require the consideration of additional planning issues, such as embedded capital gains. It’s important to know that assets gifted during lifetime will retain their tax basis and will not receive a step-up in tax basis at death. In other words, many assets – other than certain exceptions like retirement accounts – will have all the capital gains disappear if still owned at death, which does not apply to assets given away during life.

Private investments, such as private equity funds, can also be a great option for gifting; although gifting such assets can often involve greater complexity. These assets typically have significantly lower valuations early on but can later grow substantially for the benefit of heirs. (See the article by Sean Brady on planning strategies for private fund principals.) Similar to private equity investments, closely held business interests and real property can also be powerful estate planning tools, especially taking into account potential lack of marketability and lack of control discounts for gift purposes.

There is no one optimal strategy for gifting that works for everyone. It’s vital to customize any gifting plan and weigh the trade-offs in gifting different types of assets by working with a collaborative team of advisors, including your wealth manager, attorney, accountant, and potentially other specialists. Gifting these amounts is a big decision, one that should only be made in the context of a comprehensive estate plan. But if gifting is a goal, there may be limited time to do it in the most tax-efficient manner.

Justin Miller is a Partner at Evercore Wealth Management and Evercore Trust Company and the National Director of Wealth Planning. He can be contacted at justin.miller@evercore.com. Neza Gallitano is a Managing Director and Wealth & Fiduciary Advisor; and Alex Pavelock is a Director and Wealth & Fiduciary Advisor. They can be contacted at, respectively, neza.gallitano@evercore.com and alex.pavelock@evercore.com.

To view Justin, Neza and Alex discussing this topic in a recent webinar or to learn more, please visit https://evercorewealthandtrust.com/independent-thinking-panel-gifting-before-the-estate-tax-exemption-sunset-the-whys-why-nots-and-when/ or contact your Evercore Wealth Management and Evercore Trust Company Advisor.

Editor’s note: This guide is extracted from an article published in Independent Thinking in 2021; the amounts have been adjusted to reflect subsequent inflation.

One of the most popular wealth transfer strategies is to create a Dynasty Trust in Delaware or in other states with strong asset protection laws, for children, grandchildren and future generations.

A Dynasty Trust could not only prevent future gift, estate and GST tax, but it could also help protect assets for family members from future creditors in the wake of any number of potential events, such as a car accident or divorce. For instance, a married couple could transfer $27.22 million tax-free into a Dynasty Trust. Those assets and all the future growth would be permanently set aside for family members without being subject to gift, estate or GST tax. Moreover, many asset protection trust states like Delaware have eliminated the common-law rule against perpetuities, which means the Dynasty Trust can support multiple generations of a family for hundreds of years.

Dynasty Trusts are often set up as grantor trusts, allowing the grantor to pay all the income tax for the trust without any gift tax consequences. In other words, the Dynasty Trust’s assets grow free of income tax, and the payment of income tax by the grantor further reduces the grantor’s taxable estate. On the other hand, wealthy families in high income-tax states may want to consider creating a non-grantor trust, where the trust pays its own tax, in a jurisdiction where the Dynasty Trust would not be subject to any state income tax. As a non-grantor trust in a state without a state income tax, the Dynasty Trust could continue to grow free of estate, gift and GST tax, as well as state income tax for generations – subject to potential state sourcing rules and throwback tax, for example, in California and New York.

Not all wealthy parents are comfortable permanently setting aside millions of dollars for children and future generations, especially if they might need or want the assets back in the future. In that case, a spousal lifetime access trust, or SLAT, could be the optimal solution to maximize the gift, estate and GST tax savings while still protecting assets for the spouses for the rest of their lifetimes. With a SLAT, one spouse would create a $13.61 million irrevocable trust with their separate property to benefit the second spouse. After the second spouse dies, the SLAT protects future generations, free of gift, estate and GST tax. It is important to remember that SLATs are irrevocable trusts, which could be a big issue if spouses get divorced in the future.

It may also be possible for the second spouse to create a similar $13.61 million SLAT for the first spouse. However, the two SLATs would need to be independent and different enough to avoid what is known as the “reciprocal trust doctrine” and “step transaction doctrine.” Accordingly, the first spouse is taking a real risk that the second spouse might not necessarily fund a second SLAT for the first spouse. Suppose there is concern about the reciprocal trust or step transaction doctrine. In that case, instead of the second spouse creating a similar SLAT for the first spouse, another option could be for the second spouse to utilize their individual $13.61 million exemption by creating an entirely different type of trust, such as a Dynasty Trust, for future generations.

Typically, SLATs are grantor trusts, similar to Dynasty Trusts. As an alternative, careful drafting may make it possible to create a spousal lifetime access non-grantor trust, or SLANT. As a non-grantor trust, the SLANT would grow free of state income tax in a jurisdiction such as Delaware, subject to potential state sourcing rules and throwback tax, for example, in California and New York.

Families looking to maximize the amount they can leave to future generations free of gift, estate and GST tax can consider several strategies that maximize use of the current high exemption amounts. A sale to an intentionally defective grantor trust, or IDGT, which could be a Dynasty Trust or SLAT, is one of the most powerful strategies to set aside substantial amounts of assets for future generations. Typically, the first step is to fund the IDGT with an amount equal to 10% of the assets that the IDGT will be acquiring. The initial gift is often referred to as seeding the trust, although some practitioners are comfortable eliminating this step if there are adequate beneficiary guarantees.

For example, a married couple who are parents could gift $20 million to an IDGT without fully utilizing their entire combined exemption amount, and the IDGT could then buy $200 million worth of assets from the parents for a promissory note. The IRS publishes applicable federal rates monthly; the minimum interest-only payment that the parents would need to charge on a promissory note for 30 years would be 4.1% (for a loan made in October 2024). To make the sale to IDGT strategy even more effective, wealthy families often sell assets, such as closely held business interests, to the IDGT at a discount due to their lack of marketability and control. Families could create a family limited partnership, or FLP, or a family LLC to manage the family’s investments. It is essential that the entity has a legitimate business purpose and that the family respects both the form and substance of the structure. For instance, an FLP interest could have a $300 million undiscounted value but could be purchased by the IDGT for a $200 million promissory note if a valuation provided a 33.33% discount for lack of marketability and control. If such an asset had a 7% net growth rate over a 30-year period, approximately $1.5 billion could be transferred to future generations completely free of gift, estate and GST tax.

Every family has unique characteristics and dynamics, and again, any plan should reflect the collaborative counsel of advisors, including a Wealth & Fiduciary Advisor, attorney and accountant. A professional appraiser also should be included to value assets other than cash or publicly traded securities. And don’t forget to file Form 709, United States Gift (and Generation-Skipping Transfer) Tax Return, to report any gifts that take advantage of the exemption amount.

Every divorce is unique, but no one needs to feel alone in the experience. Building a team of advisors, including an attorney, an accountant, and a wealth management advisor, is the first step in working to a positive outcome – and a fresh start.

Like most preventative measures, pre- and post-nuptial agreements can feel difficult in the present, but they can save a lot of grief in the longer term. Please see below for a brief overview.

There are typically four types of divorce proceedings: self-settled divorce (no attorneys, no mediators), mediated divorce (no attorneys, but a qualified mediator representing both spouses), collaborative divorce (each spouse hires their own attorney but divorce proceeds outside of court), and litigated divorce (both spouses hire attorneys, and the case is presided over by a judge in court). In any case, it is wise to meet with an accountant and wealth advisor in conjunction with legal counsel.

Each state has different rules and case law governing divorces and asset settlements. Within the nine community property states, for example, assets are deemed community or separate property of one spouse, and all community property will typically be divided equally.1 Conversely, equitable distribution states split all assets, earnings, debts, and property in a division in a manner meant to be fair but not necessarily equal.

Custody of minor children or any suspicion of nefarious activity and hidden assets should be discussed with an attorney.

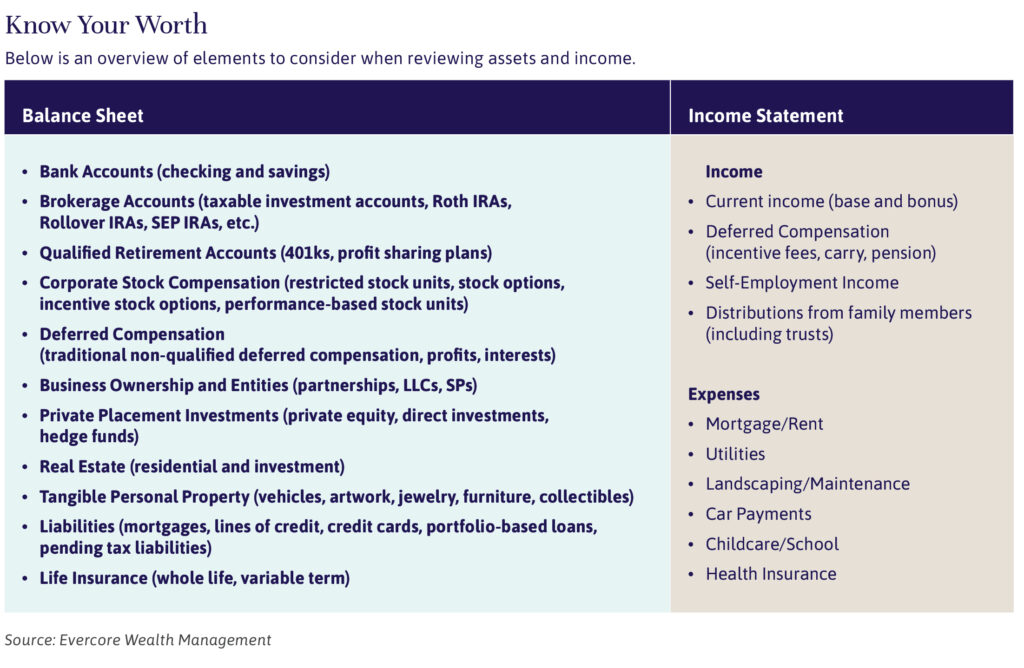

The most important starting point in a divorce negotiation is to build a firm understanding of the current balance sheet and income statement. A wealth advisor and a tax specialist can help identify and value assets and liabilities, as well as income and expenses. The chart below can serve as a primer of the types of assets you may identify, but this will vary from individual to individual.

Some assets, like homes or artwork, cannot be split, and so adjustments are made to the division of other assets to adjust for those values. This is a potential pitfall for many divorcing spouses, as personal preferences may drive decisions that undermine future lifestyle spending.

A thorough understanding of attributes of various types of assets is required before deciding what makes sense for each individual. For example, the family home may prove expensive, with carrying costs including local property taxes, insurance, maintenance, and repairs. Selling it later may incur substantial transaction and tax costs not accounted for in the divorce settlement. Further, once a divorce is finalized, the spouse that retains the primary residence loses their former spouse’s potential capital gains exemption (currently $250,000). Assets should be evaluated on a net basis and in the context of an individual’s income, liquidity, and risk profile.

Here’s another example: The inherent value of an IRA, which is not accessible without penalties until age 59½ and is taxed as ordinary income when distributed, is not equal in value to a brokerage account invested in fully liquid securities taxed at capital gains rates. Similarly, a brokerage account invested in equity securities with a large, embedded capital gain and low income yield does not have the same tax implications, income generation or risk profile as a portfolio comprised of municipal bond securities generating tax-exempt income.

It is also important to identify and review assets that may hold little value now but could be worth more in the future. Some are more easily valued, such as restricted stock units vesting over time, while others may not be so, such as interests in a private company that could be headed toward a liquidity event. Even if the current value is negligible, analysis should be given to potential future value of the assets before they are dismissed as part of the asset split.

Balance sheet items outside an individual’s taxable estate are also important to incorporate in divorce planning. If either spouse is a beneficiary of an irrevocable trust with distributions that benefited the marriage, this may be considered as part of the negotiation around alimony and maintenance payments. Parents should consider whether any accounts have been set up for their children’s education or future benefit, such as 529 plans, Uniform Transfers to Minors Act accounts, or UTMAs, and irrevocable trusts.

In negotiating alimony payments and asset splits, it is important to identify current lifestyle costs, on a pre- and post-tax basis. Some expenses may decrease post-divorce while others, such as healthcare insurance or housing/mortgage servicing, may go up. Anyone counting on alimony should also consider securing agreement or insurance that the payments will continue in the event of the payor’s disability or death. A lifestyle analysis, a long-term financial planning tool, can also be incorporated as the divorce is being worked through to help identify what various settlement plans might mean for an individual’s future financial picture.

The divorce is finalized and your assets equitably split. Now what? A balance sheet is once again the starting point of the financial planning discussion – this time focused on defining the future.

Creating a lifestyle analysis incorporates current income, such as wages, investment income, and alimony, as well as current and future expenses. It provides a basis for the discussion around how to build a portfolio to achieve future goals. As with any major change, it may take a while to figure out what the new normal is.

Divorce is a complete overhaul to each spouse’s financial picture that needs to be reevaluated. Part of that is redefining an investor’s risk tolerance post-divorce. Simply put, risk tolerance refers to an investor’s willingness and ability to endure fluctuations in the value of their investments in pursuit of potentially higher returns. One might find that with a changed financial situation, and no longer making decisions in conjunction with a spouse, one’s risk tolerance is different than it was. It is also important to consider an individual’s new tax profile when deciding on underlying investment vehicles and creating an annual capital gains budget. Understanding – and regularly revisiting – risk tolerance and asset allocation is essential in constructing a portfolio that aligns with financial goals, time horizon, and emotional comfort level.

It’s also worth noting that divorce often comes with a heavy administrative burden. While some to-do’s may be top of mind, such as name changes and home titles, others, including estate documents, retirement beneficiary designations, and asset and debt titling, are just as crucial.

A wealth advisor can assist throughout the divorce process and beyond, helping with both financial and nonfinancial needs. Developing a thorough understanding of the current balance sheet, lifestyle needs, goals, and appetite for risk can go a long way in making informed decisions and easing a significant transition.

Judy Moses is a Partner and Portfolio Manager at Evercore Wealth Management. She can be contacted at moses@evercore.com. Neza Gallitano is a Managing Director and Wealth and Fiduciary Advisor at Evercore Wealth Management and Evercore Trust Company. She holds the Certified Divorce Financial Analyst designation. She can be contacted at neza.gallitano@evercore.com.

A prenuptial agreement is a legally enforceable written agreement made by a couple before marriage. It discloses a full and fair list of all property and debts of each partner and spells out the treatment in the event of the dissolution of the marriage or death. It can also discuss the treatment of future earnings and spousal support. The agreement will define what is separate and what is marital property; these assets should stay that way during the duration of the marriage.

Families often use trusts to try to protect family assets. However, distributions from a trust, if comingled with marital assets, could become marital property. In some states, a beneficiary of a trust may have trust assets treated as marital property. Irrevocable trusts cannot be changed except under certain circumstances. Prenuptial agreements can further help solidify protection of these assets.

A prenuptial agreement protects both spouses. For the spouse entering the marriage with assets, it can protect an inheritance, closely held business or other family legacy asset from leaving the family line. It also protects an individual entering a second or subsequent marriage. Importantly, it can protect an individual from taking responsibility for the debts of the other spouse. On the other hand, it can also protect the less affluent spouse, especially when that individual relies on the other spouse for income.

A prenuptial agreement requires both parties to have adequate legal representation and to fully disclose all significant assets. Generally, the agreement should be signed in writing before a notary at some period before the wedding. As with any contract, a prenuptial agreement can be renegotiated at any time.

Your Evercore Wealth Management Wealth and Fiduciary Advisor can help you and your attorney design a prenuptial agreement by reviewing your financial statements and advising on whether your future lifestyle needs will be met under the agreement.

– NG

The wonderful thing about growing up in one country and living in another is that you get to come “home” twice on a single visit. But managing family assets across borders can feel like more than twice the work.

Families with international connections often need to comply with the laws of both the United States and their home country, which may have significant differences in tax, legal, and accountancy principles. The result can be a complex web of legal, tax, and investment challenges. Add in a third or fourth jurisdiction, and the risk of costly mistakes multiplies exponentially. Consider the fact that while every U.S. state other than Louisiana uses a “common law” system (based on traditional English law), most European and Latin American countries apply a “civil law” system. Civil law countries are more likely to have forced heirship rules, limit flexibility of disposition, and give little legal effect to trust structures. Furthermore, even ostensibly common law jurisdictions like the United Kingdom and Canada differ significantly from the United States in how they treat traditional estate planning structures.

Americans living abroad may face even more complex challenges. Unlike citizens of just about every other country (except Hungary and Eritrea, at present), American citizens continue to be subject to U.S. income, estate, and gift tax rules, regardless of where they live or where their property is located. The United States has treaties in place with many countries, which may help to offset the effects of competing jurisdictions, but navigating the complex interplay of different systems can be treacherous.

Even relatively small distances can loom large if there’s a border in between. For example, if one spouse is a U.S. citizen and the other Canadian, chances are that, regardless of which country they live in, they hold investable assets in both, and are therefore subject to multiple (often conflicting) tax, legal, and reporting requirements. It may be difficult to find a single wealth management professional able to cover all sides of that equation.

Accordingly, any dual (or more) nationality families are best served by a team of advisors with the knowledge and confidence to review both the U.S. and international aspects of their estate plan and investment portfolio. In addition to the requisite legal, technical, and financial expertise, this team of advisors also needs the structural support necessary to satisfy all tax, compliance, and reporting requirements, including the ability to track cost basis in accordance with the tax and accounting rules of both jurisdictions.

Similarly, dual or multinational families need advisors who can continually review their charitable giving, retirement planning, and saving for their children’s education to maximize the tax benefits in each country. Remember that mainstream U.S. tax-deferral vehicles like IRAs and 529 plans may not be given the same special treatment in other countries.

Perhaps the most pressing issue for many families with a non-U.S. citizen member (particularly, a spouse) is the looming sunset of the current estate and gift tax exemptions at the end of 2025 (currently $13.61 million for 2024 and estimated to drop to around $7.5 million at the end of 2025). Under U.S. law, noncitizen spouses do not benefit from an unlimited marital deduction for gift and estate tax purposes. Similarly, the “portability” rules allowing a surviving spouse to carry over any unused exemption are not available. Therefore, it is even more important for a U.S. resident or citizen with a non-U.S. spouse to consider using the increased exemptions to make lifetime gifts to that spouse before the sunset.

Multinational families are common now, as members move to a new country but maintain their ties with the old. It’s not the simple life, that’s for sure. But with the appropriate planning, it can be a wonderful way to live, rich in perspective and opportunity, as well as challenges.

Alex Lyden is the Chief Fiduciary Officer at Evercore Trust Company, based in Wilmington, Delaware. He can be reached at alex.lyden@evercore.com.

Life insurance is often unnecessary for ultra-high net worth families. But in the right circumstances it can be a powerful planning tool, helping to provide estate liquidity, fund buy/sell agreements, or shelter taxes. Here are a few brief highlights:

Income replacement. High earners, as opposed to those with considerable assets, should consider life insurance (and possibly disability insurance) if the loss of income would materially affect their family’s quality of life. Term insurance is usually sufficient to mitigate this risk. Cash-flow projections will be important in determining the size and duration of the policy, but it’s fair to say that most young families could benefit from some form of coverage.

Estate liquidity. Families with a taxable estate of primarily illiquid assets, such as real estate or a family business, can arrange for life insurance to pay state and federal estate taxes, avoiding a forced sale at the owner’s death. Section 303 of the Internal Revenue Code allows an estate to sell shares back to a closely held business to cover estate taxes without being taxed as a dividend distribution in certain cases. Section 6166 allows beneficiaries to extend payments for all or part of the estate taxes attributable to the business for up to 14 years if certain conditions are met. Executing these arrangements can be a complicated and costly process, however, and should be considered very carefully.

If estate liquidity is an issue for a married couple, a simple solution may be a second-to-die universal life insurance policy. Usually, a well-planned estate pays taxes only at the passing of the surviving spouse. A second-to-die policy will only pay out on the death of both spouses, which drives down the cost of insurance. It provides long-term coverage at a relatively low cost.

Estate equalization. Parents who want to transfer a family-owned business to children active in the business without shortchanging other children can also consider a second-to-die universal life policy if there are not enough assets to equalize inheritances. Again, comprehensive estate and trust planning is necessary in navigating the related tax, control, and distribution issues.

Funding buy/sell agreements. Business partners can arrange for insurance to help cover the purchase of shares at the death of one or more of the partners. These policies work best as part of a robust buy/sell agreement and business succession plan that details business continuity in the event of retirement, disability, or death. Term or universal insurance may be appropriate, depending on the broader plan and participants.

Tax sheltering. Private placement life insurance, or PPLI, is a form of variable universal life insurance that can be a powerful tax sheltering tool for high earners with large balance sheets and significant liquidity. These policies allocate investments to liquid and to illiquid investments, such as hedge funds or private equity partnership interests, and shelter the income tax liability generated from distributions. Policyholders should have a decades-long investment time horizon, but the result can be a significant savings on income and, eventually, estate taxes, especially when combined with an irrevocable life insurance trust.

It should be noted that PPLI has come under recent scrutiny, with the Senate Finance Committee suggesting that regulators take a closer look at these policies.

When deciding where to get advice on your policy, remember that an insurance provider’s sales incentives should not drive your decisions in buying, keeping, or terminating an insurance policy. Please contact your advisor at Evercore Wealth Management and Evercore Trust Company, N.A. for an objective discussion of your family’s insurance needs and how insurance fits in with other aspects of your comprehensive wealth plan.

Sean Brady is a Managing Director and Wealth and Fiduciary Advisor at Evercore Wealth Management and Evercore Trust Company. He can be contacted at sean.brady@evercore.com.

Here are the major types of life insurance and considerations for high net worth and

ultra-high net worth families:

– SB

Editor’s note: Evercore Wealth Management released its legislative and regulatory guide in October to inform clients of end-of-year planning discussions in the context of overall wealth planning goals.

Highlights and subsequent relevant IRS updates are included here. Please contact your advisor for further information or to discuss your specific circumstances.

For tax year 2024, the top marginal tax rate remains 37% for individual single taxpayers with incomes greater than $609,350, married couples filing jointly with incomes greater than $731,200, and estates and trusts with incomes greater than $15,20

The new Setting Every Community Up for Retirement Enhancement (SECURE) Act 2.0 included adjustments to required minimum distributions and qualified charitable distributions. In addition, guidance issued by the IRS addressed estate tax portability elections, and a recent tax court opinion highlighted the importance of careful planning and timing of charitable contributions ahead of a liquidity event. The age for RMDs was raised from 72 to 73 as of January 1, 2023, and will rise again to 75 on January 1, 2033.

Qualified Charitable Distributions (QCDs)

Currently, an individual who is 70 1/2 or older can make QCDs up to $100,000 directly from an IRA to a qualified charity – but not to a donor-advised fund. Beginning in 2024, the QCD amount will be indexed for inflation to $105,000.

Individuals who are 70 1/2 or older are now permitted a one-time QCD of up to $50,000 from an IRA to a charitable gift annuity (CGA), charitable remainder unitrust (CRUT), or charitable remainder annuity trust (CRAT) that benefits the participant or their spouse. For more information, please speak with your Wealth Advisor.

Inflation Reduction Act

The Inflation Reduction Act was passed in 2022 and continues to be implemented. It includes a wide variety of legislation targeting many different sectors of the economy. Among its provisions are:

Gift and Estate Tax

The 2024 lifetime gift and estate tax exemption will be $13,610,000, an increase of $690,000 from 2023 levels. Additionally, the annual gift tax exclusion amount will be $18,000 for gifts made in 2024, an increase of $1,000 from 2023.

As always, we recommend meeting with your Evercore Wealth Management advisor, your attorney and your accountant before implementing new strategies to ensure that they are aligned with your long-term goals.

Like professional athletes, corporate executives are often paid for performance.

Unlike many athletes, executives may have more time on their side, thanks to deferred pay compensation structures that reward those who hang in there – and plan well. And it’s not just the top players who benefit. In recent years, companies have expanded deferred compensation packages well beyond the C-suite, in some cases to nearly all employees. Long-term incentives as a proportion of C-suite executive pay have more than tripled over the last few decades to about 70% of total pay.

That proportion is likely to continue rising in the wake of the 2022 ruling by the Securities and Exchange Commission, or SEC, on “Pay vs. Performance,” which requires companies to disclose executive compensation along four specific measures, as illustrated below. The ruling is the latest step to pay transparency, which started with the “Say on Pay” ruling in 2011 as part of the Dodd-Frank Act. Shareholders and boards want to see that executives have skin in the game, and by large, executives have benefited enormously. Let’s take a quick look at the most common types of executive compensation, along with the advantages, drawbacks, and other considerations. Many companies will provide a mix of compensation structures, with the most common features including cash compensation with additional incentive compensation in the form of restricted stock and performance-based restricted stock.

Stock options are a powerful, tax-efficient tool to compensate executives, which gained immense popularity in the 1950s when marginal tax brackets were much higher. If the underlying stock price grows, the owner of a stock option can participate in those gains while simultaneously deferring tax until the exercise of the option. And if the underlying stock price falls below the strike price, the owner of the options can simply let them expire; the only downside is opportunity cost. Further, if the stock options are qualified incentive stock options and the holding requirements are met, the owner may be able to avoid ordinary income tax due when they exercise the options and on the difference between the sale price and the strike (purchase) price at disposition of the shares. Although, it is important to note that the exercise of incentive stock options could result in significant alternative minimum tax consequences.

Other types of stock awards also align the executive and shareholder goals. In other words, everyone makes more if the company does well. Although, noncash awards may carry more risk for the executive. Restricted stock and restricted stock units, or RSUs, are taxed as ordinary income at the time of vesting. Unless the share owner is able to simultaneously sell shares at the time of vesting, this means that the tax bill is due before the liquidity is available and cash must be used from other sources. Performance-based restricted stock units, or PSUs, vest only if the company hits certain performance targets and are thereafter taxed like RSUs. PSUs are especially appealing for companies and boards, as they motivate executives to meet performance targets while also allowing companies to present large compensation packages to attract executives.

There are several other compensation structures that are available but less prevalent, such as traditional deferred compensation plans, long-term incentive plans (or LTIPs) and performance stock plan “kickers” (whereby additional discretionary stock grants can be made for superior performance). Employees should note that forced bonus deferrals are often made to non-qualified deferred compensation plans. These plans are subject to the creditor risks of the company, which should be taken into account when considering how much to defer and how to plan for these funds. Companies often implement new compensation measures trying to balance current year fiscal reporting while competing to attract top-tier talent.

In just about all cases, employee shares in both public and private companies are often required to be held in the employee’s own name. Transfers to family trusts or family members are either prohibited or very restricted. As a result, sometimes the largest asset on an individual’s balance sheet cannot be used to take advantage of the current lifetime estate tax exemption amounts.

Therefore it is important to maximize estate planning techniques available for unrestricted assets, as well as develop a plan to incorporate company stock assets into the estate plan once they become unrestricted. Some companies do allow vested shares of common stock to be reassigned, so it is also important for employees to understand the specific policies of their incentive compensation plans.

Companies competing for talent at all levels put together enticing compensation packages but are equally motivated to push much of this compensation into long-term payout structures, thereby tying employee compensation to tenure. Further, companies have different vesting conditions in the case of termination or change of control. It is important for employee shareholders to understand how their shares vest, or don’t vest, in each of these scenarios to calculate a net present value of their compensation, which can guide future decision making.

Often, employee shareholders do not actually diversify away from company holdings until they leave that role. The bull market that we’ve seen since March of 2009 and record IPO valuations have made it easy for employee shareholders to stay invested. Without proper planning, though, employees could be left holding the bag. Employee stockholders who worked at Lehman Brothers in the first two weeks of September 2008 saw their net worth invested in company stock drop 46% before being completely wiped away in one day. More recently, the COVID-19 pandemic caused some companies’ values to soar (such as Zoom and Peloton), while others plummeted (such as airline stocks and hotel brands). Both Zoom and Peloton shares have fallen back to pre-pandemic levels, off 89% and 97% of their COVID-19 era peaks, respectively. This year, employees and other shareholders of First Republic Bank lost nearly all the value in their holdings as the share price lost over 90% of its value over a period of six weeks in February and March 2023, before losing nearly all remaining value before May. Executives at WeWork and Twitter had similar experiences as fraught management caused share values to tumble. While these examples are extreme, even lower levels of volatility can impact an individual’s cash flow plans or retirement timing.

Diversification is therefore a crucial part of the planning process for executives. However, sale restrictions, trading windows, and tacit expectations not to sell stock can often prevent employee shareholders from fully diversifying their concentrated positions, which further exposes their net worth to large fluctuations and volatility. One simple way for employees to diversify away from company stock is to elect shares to be sold upon vesting or exercise to cover income tax withholding. Some companies even allow employees to elect a higher withholding rate than the statutory federal withholding rate of 22%, thereby allowing them to fully cover their tax liability. Selling shares to cover tax withholding allows individuals to reduce their overall employee stock exposure while preserving cash and other assets outside of the concentrated stock. It is important to work with a wealth planning advisor and a CPA to properly plan for tax liabilities associated with vesting of restricted shares or the exercise of options.

10b5-1 plans are often established to allow insiders of public-traded corporations to set up a trading plan for selling company stock they own while abiding by insider trading laws. Documents pertaining to these plans set forth certain events, whether date-based or stock-price based, at which an executive’s shares will be sold. Plans can stipulate various time frames, but typically are in force for six months to two years. While it may be possible to modify and terminate an existing plan, such changes are subject to significant limitations.

Proper planning can enable executives to ensure that they are meeting lifestyle and tax liability needs through their direct (cash) payments while addressing their incentive payments in the context of longer-term goals. This planning should consider various scenarios, including those in which the company performance metrics miss their mark and shares don’t vest. With the right planning, an executive will be fully apprised of the existing and potential value of a compensation package involving stock and have the power to understand and negotiate for future roles. Most important, proper planning allows individuals to maximize their balance sheet and cash flow and make informed diversification decisions to preserve their earnings for years to come.

It’s also worth noting that different companies call these incentive plans by different names, in which case a wealth advisor could help identify the plan and its advantages and constraints.

Neza Gallitano is a Managing Director and Wealth & Fiduciary Advisor at Evercore Wealth Management and Evercore Trust Company, N.A. She can be contacted at neza.gallitano@evercore.com.

Several legislative and regulatory updates that may be worth considering this year, in the context of overall wealth planning goals.

For instance, the SECURE 2.0 Act included adjustments to required minimum distributions and qualified charitable distributions. In addition, guidance issued by the IRS addressed estate tax portability elections, and a recent tax court opinion highlighted the importance of careful planning and timing of charitable contributions ahead of a liquidity event.

Please contact wealthmanagement@evercore.com if you would like to learn more about our 2023 Year-End Wealth Planning Review, our annual guide, to highlight potential opportunities and strategies ahead of planning discussions with our clients.

You may have heard the proverb “shirtsleeves to shirtsleeves in three generations,” but did you know that Italians say that families go “from stalls to stars to stalls”; Chinese caution that “wealth never survives three generations”; Mexicans warn of “first-generation traders, second-generation gentlemen and third-generation beggars”; and Swedes sum it up with the stark “acquire, inherit, ruin?”

Regardless of the country, culture or even tax laws, there appears to be a sense that when families attempt to transfer wealth to future generations, something vital is often lost.

It doesn’t have to be this way, of course. Families that successfully transfer wealth think long and hard about what they are trying to preserve – and why they are trying to preserve it. They focus on preserving nonfinancial capital in addition to financial capital. This can include individual capital, or each family member’s personal strengths and talents; collective capital, such as family members supporting each other; community capital, which includes the family’s contributions to the local community; and spiritual capital, which can take many forms but drives the family’s ethos. In short, they transfer values along with money.

Communication is a crucial element in maintaining success. Much has been written about the significant differences among generations – from Baby Boomers and Generation X, on to Generation Y (the Millennials), Generation Z, and the most recent Generation Alpha. Successful families acknowledge that the life experiences of grandchildren and future generations are going to be very different from those of their grandparents. As an example, according to a 2021 Pew Research Center survey, more than two-thirds (68%) of U.S. respondents said they think today’s children will be financially worse off as adults than their parents.1 For wealthy families, this is an even bigger challenge, given the relatively higher starting point. A recent Stanford study found that approximately 90% of those born in the 1940s earned more than their parents as adults, compared to only about half of those born in the 1980s.2

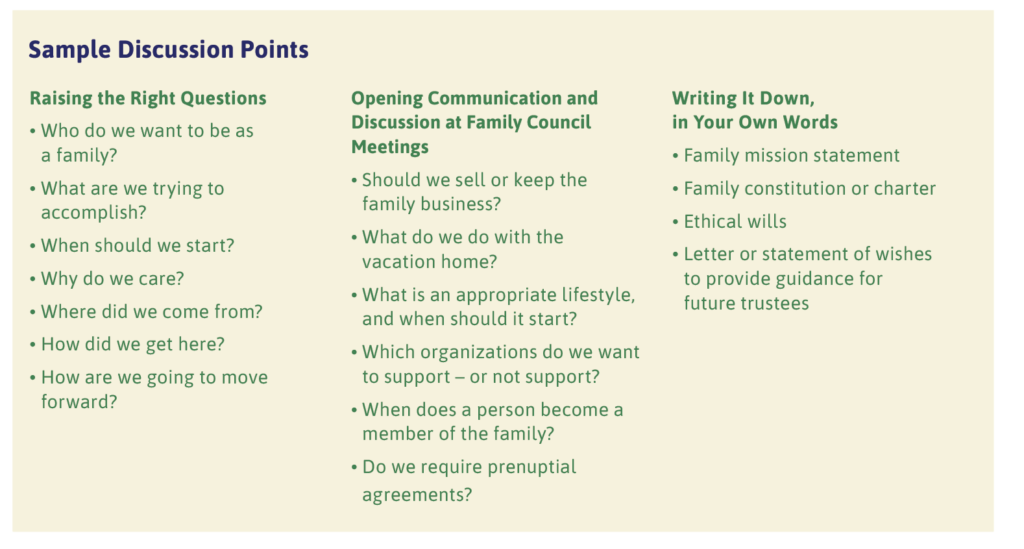

Demographics, addressed from an investment point of view in this issue of Independent Thinking, shouldn’t need to shape a family’s destiny – not if differing perspectives are raised and addressed. To encourage healthy communication, regular family council meetings can be surprisingly effective. Family council meetings can provide every member of the family an opportunity to proactively contribute to the family’s long-term success while preserving the role of the matriarch and/or patriarch. Please take a look at the chart below for some sample discussion points.

Another key factor for successful families is that that they tend to be philanthropic. Indeed, studies have shown that philanthropy actively fosters happiness – as well as the potential for significant tax savings.3 In preparing the next generation to be happy and productive members of society, family philanthropy – or giving to charity collaboratively as a family – could be one of the most impactful activities to consider.4 James E. Hughes, Jr., the author of Family Wealth, put it best when he observed that: “Paradoxically, families often learn more about long-term wealth preservation through the process of learning to give away than by the process of learning to accumulate and spend.”

While healthy family governance is a vital part of multigenerational success, families can’t ignore the importance of comprehensive tax and investment planning. Since no one advisor can or should do it all, successful families rely on a collaborative team of advisors to provide a cohesive strategy for growing and preserving wealth across multiple generations. That should also include all the left-brain wealth management responsibilities, such as legal documents, asset protection, privacy, confidentiality, taxes, investments, and so on. And it should also include all the right-brain family-oriented issues: an understanding of the family’s mission, vision, and values; educating family members; and supporting future family leadership. After all, successful families don’t just care about transferring the maximum amount of assets in the most tax-efficient manner to future generations, they also focus on preserving family harmony so that their family legacy will continue for future generations.

It’s worth recalling Warren Buffett’s well-known line on giving his children “enough money so that they could feel they could do anything, but not so much that they could do nothing.”5 The challenge for families is that there is no magic dollar figure when it comes to transferring wealth to future generations in a manner that helps – rather than hinders – their future happiness and success. Anyone struggling to identify how much money that might be should instead follow the secrets of successful families and consider the more important question: “What have you prepared them for?”

Justin Miller is the National Director of Wealth Planning at Evercore Wealth Management and Evercore Trust Company, N.A. He can be contacted at justin.miller@evercore.com.

The author Zig Ziglar once said, “Money isn’t the most important thing in life, but it’s reasonably close to oxygen on the ‘gotta have it’ scale.” Still, a business owner caught up in the stress and time-consuming work of negotiating and structuring the sale of their company can lose sight of what the transaction can mean at the personal level. It’s time to take a deep breath and consider this possible once-in-a-lifetime opportunity to maximize personal after-tax profits; minimize income, gift, estate, and generation-skipping transfer taxes; accomplish charitable goals; and protect assets.

A successful transaction starts with a collaborative team of advisors – which can include investment bankers, attorneys, accountants, and strategic wealth planning advisors – all working together to prepare the business owner for the liquidity event and to maximize the value, speed, and certainty of the transaction closing. By combining tax, estate planning and business succession strategies, we believe business owners will have the greatest opportunity to maximize the wealth from the sale of their business.

With strategic wealth planning, the resulting savings can be significant – and the earlier you start, generally, the better the results can be. However, the sheer number of potential planning strategies can be overwhelming and easily lead to planning paralysis. For example, options could include intentionally defective grantor trusts, grantor retained annuity trusts, completed gift non-grantor trusts, incomplete gift non-grantor trusts, spousal lifetime access trusts, asset protection trusts, charitable trusts, family limited partnerships, family limited liability companies, qualified opportunity zone investments, qualified small business stock stacking, installment sales, discounting, recapitalization, estate freezes – it’s enough to make almost anyone’s head spin!

So, how can Evercore Wealth Management help? Consider the recent experience of a California-based couple, described below, who were able to successfully close their private transaction in a tax-efficient manner while creating a lasting legacy for their family and charity. By adding a wealth advisor to their collaborative advisory team, the couple successfully eliminated $45 million of the sale proceeds from being subject to federal income taxes, as well as $35 million from being subject to state income taxes, deferred an additional $10 million from both federal and state income taxes, generated a $6 million charitable income tax deduction, and created a lasting legacy for their family that provided both asset protection and the ability for assets to grow free of gift, estate, and generation-skipping transfer taxes in perpetuity.

Selling a business is a challenging, and often exhausting, transition. But it’s important to make time, as early as possible, to ensure that a strategic wealth plan is structured to maximize the potential advantages of the transaction. After all, this life event is often the result of many years of hard work and sacrifice. In short, don’t leave any money on the table.

If you are selling your company, consider contacting a Wealth and Fiduciary Advisor at Evercore Wealth Management and Evercore Trust Company, N.A., who can work with you, your family, and your team of advisors to help protect your wealth, your legacy, and your family’s values for future generations.

Justin Miller is a Partner and National Director of Wealth Planning at Evercore Wealth Management. He can be contacted at justin.miller@evercore.com.

A California couple was so caught up in the approaching sale of their private technology business that they almost canceled the meeting with the wealth advisor recommended by their investment banker. They already had done some estate planning years ago by funding an irrevocable intentionally defective grantor trust, or IDGT, for their children, and while they knew it was a good idea to consider other estate planning strategies, they thought it could wait. But in the end, they took the meeting.

The first thing this couple’s new wealth advisor discovered while reviewing their financial and estate planning documents was that a required gift tax return was never filed for their existing IDGT. After working with their attorney and accountant to rectify that issue, the wealth advisor prepared easy-to-follow flowcharts and detailed financial projections for the couple to consider additional tax planning options.

Next, the wealth advisor recommended setting up three new irrevocable non-grantor trusts in Delaware for the benefit of each of the couple’s adult children and any future grandchildren. Unlike their IDGT, each of those new non-grantor trusts qualified for a $10 million exclusion from both federal and state income taxes by taking advantage of section 1202 of the Internal Revenue Code with respect to qualified small business stock, or QSBS. As a result of the QSBS planning, the couple was able to exclude a total of $40 million of proceeds from federal income taxes – that is, $30 million with the non-grantor trusts and $10 million personally. And even though they lived in a state that does not have a similar QSBS exclusion at the state level, the three non-grantor trusts based in Delaware also were able to avoid state income taxation on $30 million in gains. In addition, by using their remaining lifetime exemption amount, which is $25.84 million per couple in 2023, those trusts’ assets and all the future growth of the assets will remain protected from creditors and free of gift, estate, and generation-skipping transfer taxes for multiple generations.

After their wealth advisor walked them through various philanthropic planning options, the couple decided that a private foundation was not worth the extra administrative burden, but they did decide to set up a donor-advised fund with $5 million of their company stock. Not only did that charitable gift generate a $5 million tax deduction – which was used to offset their ordinary income from salaries, bonuses, and exercise of stock options – but the gift also protected the family from paying any capital gains on the sale of that stock. In addition, the couple funded a charitable remainder trust, or CRT, with $10 million, which generated an additional $1 million charitable deduction, deferred federal and state income taxes, and should provide an annual payment of 7.7% of the value of the trust to the couple for the rest of their joint lifetimes (projected to be $21 million pre-tax over 32 years with an assumed 7% return). Everything remaining in the CRT after both their deaths (estimated to be $7.2 million with that assumed 7% return1) would go to their donor-advised fund, which their children would then be able to participate in giving away to charities during their lifetimes.

As part of the comprehensive wealth planning process, the wealth advisor also made sure that the couple had a short-term cash management plan in place to protect the post-transaction proceeds, generate interest, and cover the federal and state income taxes that would be due on the transaction. The wealth advisor included a senior portfolio manager as part of the wealth management team to help this couple create an initial goals-based investment policy statement that would help guide their long-term investment strategy and overall asset allocation, taking into account both the location and structure of all their assets across various family trusts and business entities.

Last, the wealth advisor facilitated the couple’s first family council meeting, in which their adult children had an opportunity to learn more about the various planning structures, and the family could communicate about how the substantial proceeds from the sale of the company would be used to support the family’s values and future legacy.

– Justin Miller

The new SECURE Act 2.0 (Setting Every Community Up for Retirement Enhancement) includes some important provisions affecting high net worth individuals and families.

Please see our recent publication linked here, “The Impact of the SECURE Act 2.0 on Retirement Accounts,” for details of some of the key changes. Please contact your Evercore Wealth Management wealth advisor or email us at wealthmanagement@evercore.com with any questions or concerns.

Evercore Wealth Management, LLC and Evercore Trust Company, N.A. professionals assemble an extensive annual guide, to highlight potential opportunities and strategies ahead of our end-of-year planning discussions with our clients.

While the major tax proposals that would have impacted high net worth individuals, trusts and estates were not included in the final Inflation Reduction Act, there are still some updates to current federal tax law that may be worth considering in the context of overall wealth planning goals. These include changes to required minimum distributions, qualified charitable distributions, and gift, estate, and generation-skipping tax exemptions.

Please contact wealthmanagement@evercore.com if you would like to learn more about our 2022 Year-End Wealth Planning Review.

Higher interest rates – up fourfold in a year, albeit still low – can complicate wealth planning decisions. But families who keep rates in perspective, stick with established wealth plans, and make tactical moves now should stay on track to help meet long-term goals.

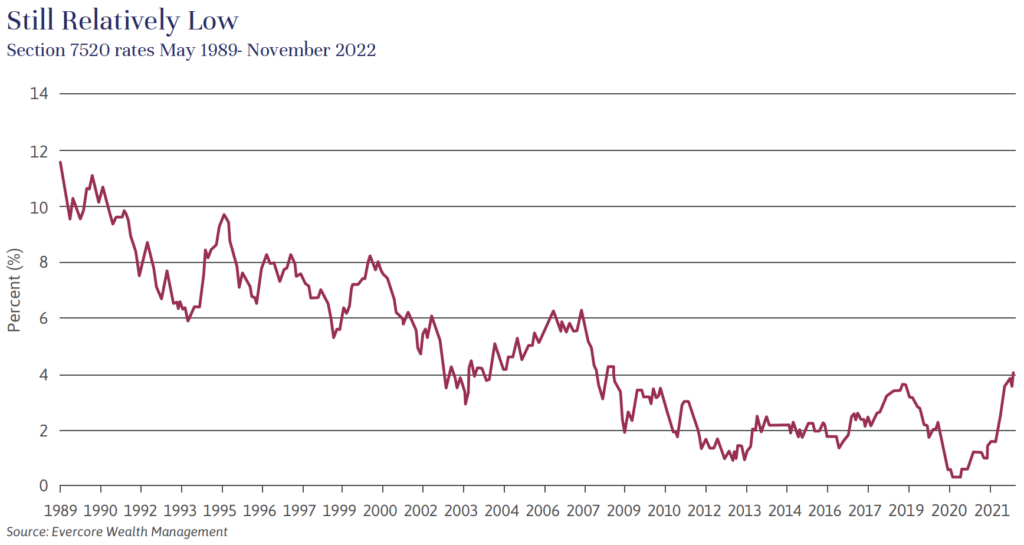

Grantor Retained Annuity Trusts, or GRATs, have been popular with high-net-worth families for years. Historically low interest rates have enabled grantors to fund trusts at the Section 7520 rate, or the hurdle rate, published monthly by the IRS, in the expectation that the funds would in fact outperform that rate and the excess appreciation be transferred to the beneficiaries free of gift and estate tax. That worked brilliantly when rates were low and markets were rising. Now families have a higher hurdle to surmount; as of November, the 7520 rate is 4.8%, up from 1% just a year ago. And the markets haven’t been helping the existing GRATs.

This is where perspective matters. Sure, rates aren’t as favorable as they were a year ago, but as illustrated by the chart below, they are still low from a longer-term perspective. As for the markets, a bear market can be a boon when funding a brand new GRAT. Once the account performance clears the hurdle rate, the GRAT beneficiaries could benefit from a subsequent market recovery. (See the diagram below for an example of a GRAT.)

A Charitable Lead Annuity Trust, or CLAT, may still be an attractive transfer strategy for families who are charitably inclined. CLATS are split-interest trusts that benefit a charity during their terms and, at the termination of the trust, allow remaining assets to pass to the remainder beneficiary, typically the heirs. As with a GRAT, the amount of the remainder will depend on whether the trust’s investments outperform the Section 7520 rate.

In a still relatively low interest rate environment and after a market dislocation, CLATs can be an effective means of wealth transfer to the next generation. The interim beneficiary of the charitable lead interest can be a donor-advised fund, a private foundation, or a public charity. If structured as a grantor trust, the grantor may have an immediate tax deduction as well. Decisions between grantor and non-grantor CLATs are based on personal circumstances and should be made with professional consultation.

Please note that both GRATs and CLATS should only be used for the transfers to the immediate next generation, not to grandchildren.

Families looking for more immediate wealth transfer solutions, say to help buy a home or start a business, may want to consider intra-family loans, especially now that mortgage and bank personal loan rates have spiked. Intra-family loans can be made using the Applicable Federal Rates (AFRs) published monthly by the IRS. At present, that could mean as much as a three-percentage point difference on a 30-year mortgage. It is important to note that the loan documents should be properly drafted, as they may otherwise be viewed by the IRS as a gift. The interest on the loan will be taxable to the lender as ordinary income.

Other estate-planning vehicles, such as Qualified Personal Residence Trusts (QPRTs) and Charitable Remainder Trusts (CRTs), will become more attractive if interest rates continue to rise. We will review these in future editions of Independent Thinking as circumstances warrant. At present, rates are still relatively low, and we continue to think that it is more likely than not that they will stay that way. (See John Apruzzese’s article titled, Orienting in a Changing Investment Landscape.)

Either way, it’s important to keep in mind that interest rates should never be the only driver in wealth transfer decisions. While giving sooner rather than later could provide significant tax benefits, as a married couple can transfer up to $24.12 million in 2022 and $25.84 million in 2023 completely free of taxes over their lifetimes until 2025, after which time the exemption amounts are roughly halved, transfer strategies should also be executed in the context of long-term plans. Families considering substantial transfers should consult their Evercore Wealth & Fiduciary Advisors to review the most appropriate planning vehicles in the context of long-term wealth plans, as well as prevailing economic and market conditions.

Making significant gifts to loved ones is arguably one of the most fraught wealth management decisions. Emotionally, we need to balance the joy of giving during our lifetimes with a potential loss of control and the prospect of unintended consequences. Practically, we need to weigh how much we can afford to give, with the realization that every dollar not transferred could be subject to a 40% federal estate tax (or more, if rates return to previous levels), as well as potential state estate taxes.

The last thing anyone wants is to have to borrow from their kids or grandkids later in life because they gave too much away. Whether you have $10 million or $100 million, a long-term cash-flow analysis – also called a lifestyle analysis – is a necessity. No one wants to be forced into significant drawdowns at the wrong time, which means that inflation and market volatility must be considered. In addition, wealthier people tend to live longer than average, and a longer life could bring unexpected and uninsurable medical expenses down the road.1

Sometimes, even those with more wealth than they would ever spend in multiple lifetimes might be afraid to give. In that case, it is important to address any anxiety from a psychological and emotional perspective, as well as from a practical one.

Some people want to know how much is enough. Other people want to learn how much is too much. Warren Buffett once said that the perfect amount to give children is “enough money so that they would feel they could do anything, but not so much that they could do nothing.”2 Unfortunately, there is no magic number.

Instead, the answer is to give loved ones no more than they are prepared for. An unprepared individual could receive a few hundred thousand dollars, and it could ruin their life – they might drop out of school, abuse drugs and alcohol, or develop a gambling addiction. On the other hand, a prepared person could be gifted millions of dollars and could still turn out well – continue to study hard, build a career, raise a family, and become a pillar of the community.